Withholding Tax on FPIs

- 18 May 2026

In News:

The Government of India is considering a sharp reduction in the Withholding Tax (WHT) rate on Foreign Portfolio Investors (FPIs) from 20% back to the previous concessional rate of 5%. This move follows the expiration of the concessional window under Section 194LD of the Income Tax Act in mid-2023, which effectively caused the rate to revert to 20%, positioning India as a high-tax jurisdiction for global bond investors.

The primary trigger for this policy reconsideration is the need to arrest capital outflows that have eroded India’s foreign exchange reserves by nearly USD 38 billion since March 2026, driven by heightened geopolitical uncertainties (such as conflicts in West Asia) and a sharp surge in global crude oil prices.

Understanding Withholding Tax (WHT)

Withholding Tax, analogous to Tax Deducted at Source (TDS) under domestic tax law, is a mechanism where the payer of an income item deducts tax at the source before remitting the remaining net balance to the recipient.

International Withholding Tax

This applies specifically when a payer within one country makes payments (such as interest, dividends, or royalties) to a non-resident recipient in another country. It serves as a vital tool for source-based taxation, ensuring advance revenue collection and reducing the risk of cross-border tax evasion.

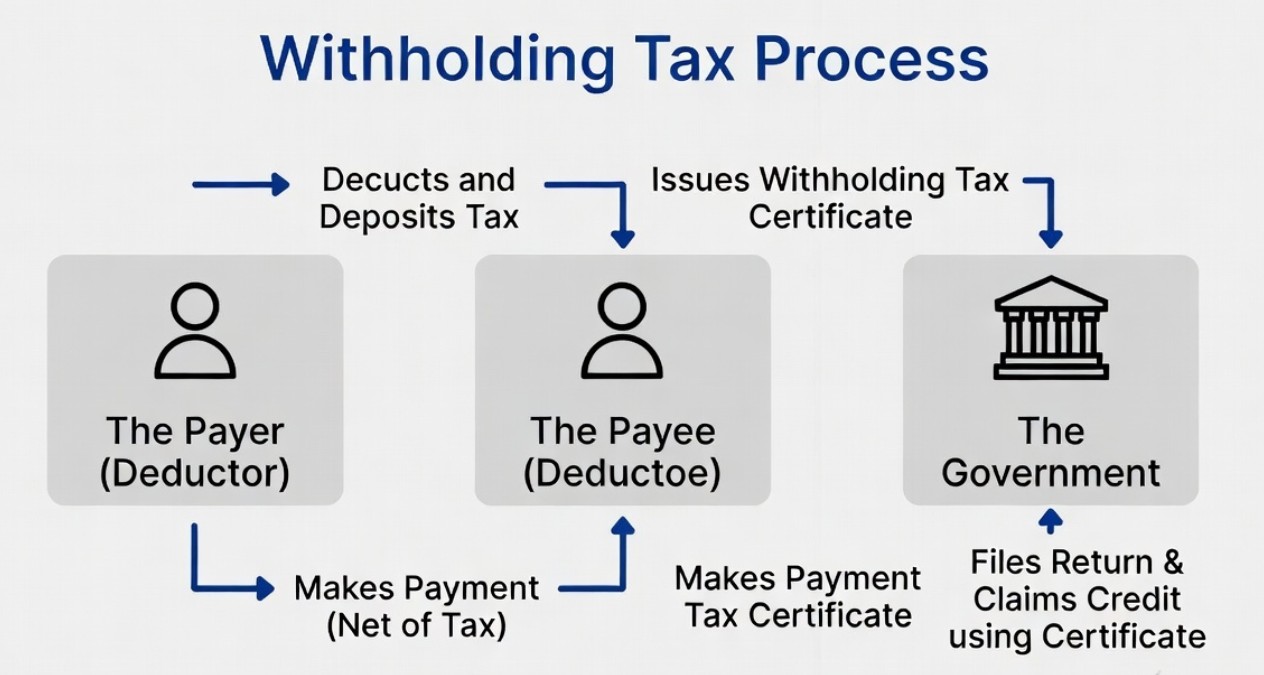

The Core Mechanism (As Illustrated Above):

- The Payer (Deductor): Deducts the statutory tax percentage from the gross amount due and deposits this tax directly with the Government.

- The Payee (Deductoe): Receives the net payment (net of tax) alongside a Withholding Tax Certificate issued by the payer.

- The Government: Receives the advance tax collection. The Payee subsequently files a tax return in India and claims tax credits using the issued certificate.

General WHT Classification by Income Type

WHT spans across several distinct asset and income streams, each governed by independent threshold limits and criteria:

- Salaries: Deducted monthly by employers based on progressive annual income tax slabs.

- Interest Income: Banks deduct tax at source on fixed deposits and other debt instruments once earnings cross predefined annual thresholds.

- Professional & Technical Fees: Applied to payments made to freelance contractors, consultants, legal experts, or engineers.

- Rent & Royalties: Imposed on high-value commercial or residential lease payments and intellectual property payouts.

- Dividends: Companies withhold a designated percentage when distributing corporate profits to domestic or foreign shareholders.

Economic Implications: High WHT vs. The Concessional 5% Rate

Challenges of the 20% WHT Regime (Yield Compression & Capital Flight)

- Reduction in Net Yields: A 20% WHT directly reduces the risk-adjusted post-tax returns for FPIs on government securities (G-Secs) and corporate bonds, weakening the power of long-term compounding.

- Liquidity & Transactional Bottlenecks: It locks up foreign investor capital at the source, constraining immediate capital available for reinvestment.

- High Compliance and Regulatory Friction: To mitigate the high 20% rate, FPIs are forced to seek relief via Double Taxation Avoidance Agreements (DTAAs). This process involves complex, paperwork-heavy administrative processes to claim tax credits in their home jurisdictions.

- Delayed Index Integration: Higher interest tax structures act as an operational deterrent, dragging down India's competitive edge just as the nation integrates into major global bond indices.

Macroeconomic Significance of Slashing WHT to 5%

- Boosting Forex Inflows: Restoring the 5% concessional rate is projected to unlock USD 45–50 billion of stable inflows over 2 years from patient, long-term institutional capital, such as global pension funds, sovereign wealth funds, and endowments.

- Stabilizing the Indian Rupee: Enhanced FPI debt inflows will help defend against external vulnerabilities, counter heavy capital flight, and rebuild the USD 38 billion cushion lost from forex reserves.

- Deepening Sovereign Debt Markets: Lowering tax frictions satisfies a long-standing demand of global investors, boosting liquidity in the Indian sovereign debt market and smoothing India’s inclusion and weight scaling in global bond indices.

- Reducing Sovereign Borrowing Costs: Increased foreign demand for Indian government securities compresses domestic bond yields, lowering the cost of borrowing for the government and supporting fiscal management.