Pradhan Mantri MUDRA Yojana (PMMY)

- 10 Apr 2026

In News:

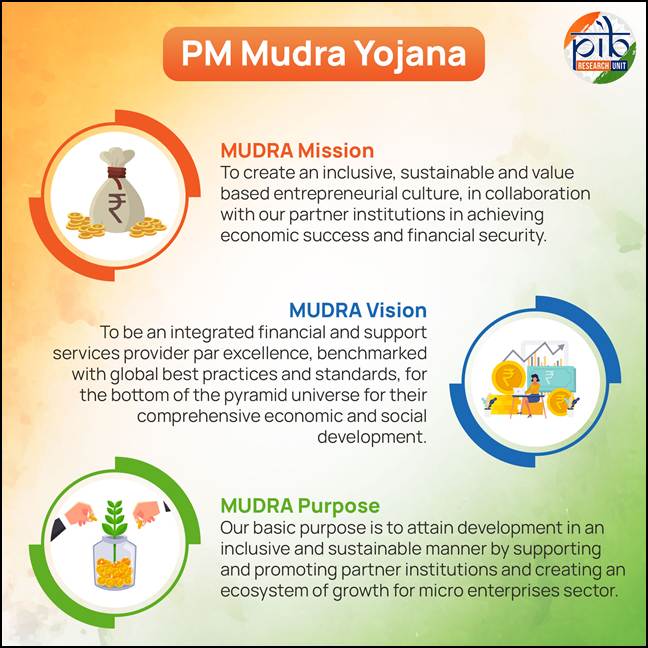

Launched on April 8, 2015, the Pradhan Mantri MUDRA Yojana (PMMY) has completed 11 years as a cornerstone of India’s financial inclusion strategy. By focusing on the philosophy of "Funding the Unfunded," the scheme has successfully integrated millions of non-corporate, non-farm micro and small enterprises (MSEs) into the formal financial ecosystem.

Core Philosophy: The Three Pillars of Financial Inclusion

The PMMY is built upon three strategic objectives designed to serve the underserved:

- Banking the Unbanked: Bringing the informal sector into the fold of institutional finance.

- Securing the Unsecured: Providing credit without the requirement of traditional collateral.

- Funding the Unfunded: Ensuring capital reaches those traditionally overlooked by banks.

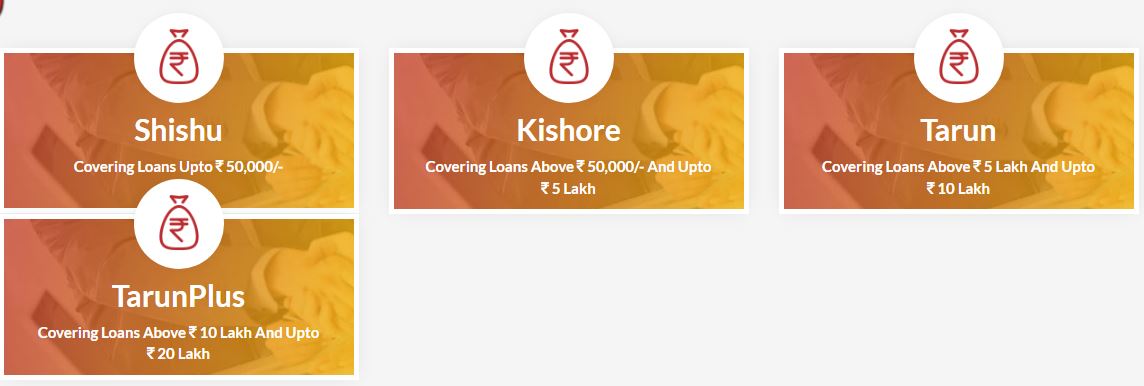

Key Features and Loan Structure

PMMY provides collateral-free institutional credit up to ?20 lakh. The loans are categorized based on the stage of growth and funding requirements of the micro-unit:

|

Category |

Loan Range |

Focus Area |

Share (No. of Loans) |

|

Shishu |

Up to ?50,000 |

Initial seed capital for micro-startups. |

74% |

|

Kishor |

?50,000 to ?5 Lakh |

Mid-stage expansion and equipment purchase. |

24% |

|

Tarun |

?5 Lakh to ?10 Lakh |

Scaling established small businesses. |

2% |

|

Tarun Plus |

?10 Lakh to ?20 Lakh |

For successful entrepreneurs graduating from Tarun. |

0.004% |

MUDRA (Micro Units Development & Refinance Agency Ltd.), a subsidiary of SIDBI, provides refinance support to Member Lending Institutions (MLIs) such as Scheduled Commercial Banks, RRBs, NBFCs, and MFIs.

11-Year Performance Analysis (As of March 2026)

The scheme has witnessed exponential growth, transitioning from a sanction of ?1.37 lakh crore in its first year to over ?5.65 lakh crore in FY 2025-26.

- Total Disbursement: Over ?40.07 lakh crore across 57.79 crore loan accounts.

- Democratization of Credit:

- Women's Empowerment: Approximately 67% (two-thirds) of all loans have been sanctioned to women entrepreneurs.

- Social Equity: Over 51% of beneficiaries belong to SC/ST/OBC categories.

- New Entrepreneurs: Over 12.15 crore loans (amounting to ?12 lakh crore) were extended to first-time entrepreneurs.

Challenges and Structural Hurdles

Despite its massive reach, PMMY faces several critical challenges that impact its long-term economic utility:

- The "Missing Middle": 74% of loans remain in the 'Shishu' category, indicating a struggle to graduate micro-units into larger, sustainable medium enterprises.

- Sectoral Skewness: Loans are heavily concentrated in trading and services, with limited penetration in manufacturing, which limits the employment multiplier effect.

- Asset Quality: The collateral-free nature, combined with inadequate credit checks in some cases, has led to concerns regarding Non-Performing Assets (NPAs) in public sector banks.

- Credit-Absorption Deficit: A lack of financial literacy and market access means many borrowers struggle to deploy funds productively, leading to high mortality rates for micro-enterprises.

Way Forward: Moving Toward a 'Credit-Plus' Approach

To align with the vision of Viksit Bharat 2047, PMMY must evolve beyond mere credit dispensation:

- Cash-Flow Based Lending: Transitioning from collateral-based models to using Digital Public Infrastructure (DPI) like the Account Aggregator framework and GSTN for real-time credit assessment.

- Enterprise Development: Integrating PMMY with platforms like ONDC and the Skill India Mission to provide market linkages and technical handholding.

- Incentivizing Micro-Manufacturing: Offering interest subventions specifically for manufacturing units to boost Gross Fixed Capital Formation (GFCF).

- AI-Driven Monitoring: Using data analytics to track the end-use of funds, preventing the diversion of business loans toward personal consumption.

The Pradhan Mantri MUDRA Yojana has effectively dismantled the entry barriers to formal credit for India's grassroots entrepreneurs. By addressing current structural asymmetries and adopting a holistic "Credit-Plus" model, the scheme will continue to be a vital engine for inclusive growth and self-reliance (Atmanirbhar Bharat).

Pradhan Mantri Mudra Yojana (PMMY)

- 22 Sep 2025

In News:

Launched in 2015, the Pradhan Mantri Mudra Yojana (PMMY) is a flagship financial inclusion initiative of the Government of India. The scheme seeks to provide affordable credit to micro and small enterprises (MSEs) engaged in non-farm income-generating activities, thereby integrating them into the formal financial ecosystem.

Objective

- PMMY aims to “fund the unfunded” by facilitating access to institutional credit for small entrepreneurs who traditionally lack collateral or formal financial history.

- The scheme empowers these enterprises through loans provided by Public Sector Banks (PSBs), Regional Rural Banks (RRBs), Cooperative Banks, Private Banks, Foreign Banks, Micro Finance Institutions (MFIs), and Non-Banking Financial Companies (NBFCs).

Key Features and Loan Details

- Loan Amount: Up to ?10 lakh for non-farm income-generating activities across sectors such as manufacturing, processing, trading, and services.

- Eligibility: Any Indian citizen with a viable business plan for such activities can apply for a MUDRA loan through approved institutions.

- Subsidy: PMMY does not directly offer subsidies; however, if linked to other government schemes with capital subsidies, those benefits can be availed concurrently.

Categories of MUDRA Loans

|

Category |

Loan Range |

Target Group |

|

Shishu |

Up to ?50,000 |

New or micro enterprises in the early stage |

|

Kishore |

?50,000 – ?5 lakh |

Businesses seeking growth or consolidation |

|

Tarun |

?5 lakh – ?10 lakh |

Enterprises looking to expand operations |

Achievements under MUDRA 1.0

- Credit Outreach: Over ?27.75 lakh crore has been disbursed to nearly 47 crore beneficiaries, expanding access to formal credit for small entrepreneurs.

- Social Inclusion: Around 69% of loan accounts are held by women, while 51% belong to SC, ST, and OBC categories — strengthening financial inclusion and social equity.

- Employment Generation: The scheme has spurred job creation and self-employment, particularly in rural and semi-urban areas, fostering local entrepreneurship and economic decentralisation.

Vision for MUDRA 2.0

To further enhance the scheme’s reach and impact, the proposed MUDRA 2.0 envisions the following reforms:

- Wider Outreach: Greater focus on underserved rural and semi-urban regions through digital platforms and community-level facilitation.

- Financial Literacy & Mentorship: National-level programmes to improve awareness about budgeting, savings, digital transactions, and credit management to ensure sustainable enterprise growth.

- Enhanced Credit Guarantee Scheme (ECGS): A robust guarantee mechanism to minimise lender risk and encourage more credit flow to micro enterprises.

- Real-Time Monitoring Framework: Technology-driven systems for tracking disbursal, utilisation, and repayment to ensure transparency and reduce misuse.

- Impact Evaluation: Periodic socio-economic assessments to measure outcomes on income generation, employment, and business viability.

Pradhan Mantri MUDRA Yojana (PMMY)

- 08 Apr 2025

In News:

The Pradhan Mantri MUDRA Yojana (PMMY), a flagship initiative aimed at providing financial support to unfunded micro and small enterprises, has completed 10 years since its launch in 2015.

Overview of PMMY

- Objective: To offer collateral-free institutional credit to non-corporate, non-farm micro and small enterprises.

- Loan Limit: Up to ?20 lakh without any collateral.

- Implementing Institutions (MLIs):

- Scheduled Commercial Banks

- Regional Rural Banks (RRBs)

- Non-Banking Financial Companies (NBFCs)

- Micro Finance Institutions (MFIs)

Categories of MUDRA Loans

Loan Category Loan Amount Range

Shishu Up to ?50,000

Kishor ?50,000 to ?5 lakh

Tarun ?5 lakh to ?10 lakh

Tarun Plus ?10 lakh to ?20 lakh

Key Achievements (2015–2025)

- Boost to Entrepreneurship: PMMY has sanctioned over 52 crore loans amounting to ?32.61 lakh crore, catalyzing a grassroots entrepreneurship revolution.

- MSME Sector Financing: Lending to MSMEs increased significantly:

- From ?8.51 lakh crore in FY14

- To ?27.25 lakh crore in FY24

- Projected to exceed ?30 lakh crore in FY25

- Women Empowerment: 68% of Mudra beneficiaries are women, highlighting the scheme’s impact in fostering women-led enterprises.

- Social Inclusion:

- 50% of loan accounts are held by SC, ST, and OBC entrepreneurs.

- 11% of beneficiaries belong to minority communities, showcasing PMMY’s contribution to inclusive growth.