11 Years of Jan Suraksha Schemes

- 10 May 2026

In News:

On May 9, 2026, India celebrated the 11th anniversary of its three flagship Jan Suraksha (Social Security) Schemes. Launched in 2015, these initiatives—Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY), Pradhan Mantri Suraksha Bima Yojana (PMSBY), and Atal Pension Yojana (APY)—were designed to bridge the massive gap in insurance and pension coverage, particularly for the unorganized sector and vulnerable populations.

By leveraging the "JAM Trinity" (Jan Dhan, Aadhaar, and Mobile), these schemes have successfully transitioned India from a country with negligible social security to one with a digitized, high-volume, and affordable safety net.

Overview of the Triple Pillar Framework

The Jan Suraksha ecosystem is built on three distinct but complementary products that address the lifecycle risks of death, disability, and old age.

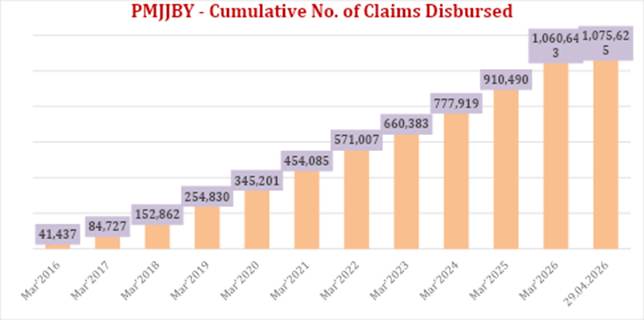

1. Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY): Life Cover

- Nature: A pure-term, one-year life insurance plan renewable annually.

- Coverage: Provides ?2 lakh in the event of death due to any reason.

- Eligibility: Bank or Post Office account holders aged 18 to 50 years.

- Affordability: The premium is set at ?436 per annum (approximately ?1.20 per day), deducted via a seamless auto-debit facility.

2. Pradhan Mantri Suraksha Bima Yojana (PMSBY): Accidental Cover

- Nature: A low-cost accidental death and disability insurance scheme.

- Coverage: Offers ?2 lakh for accidental death or total permanent disability, and ?1 lakh for permanent partial disability.

- Eligibility: Available to account holders in the 18 to 70 years age bracket.

- Affordability: At just ?20 per annum, it remains one of the cheapest insurance products globally.

3. Atal Pension Yojana (APY): Retirement Security

- Nature: A guaranteed pension scheme targeted at the unorganized sector to provide financial stability in old age.

- Benefits: A guaranteed monthly pension ranging from ?1,000 to ?5,000 starting at age 60.

- Eligibility: Open to bank account holders aged 18 to 40 years who are not income tax payers.

- Spousal Protection: After the subscriber’s death, the pension continues for the spouse. Subsequently, the entire accumulated corpus is returned to the nominee.

Achievements and Impact Analysis (2015–2026)

After eleven years, the scale of these schemes reflects a significant shift in India’s financial landscape:

- Massive Enrolment: The cumulative enrolment has crossed a staggering 94.56 crore, indicating high public trust. PMSBY alone accounts for over 58.09 crore enrolments.

- Financial Safety Net: The schemes have provided tangible relief during crises. For instance, PMJJBY has settled claims worth over ?21,512.50 crore, supporting more than 10.7 lakh bereaved families.

- Gender and Inclusive Growth: Gender inclusivity has been a standout feature; nearly 49% of subscribers under the Atal Pension Yojana are women, promoting financial autonomy for females.

- Integration with PMJDY: The schemes have successfully tapped into the Pradhan Mantri Jan Dhan Yojana (PMJDY) ecosystem, bringing over 19.30 crore of the country's poorest account holders under the protective umbrella of accidental insurance.

- Securing the Future: APY has empowered over 9.04 crore individuals to build a formal retirement corpus, essential for a country with a growing elderly population.

Critical Challenges in Implementation

Despite remarkable success, several hurdles persist in the "last mile" of social security:

- Persistence Issues: Maintaining the "auto-debit" success rate is difficult. If account holders fail to maintain a balance of ?436 or ?20, the insurance cover lapses, often without the subscriber realizing it.

- Literacy and Claim Errors: There remains confusion between "accidental" and "natural" death. Many families attempt to file claims for natural deaths under the PMSBY accidental policy, leading to rejections and distress.

- Inflationary Pressures: The ?2 lakh sum assured, fixed in 2015, has seen its purchasing power eroded by inflation over the last decade, potentially making the payout insufficient for a family’s long-term survival in 2026.

- Awareness in Remote Belts: While enrollment is high, awareness of the procedure to claim benefits is still low in tribal and deep-rural pockets, where the "silent grief" of lost benefits often goes unrecorded.

The Road Ahead: Jan Suraksha 2.0

To evolve into a truly universal system, the next phase of these schemes must focus on:

- Dynamic Coverage: Periodically reviewing and increasing the sum assured (e.g., from ?2 lakh to ?5 lakh) to keep pace with the rising cost of living.

- Digital Claim Settlement: Enhancing the Jan Suraksha Portal to allow real-time, paperless claim filing for beneficiaries, reducing their dependence on bank intermediaries.

- Incentivized Persistence: Developing a "No-Claim Bonus" or loyalty reward for subscribers who maintain uninterrupted auto-debits for over a decade.

- Integrated Bundling: Moving toward a Unified Jan Suraksha Product that offers life, accident, and pension benefits through a single enrollment process, simplifying the experience for the semi-literate population.