NITI Aayog’s “Future of India’s Semiconductor Industry” Roadmap

- 01 Jun 2026

In News:

Recognising semiconductors as the foundation of national security, digital sovereignty, economic resilience, AI infrastructure, defence systems, telecommunications, healthcare technologies, automobiles, and advanced manufacturing, NITI Aayog’s Frontier Tech Hub has released India’s first comprehensive 10-year roadmap titled “Future of India’s Semiconductor Industry.” The roadmap envisions building a USD 120–150 billion domestic semiconductor value chain by 2035, transforming India from a major chip consumer into an indispensable global semiconductor player.

Why the Roadmap is Important

India currently faces extreme strategic vulnerability, with 90–95% of its semiconductor demand met through imports. Between FY17 and FY25, semiconductor imports cost the country nearly USD 150 billion, and if current trends continue, the annual import bill could rise to USD 240 billion by 2035. At the same time, India’s domestic semiconductor market is projected to reach USD 200 billion by 2035, driven by rapid growth in electronics manufacturing, electric vehicles (EVs), AI systems, data centres, telecom equipment and digital infrastructure.

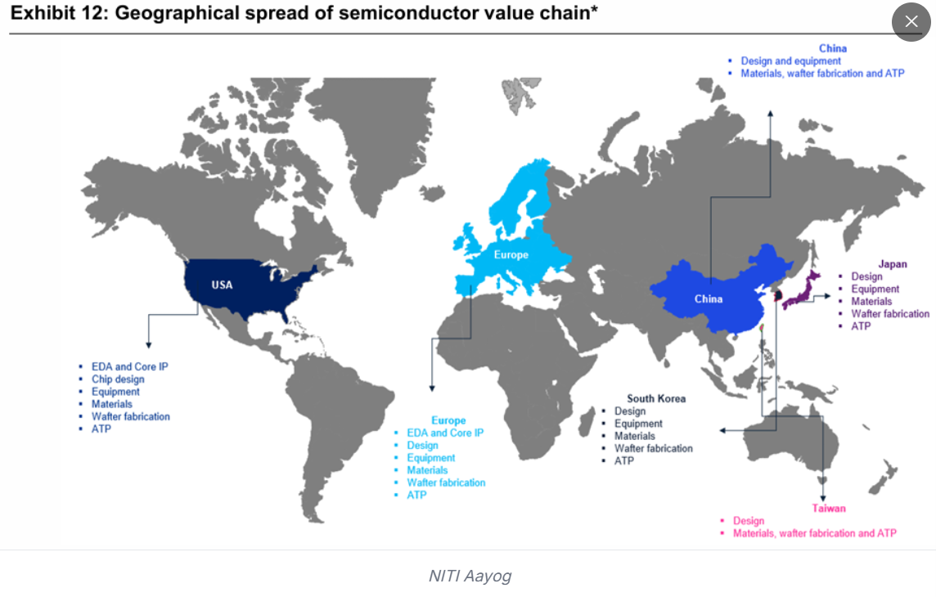

India’s Strategic Approach: Beyond the Wafer Race

Instead of competing directly in the highly capital-intensive cutting-edge wafer fabrication race, the roadmap advocates a “More-than-Moore” strategy, focusing on areas where India can build sustainable competitive advantages:

- Advanced Packaging and OSAT (Outsourced Semiconductor Assembly and Test)

- Compound Semiconductors

- Wide-Bandgap Materials (SiC and GaN)

- Advanced Semiconductor Design and Design IP

- AI-Native Chip Design

The roadmap aims to position India among the top global destinations for advanced packaging and OSAT, emerge as a major supplier of wide-bandgap semiconductors, and create more than 100 advanced semiconductor design IPs by 2035.

Key Strengths and Opportunities

India possesses several structural advantages:

- Houses 20% of the global semiconductor design workforce.

- Benefits from the China 1 strategy and global supply-chain diversification.

- Can leverage growing partnerships with the US, Japan and the European Union.

- Rising EV adoption creates demand for SiC and GaN power devices.

- Backed by India Semiconductor Mission (ISM) 2.0, which shifts focus from ecosystem creation to ecosystem deepening.

Major Challenges

Despite the opportunity, significant barriers remain:

- USD 135–180 billion investment requirement over the next decade.

- A modern semiconductor fab requires over USD 5 billion, while leading-edge facilities can exceed USD 15 billion.

- Long gestation periods of 4–5 years before production begins.

- Shortage of specialized fabrication, materials and cleanroom talent.

- High requirements of ultra-pure water and uninterrupted electricity.

- Strong market dominance of established East Asian semiconductor ecosystems.

Five Pillars of the Roadmap

The strategy is built around five mutually reinforcing pillars:

- Pioneering Frontier R&D and Design IP

- Policy and Investment Mobilisation

- Production through Advanced Packaging and Compound Semiconductors

- People and Talent Development

- Partnerships with Trusted Nations and Global Industry

The roadmap marks India's transition from ecosystem creation to ecosystem deepening, focusing on design leadership, advanced packaging, compound semiconductors, talent development, R&D and trusted global partnerships. By leveraging its design strengths and targeting high-value segments rather than the traditional wafer race, India seeks to capture 10–13% of the global semiconductor market by 2035 while strengthening its technological sovereignty and advancing the vision of Viksit Bharat 2047.