Digital Payments Revolution

- 13 Apr 2026

In News:

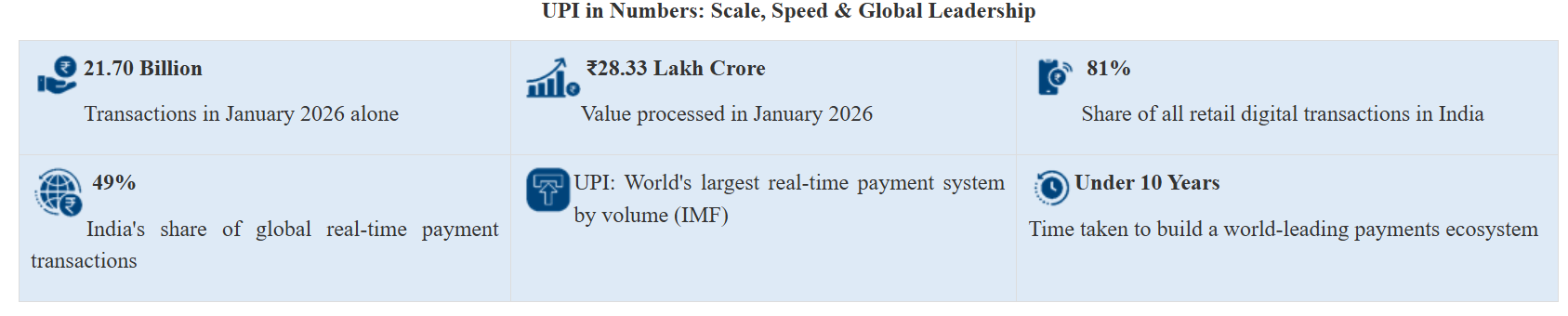

India’s financial landscape has undergone a radical metamorphosis, transitioning from a cash-heavy, urban-centric banking model to a world-leading, real-time digital infrastructure. As of January 2026, India has solidified its global leadership in fintech, processing a record 21.70 billion transactions worth ?28.33 lakh crore in a single month.

The Evolution of Payment Systems

The journey from "Queues to QR Codes" can be categorized into four distinct phases:

- The Traditional Era: Reliance on physical cash, barter, and cheques; limited to urban centers.

- Institutional Formalization (2004–2010): Introduction of RTGS and IMPS, enabling 24/7 transfers, yet restricted to the banked elite.

- The Structural Breakthrough (JAM): The combination of Jan Dhan (Access), Aadhaar (Identity), and Mobile (Connectivity) created the bedrock for mass financial inclusion.

- The UPI Radicalization (2016–Present): The launch of the Unified Payments Interface (UPI) by NPCI democratized payments via Virtual Payment Addresses (VPA) and QR codes.

The Architectural Pillars: JAM Trinity & DBT

The JAM Trinity acted as a catalyst for "Aatmanirbhar" banking:

- Pradhan Mantri Jan-Dhan Yojana: Brought the "unbanked" into the formal fold via zero-balance accounts.

- Aadhaar: Provided a digital, biometric identity for seamless authentication.

- Mobile Connectivity: Served as the primary interface for transactions.

- The DBT Effect: This framework enabled the Direct Benefit Transfer (DBT) system, ensuring government aid reaches beneficiaries without intermediaries, thereby reducing leakages and building public trust in digital systems.

UPI: The Global Gold Standard

UPI is now the world’s largest real-time payment system by volume. Key 2026 statistics highlight its dominance:

- Market Share: UPI accounts for 81% of all retail digital transactions in India.

- Global Footprint: India contributes 49% of total global real-time payment transactions.

- Institutional Growth: The network has expanded from 216 banks (2021) to 691 banks (2026).

- International Reach: Operational or linked in countries including France, UAE, Singapore, Bhutan, Nepal, Sri Lanka, Mauritius, and Qatar.

Beyond Payments: Socio-Economic Significance

- Financial Inclusion: Dissolves the urban-rural divide; village mandis and street vendors now transact with the same speed as metropolitan hubs.

- Formalization of Credit: Digital footprints allow informal workers (auto drivers, domestic help) to access formal credit, insurance, and pre-approved credit lines.

- Economic Efficiency: Reduces the heavy "cost of cash" (printing, storage, transport) and speeds up the velocity of money.

- Enhanced Security: Effective April 1, 2026, the RBI mandated Multi-layer/Two-factor authentication (biometrics, secure tokens, and PINs) to combat digital fraud.

Critical Challenges

Despite its success, the ecosystem faces several hurdles:

- Cybersecurity: Sophisticated phishing and identity theft remain persistent threats.

- Digital Literacy: A gap exists in the deep-tech understanding required to resolve transaction failures among first-time rural users.

- Infrastructure Load: Processing 20 billion monthly transactions puts immense pressure on bank servers and the NPCI central switch.

- Data Privacy: The massive volume of financial data necessitates a robust legal framework to prevent commercial misuse.

Way Forward: The Road to 2030

To sustain this momentum, the focus must shift toward:

- Product Diversification: Scaling UPI Lite (small-value offline payments) and UPI AutoPay (recurring bills).

- Credit Integration: Leveraging "Credit on UPI" to turn a payment tool into a comprehensive financial services platform.

- Deep-Rural Outreach: Ensuring 100% connectivity in remote regions to digitize the "last mile" of the economy.

- Cross-Border Dominance: Positioning UPI as a cheaper, faster alternative for global remittances.