Reproductive Rights of Women with Intellectual Disabilities

- 27 Jun 2026

In News:

The Karnataka High Court recently permitted a total abdominal hysterectomy (surgical removal of the uterus) for a 23-year-old woman with severe intellectual and developmental disabilities after a medical board concluded that she lacked the capacity to provide informed consent and that the procedure was medically necessary. The judgment has once again highlighted the legal and ethical issues surrounding consent, reproductive autonomy, and the rights of persons with disabilities.

The Core Legal Issue: Informed Consent

Informed consent is a fundamental principle of medical ethics and law. Before any major medical procedure, a patient must voluntarily understand the nature, purpose, risks, and consequences of the treatment and provide free consent.

A legal dilemma arises when a person with severe intellectual disability lacks the cognitive capacity to make such decisions. In such cases, neither doctors nor family members can unilaterally authorise irreversible medical procedures. Judicial intervention becomes necessary to ensure that the person's rights and welfare are protected.

Doctrine of Parens Patriae

Courts exercise the doctrine of Parens Patriae (Latin for "parent of the nation") while dealing with individuals who are incapable of protecting their own interests.

Under this doctrine, the court acts as a guardian and determines what would serve the best interests of the individual by considering medical evidence, dignity, bodily integrity, and overall welfare. The objective is not to substitute the person's autonomy unnecessarily but to protect vulnerable individuals where informed decision-making is impossible.

Legal Framework

The principal legislation governing such situations is the Rights of Persons with Disabilities Act, 2016 (RPwD Act).

Section 10 of the Act explicitly prohibits subjecting any person with a disability to a medical procedure resulting in infertility without their free and informed consent. The provision was enacted to prevent the historical practice of forced sterilisation of women with intellectual disabilities, often carried out under the guise of convenience or protection.

Consequently, any departure from this principle requires strict judicial scrutiny.

Supreme Court Guidelines on Hysterectomies

In Dr. Narendra Gupta v. Union of India (2023), the Supreme Court addressed the growing incidence of unnecessary hysterectomies, particularly among women from economically weaker sections.

The Court held that such practices violate the Right to Health under Article 21 and directed all States and Union Territories to implement the Union Health Ministry's 2022 Guidelines on Preventing Unnecessary Hysterectomies. It also ordered the establishment of monitoring committees at the national, state, and district levels and directed action, including blacklisting, against hospitals performing medically unjustified hysterectomies without informed consent.

Abortion and Intellectual Disability

The legal position regarding abortion presents a distinct challenge.

Under the Medical Termination of Pregnancy (MTP) Act, 1971, a guardian may consent to abortion only in the case of a woman suffering from mental illness.

However, the law does not extend this provision to women with intellectual disabilities. Their own consent remains legally mandatory, even where cognitive capacity is severely impaired. This has resulted in several complex judicial interventions involving pregnancies arising from sexual assault.

Important Judicial Decisions

Some landmark judgments shaping this area include:

- Suchita Srivastava v. Chandigarh Administration (2009): The Supreme Court held that reproductive autonomy is part of Article 21, and clarified that intellectual disability is distinct from mental illness.

- Z v. State of Bihar (2017): The Court awarded compensation to an HIV-positive rape survivor after unlawful denial of abortion due to insistence on third-party consent.

- Orissa High Court (2020): Refused termination of an advanced pregnancy on medical grounds but directed compensation and comprehensive postnatal care.

- Gujarat High Court (2024): Permitted termination of a 28-week pregnancy of a minor tribal girl with intellectual disability after medical experts concluded that continuation would seriously endanger her physical and psychological well-being.

Autonomy versus Best Interests

The legal debate centres on balancing two equally important constitutional principles.

On one hand is reproductive autonomy, recognised as part of the Right to Life and Personal Liberty under Article 21 and reinforced by the United Nations Convention on the Rights of Persons with Disabilities (UNCRPD), to which India is a signatory.

On the other hand is the best interests principle, which courts invoke when an individual genuinely lacks the capacity to make informed decisions. Judicial intervention seeks to ensure that any restriction on personal autonomy is limited, proportionate, and solely aimed at protecting the person's health, dignity, and welfare.

Significance

The Karnataka High Court's decision highlights the complex intersection of constitutional rights, disability law, medical ethics, and reproductive justice. Indian courts have consistently sought to balance the autonomy of persons with disabilities with the duty to protect those who are unable to make informed decisions independently. The evolving jurisprudence reflects a rights-based approach that prioritisesdignity, bodily integrity, informed consent, and judicial oversight, while ensuring that irreversible medical procedures are undertaken only when demonstrably necessary and in the individual's best interests. The issue remains significant for governance, healthcare regulation, disability rights, and the protection of fundamental rights under Article 21.

Western Ghats Ecologically Sensitive Area (ESA)

- 26 Jun 2026

In News:

The Western Ghats Ecologically Sensitive Area (ESA) notification, currently valid until July 2026, has once again come under focus as six State governments continue to oppose the finalisation of ESA boundaries. The issue reflects the ongoing challenge of balancing ecological conservation with developmental needs.

Why are the Western Ghats Important?

The Western Ghats are a nearly continuous mountain range stretching about 1,500 km along India's western coast across Gujarat, Maharashtra, Goa, Karnataka, Kerala, and Tamil Nadu. Recognised as one of the world's eight "hottest hotspots" of biodiversity and a UNESCO World Heritage Site, they harbour thousands of endemic species of flora and fauna.

Beyond biodiversity, the Ghats play a crucial role in India's ecological security. They intercept the southwest monsoon, receive heavy rainfall, and serve as the source of major peninsular rivers such as the Godavari, Krishna, Cauvery, and Periyar, supporting agriculture, drinking water, hydropower generation, and livelihoods for millions.

Unlike many protected ecosystems, the Western Ghats are also densely populated and support plantation agriculture, including coffee, pepper, cardamom, tea, cinnamon, mango, and jackfruit, making conservation particularly challenging.

What is an Ecologically Sensitive Area (ESA)?

An Ecologically Sensitive Area (ESA) is a region notified by the Central Government under the Environment (Protection) Act, 1986, to protect environmentally fragile ecosystems from activities that could cause irreversible ecological damage.

Within an ESA, environmentally harmful activities such as:

- Mining and quarrying

- Red-category polluting industries

- Thermal power plants

- Large-scale construction and township projects

are either prohibited or subject to strict regulation to ensure sustainable development.

Evolution of the Western Ghats ESA Proposal

The demand for protecting the Western Ghats led to the constitution of the Western Ghats Ecology Expert Panel (WGEEP) under Madhav Gadgil in 2010.

The Gadgil Committee (2011) recommended that the entire Western Ghats (1,29,037 sq km) be declared an Ecologically Sensitive Area with stringent restrictions on developmental activities. However, the recommendations faced widespread opposition from State governments and local communities due to concerns over livelihoods and economic development.

Subsequently, the Government appointed a High-Level Working Group under Dr. K. Kasturirangan in 2012 to review the Gadgil Report.

The Kasturirangan Committee (2013) adopted a more balanced approach. It distinguished between 'natural landscapes' and 'cultural landscapes', recognising that nearly 60% of the Western Ghats had already been modified through agriculture, plantations, and settlements. The committee therefore recommended that only about 60,000 sq km of ecologically intact natural landscapes be notified as ESA while permitting sustainable activities in human-dominated areas.

Current Status

Based on the Kasturirangan Report, the Centre issued its first draft notification in 2014, proposing 56,825.7 sq km as the Ecologically Sensitive Area.

Since then, the notification has undergone several revisions owing to objections from the six affected States. The latest draft notification, issued in July 2024, remains valid until July 2026.

A significant feature of the latest notification is the proposal to finalise ESA boundaries on a phased, State-wise basis, allowing implementation in States where consensus has been reached rather than waiting for unanimous approval.

Why are States Opposing the ESA?

The principal concern of the States is that ESA notification could adversely affect economic activities and local livelihoods.

Major concerns include:

- Restrictions on mining, quarrying, industries, and infrastructure projects.

- Possible impact on plantation agriculture and rural livelihoods.

- Fear of reduced developmental opportunities in notified villages.

- Demands for exclusion of inhabited and cultivated areas from the proposed ESA.

While Karnataka has rejected the Kasturirangan recommendations entirely, Kerala has sought exclusion of several plantation-dominated villages, particularly in the Cardamom Hills of Idukki. Maharashtra, Goa, Tamil Nadu, and Gujarat have also proposed modifications to the notified boundaries.

Recent Developments

In 2022, the Central Government constituted an expert committee under Sanjay Kumar, former Director General of Forests, to examine State-specific concerns and reconcile differences using satellite imagery, revenue records, and field verification.

The committee is also examining the possibility of providing financial incentives to States through mechanisms such as Payments for Ecosystem Services (PES), under which States protecting ecologically valuable forests could receive compensation for ecosystem services such as water conservation, biodiversity protection, and carbon sequestration.

Upgradation of India’s Statistical Databases

- 25 Jun 2026

In News:

India has undertaken a comprehensive overhaul of its key statistical databases after receiving a 'C' grade—the second-lowest rating—from the International Monetary Fund (IMF) in November 2025 for the quality of its national accounts statistics. The reforms aim to improve the accuracy, timeliness, representativeness, and reliability of data used for measuring economic growth, industrial output, and inflation.

Why Was the Overhaul Necessary?

India's major statistical indicators were based on outdated base years, making them increasingly unrepresentative of the country's evolving economy. The GDP, Gross Value Added (GVA), and Index of Industrial Production (IIP) were still based on 2011–12, while the Wholesale Price Index (WPI) also used 2011–12 and the Consumer Price Index (CPI) used 2012 as their base years.

As household consumption patterns changed significantly over the past decade, older indices continued to assign weight to obsolete products such as DVD players, VCRs, tape recorders, and cassettes, while failing to adequately capture emerging expenditures like online streaming services, CNG/PNG, rural house rent, and digital communication services. Such outdated databases reduced the accuracy of economic indicators and affected evidence-based policymaking.

Why Accurate Statistical Data Matters

Reliable statistics form the foundation of economic governance. They are essential for:

- Measuring real GDP and economic growth.

- Inflation targeting by the Reserve Bank of India's Monetary Policy Committee.

- Calculation of Dearness Allowance (DA) and Dearness Relief (DR).

- Fiscal planning, budgeting, and welfare policy formulation.

- Enhancing the credibility of India's macroeconomic data globally.

Key Reforms in National Accounts (GDP/GVA)

The base year for GDP and GVA has been revised from 2011–12 to 2022–23, making national income estimates more reflective of the present-day economy.

The revised series introduces significant methodological improvements. The Double Deflator Method has been adopted for agriculture and manufacturing, wherein input and output prices are adjusted separately to generate a more accurate estimate of real economic growth. Another important reform is the segregation of multi-activity enterprises, under which the output of companies engaged in multiple sectors is now allocated proportionately across those sectors instead of being assigned entirely to a single principal activity.

The revised estimates also incorporate richer datasets such as Goods and Services Tax (GST) information and the Periodic Labour Force Survey (PLFS), thereby improving data quality and reducing statistical discrepancies.

Changes in the Index of Industrial Production (IIP)

The IIP, which measures monthly industrial performance, has also adopted 2022–23 as the new base year.

The revised index expands its coverage by including activities such as gas supply, water supply, sewerage, and waste management, in addition to manufacturing, mining, and electricity. Greater product-level detail has also been introduced by separately tracking renewable and non-renewable electricity generation and various categories of minerals.

The number of products covered has increased from 839 to 1,042, while item groups have expanded from 407 to 463, making industrial measurement more comprehensive.

Reforms in Inflation Measurement

Consumer Price Index (CPI)

The base year has been updated to 2024, with weights derived from the Household Consumption Expenditure Survey (HCES) 2023–24.

The revised CPI reflects changing consumption behaviour by:

- Expanding categories from 6 to 12.

- Increasing the number of goods and services from 299 to 358.

- Including rural house rent, online streaming services, CNG, PNG, and improved measurement of transport and communication services.

- Removing obsolete products such as VCRs, DVD players, radios, tape recorders, and cassettes.

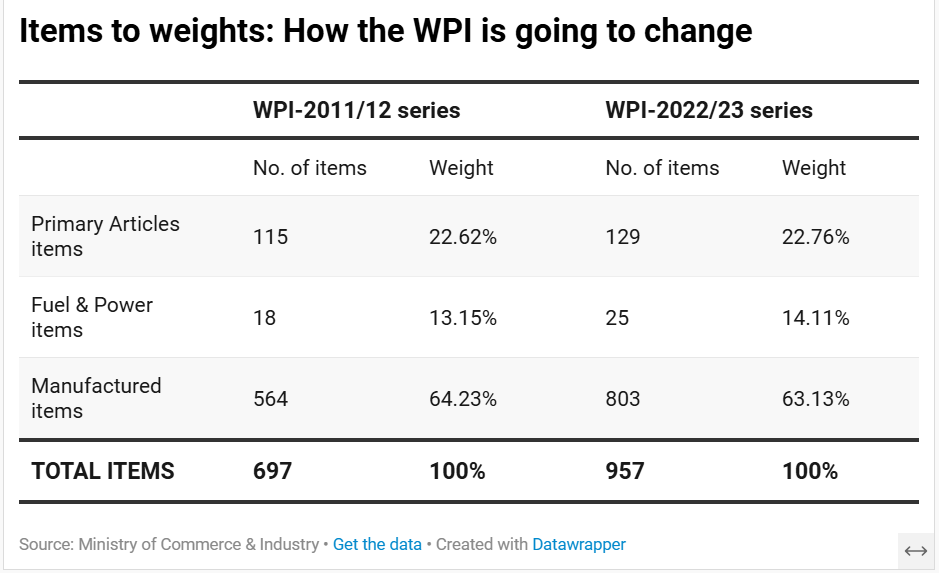

Wholesale Price Index (WPI)

The base year has been revised to 2022–23, while the number of commodities has increased from 697 to 957. Commodity classification has also been rationalised, with crude petroleum and natural gas now placed under the Fuel and Power category.

Producer Price Index (PPI): A New Addition

In June 2026, the government introduced the Producer Price Index (PPI) to provide a more accurate measure of producer-level inflation.

Unlike the WPI, the PPI:

- Separately measures input costs and output prices.

- Excludes indirect taxes and transport costs.

- Covers both goods and services, making it a more comprehensive indicator of production costs.

The government has indicated that the Wholesale Price Index (WPI) will be phased out over the next five years, after which the CPI and PPI will become India's principal inflation indices, bringing the country's statistical system closer to international best practices.

Significance

The overhaul of India's statistical databases marks a major step towards strengthening the country's statistical architecture. Updated base years, improved methodologies, expanded data coverage, and the introduction of the Producer Price Index will make economic indicators more representative of current realities and improve the quality of policymaking. These reforms are expected to enhance the credibility of India's macroeconomic statistics, facilitate better inflation and growth measurement, and align the country's statistical framework with global standards.

India's Space Sector Transformation

- 24 Jun 2026

In News:

The Press Information Bureau (PIB) released a comprehensive report highlighting India's transformation into a leading global space power over the past twelve years. Anchored in the vision of Aatmanirbhar Bharat and Viksit Bharat 2047, India’s space programme has evolved from a government-driven scientific initiative into a dynamic ecosystem integrating strategic security, commercial innovation, citizen welfare, and international cooperation.

India’s Evolving Space Architecture

India's space sector has transitioned from a closed, state-centric model to an integrated public-private ecosystem. Beyond scientific exploration, space technology today supports governance, agriculture, disaster management, navigation, communication, climate monitoring, and economic growth.

Institutional reforms have encouraged private participation while maintaining ISRO’s leadership in strategic and frontier technologies, thereby strengthening India's position in the global space economy.

Major Achievements

India's commercial space sector has witnessed remarkable expansion in recent years. NewSpace India Limited (NSIL), the commercial arm of ISRO, increased its revenues from ?321.77 crore in FY 2021–22 to ?3,246.09 crore in FY 2024–25, reflecting nearly a tenfold rise. The domestic space startup ecosystem has grown from a single registered startup in 2014 to over 400 startups by February 2026, attracting private investments exceeding USD 500 million.

India has also emerged as a reliable launch service provider, successfully launching 399 foreign satellites between 2014 and March 2026, compared to only 35 launches before 2014. Further, Aditya-L1, India's first solar observatory, has already released over 27 terabytes of scientific data, contributing significantly to global solar research.

Institutional and Policy Reforms

The transformation has been supported by significant policy reforms aimed at liberalising the sector.

The Indian Space Policy, 2023 formally opened satellite manufacturing, launch services, downstream applications, and space-based services to private players, ending the state's exclusive monopoly.

The establishment of IN-SPACe (Indian National Space Promotion and Authorization Centre) as an autonomous regulator has created a single-window mechanism for authorising and promoting private space activities. It has already facilitated the transfer of 71 ISRO technologies to domestic industries.

NewSpace India Limited (NSIL) has emerged as the principal commercial entity responsible for marketing ISRO technologies, satellite services, and launch vehicles through public-private partnerships.

To enhance investor confidence, the government introduced the Norms, Guidelines and Procedures (NGP), 2024, providing a predictable regulatory framework for private participation.

Further, the liberalisedFDI policy now permits:

- Up to 100% automatic route in manufacturing of space components.

- Up to 74% FDI in satellite operations.

- Up to 49% FDI in launch vehicles and spaceports.

India has also strengthened its strategic autonomy through NavIC (Navigation with Indian Constellation), providing indigenous satellite-based navigation services across India and nearly 1,500 km beyond its borders.

Future Space Missions

India has outlined an ambitious roadmap for becoming a major spacefaring nation.

The Gaganyaan Mission will place up to three Indian astronauts into Low Earth Orbit using indigenous technologies.

The Bharatiya Antariksh Station (BAS) is planned as India's first modular space station, with the initial module (BAS-01) targeted for launch by 2028.

The Chandrayaan-4 Mission, expected in 2027, aims to achieve India's first lunar sample return mission, while Chandrayaan-5 (LUPEX), in collaboration with JAXA, will explore water ice deposits near the Moon's south pole.

India has also approved the Venus Orbiter Mission, scheduled for launch in 2028, to study Venus' atmosphere and geological evolution.

In the climate domain, the TRISHNA Mission, jointly developed with France's CNES, will provide high-resolution thermal imaging for monitoring crop water stress, urban heat islands, and climate change.

To reduce launch costs, ISRO is developing the Next Generation Launch Vehicle (NGLV) capable of placing 30 tonnes into Low Earth Orbit, along with reusable launch technologies.

Challenges

Despite remarkable progress, India's share in the global space economy remains modest at 2–3%, considerably below its scientific potential.

Scaling advanced laboratory technologies into large-scale commercial manufacturing remains a significant challenge. Human spaceflight technologies, reusable launch systems, advanced propulsion, and planetary exploration demand sustained investments and technological innovation.

Additionally, expanding space infrastructure—including new launch facilities, reusable vehicles, and orbital stations—requires consistent long-term financial commitments.

Way Forward

India should accelerate the operationalisation of the Kulasekarapattinam Spaceport and the Third Launch Pad at Sriharikota to enhance launch capacity.

Greater integration of NavIC into smartphones, automobiles, logistics, and strategic sectors will strengthen indigenous positioning capabilities.

The government should further deepen public-private partnerships, encourage domestic manufacturing of space hardware, strengthen research in reusable launch vehicles and human spaceflight technologies, and expand international collaborations in planetary exploration and satellite services.

Achieving the national target of an 8% share of the global space economy by 2030 will require a strong innovation ecosystem, supportive regulation, skilled human resources, and sustained investments.

Conclusion

India's space programme has entered a transformative phase by successfully combining scientific excellence with commercial dynamism. Institutional reforms, private sector participation, indigenous technologies, and ambitious deep-space missions have positioned India as an emerging global space power. Continued investments in innovation, infrastructure, and international cooperation will be crucial for realizing the vision of Viksit Bharat 2047 and establishing India as a leading force in the global space economy.

Supreme Court Recognises Right to Walk as a Fundamental Right

- 23 Jun 2026

In News:

In a landmark judgment, the Supreme Court of India held that the right to walk on safe and demarcated footpaths is a Fundamental Right under Part III of the Constitution. The Court ruled that pedestrian rights take precedence over the movement of motorised vehicles and called for a comprehensive legal framework to safeguard pedestrians.

Background

The judgment arose from the death of a five-year-old boy, who was fatally hit by a tanker while walking to school with his father. The accident occurred at a location lacking both a footpath and pedestrian crossing. While enhancing compensation from ?4.70 lakh to ?11.44 lakh, the Supreme Court used the case to address the broader issue of pedestrian safety and urban planning.

Constitutional Recognition of the Right to Walk

The Court held that the right to walk is an integral part of several Fundamental Rights guaranteed under the Constitution:

- Article 19(1)(a) – Freedom of speech and expression.

- Article 19(1)(b) – Freedom of peaceful assembly.

- Article 19(1)(c) – Freedom to form associations.

- Article 19(1)(d) – Freedom of movement.

- Article 21 – Right to life and personal liberty.

The Court observed that walking is the most basic and universal mode of human movement, predating motorised transport, and therefore access to safe footpaths is a constitutional entitlement.

Key Observations

The Supreme Court declared that wherever a road exists, there is a corresponding legal obligation to provide safe pedestrian infrastructure. It placed responsibility on Urban Development Authorities, Municipal Corporations, Municipalities, and Panchayats to construct, demarcate, maintain, and protect footpaths from encroachment.

The judgment emphasized that pedestrian rights take precedence over the convenience of motorised vehicles, criticizing automobile-centric urban planning that marginalizes walkers. Roads and public spaces, the Court noted, must serve all citizens rather than only vehicle users.

The Court further recognized that citizens suffering injury or loss due to the absence or poor maintenance of footpaths can seek constitutional remedies, restitution, and compensation, independent of relief available under the Motor Vehicles Act, 1988.

Need for Legal and Institutional Reforms

The Court observed that while the Motor Vehicles Act, 1988 regulates drivers and vehicles, it does not adequately recognize pedestrian rights. It urged the government to enact a dedicated law on pedestrian rights, clearly define institutional responsibilities, establish effective grievance redressal mechanisms, and create a full-time regulatory authority for planning, monitoring, and enforcing pedestrian infrastructure standards.

The judgment also highlighted the broader democratic significance of walking, describing it as a means of expression, assembly, association, and political participation, closely linked to India's constitutional values and the spirit of the freedom movement.

Significance

The ruling transforms access to safe footpaths from a governance objective into an enforceable constitutional obligation. It strengthens the rights-based approach to urban planning, promotes inclusive mobility, and aligns with sustainable, people-centric city development by prioritizing the safety and dignity of pedestrians.

RBI Surplus Transfer & the Economic Capital Framework (ECF)

- 22 Jun 2026

In News:

The Reserve Bank of India (RBI) approved a record surplus transfer of ?2.87 lakh crore to the Union Government for FY 2025–26, the highest ever. The transfer has intensified debate over the RBI's expanding fiscal role, central bank independence, and implications for fiscal federalism.

Background

The RBI earns income primarily from interest on government securities, foreign exchange operations, returns on foreign assets (including gold), and reserve management activities. After meeting operational expenses and maintaining prescribed financial buffers under the Economic Capital Framework (ECF), the remaining surplus is transferred to the Government as non-tax revenue.

Traditionally, annual transfers ranged between ?30,000 crore and ?65,000 crore. Following the adoption of the revised ECF in 2019, transfers have increased sharply:

- FY 2022–23: ?87,416 crore

- FY 2023–24: ?2.11 lakh crore

- FY 2024–25: ?2.69 lakh crore

- FY 2025–26: ?2.87 lakh crore (Highest Ever)

The RBI's balance sheet expanded by 20.6% to ?91.97 lakh crore by March 2026, while gross income increased by over 26%, supported by higher earnings from reserve management, foreign assets, and government securities.

Economic Capital Framework (ECF)

The Economic Capital Framework (ECF), based on the recommendations of the Bimal Jalan Committee (2019), provides a rule-based mechanism to determine how much capital the RBI should retain for financial stability and how much surplus can be transferred to the Government.

Its objective is to balance monetary and financial stability with the government's fiscal requirements by ensuring adequate risk buffers.

|

Component |

Provision |

|

Contingent Risk Buffer (CRB) |

4.5%–7.5% of the RBI balance sheet |

|

Contingency Fund (CF) |

5.5%–6.5% of the balance sheet |

|

Economic Capital (including CGRA) |

20.8%–25.4% of the balance sheet |

|

Review Period |

Every five years (first review in 2025) |

Concerns

The unprecedented scale of transfers has raised concerns regarding the RBI's evolving role as a fiscal support institution. Growing dependence on central bank profits may create pressures that could gradually dilute the RBI's operational independence and increase the risk of fiscal dominance, where monetary policy decisions become influenced by the government's financing needs.

Another important concern relates to fiscal federalism. Since RBI surplus is classified as non-tax revenue, it lies outside the divisible pool under Article 270, meaning States receive no automatic share despite bearing substantial expenditure responsibilities in sectors such as health, education, and welfare. When viewed alongside the increasing use of cesses and surcharges and borrowing restrictions under Article 293, some analysts argue that it reflects a broader trend toward fiscal centralization.

There are also concerns that consistently high payouts, though currently within the ECF limits, could reduce the RBI's long-term financial buffers needed to manage future macroeconomic or financial shocks.

Way Forward

The Government should prioritize utilizing RBI surplus for capital expenditure and public debt reduction rather than financing recurring revenue expenditure. The RBI must continue to manage its portfolio solely on the basis of financial stability, liquidity management, and inflation objectives, without profit maximization becoming an implicit policy goal. Greater transparency in surplus calculations and periodic reviews of the Economic Capital Framework will help preserve both fiscal credibility and central bank autonomy. At the same time, future Finance Commissions may examine the growing share of non-divisible revenues to ensure a balanced approach to cooperative fiscal federalism.

Public Expenditure on Education: Parliamentary Standing Committee Recommendation

- 21 Jun 2026

In News:

The Parliamentary Standing Committee on Education, Women, Children, Youth and Sports has recommended increasing public expenditure on education to 6% of GDP, reiterating the target envisaged under the National Education Policy (NEP) 2020. The recommendation was made in its 381st Action Taken Report while reviewing grants for the Department of Higher Education for 2025–26.

Background

The Committee assessed the progress made towards the objectives of NEP 2020 and observed that public investment in education remains below the desired level. It emphasized that sustained financial commitment is essential to achieve reforms in higher education, improve enrolment, strengthen research and innovation, and build a globally competitive education system.

Key Findings

The Committee noted that NEP 2020 envisages increasing public expenditure on education to 6% of GDP, whereas India's expenditure stood at only 4.12% of GDP in 2021–22, indicating a significant gap between policy goals and actual spending.

It also observed that the Budget Estimate (BE) for Higher Education in 2025–26 registered only a modest increase over the previous year. To adequately address inflation and support the expansion of educational infrastructure, the Committee recommended an annual budget increase of 8–10%.

Another concern highlighted was the slow growth in the Gross Enrolment Ratio (GER) between 2018 and 2023 for both male and female students. According to the Committee, greater public investment is necessary to achieve the NEP target of 50% GER in higher education by 2035.

The report further pointed out that countries such as Bhutan (7.47% of GDP) and Maldives (4.67% of GDP) allocate a larger share of their GDP to education than India, underscoring the need for enhanced public investment.

Significance

Increasing investment in education is critical for improving learning outcomes, expanding access to higher education, strengthening research and innovation, and developing a skilled workforce. Adequate funding will facilitate the implementation of key NEP 2020 reforms, including multidisciplinary education, digital learning, institutional transformation, and expansion of higher education opportunities. Enhanced educational investment also contributes to higher productivity, improved employability, and long-term inclusive economic growth.

Way Forward

Achieving the 6% of GDP target requires sustained fiscal commitment by both the Union and State Governments. Greater emphasis should be placed on improving educational infrastructure, faculty recruitment, research funding, digital inclusion, and equitable access, while ensuring efficient utilization of financial resources to realize the objectives of NEP 2020.

US–Iran Framework Peace Deal (2026)

- 20 Jun 2026

In News:

The United States and Iran have announced a framework peace deal to end nearly four months of conflict that began after the US–Israel strikes on Iran in February 2026. The Memorandum of Understanding (MoU), to be formally signed in Switzerland, seeks to restore regional stability, reopen the Strait of Hormuz, and establish a roadmap for a comprehensive nuclear agreement.

Background

The conflict originated with coordinated US–Israeli strikes targeting Iran's strategic infrastructure, including its nuclear facilities. The war resulted in significant casualties, disruption of global energy markets, and heightened instability across West Asia. A fragile ceasefire announced in April 2026 culminated in the present framework agreement after sustained diplomatic mediation by Pakistan, Qatar, Saudi Arabia, and Türkiye.

Key Provisions of the Framework Agreement

Security and Military Measures

The agreement provides for a permanent ceasefire across all fronts, including Lebanon, and envisages a gradual reduction of military tensions.

Major provisions include:

- Withdrawal of the US naval blockade on Iranian ports.

- Gradual pullback of US forces from areas surrounding Iran.

- Commitment by the United States not to expand its regional military deployment or impose additional sanctions during the implementation period.

- Final agreement to receive approval through a United Nations Security Council (UNSC) Resolution.

Reopening of the Strait of Hormuz

Iran has agreed to immediately reopen the Strait of Hormuz for international commercial shipping under its own administrative arrangements.

The Strait remains one of the world's most strategic maritime chokepoints, carrying nearly 20% of globally traded crude oil, making its reopening critical for stabilizing global energy markets and maritime trade.

Economic Provisions

The agreement seeks to revive Iran's economy through phased economic relief:

- Release of USD 24 billion of Iranian frozen assets.

- Temporary waiver of selected oil and energy-related sanctions.

- Negotiation of a proposed USD 300 billion reconstruction package within sixty days.

- Comprehensive economic negotiations will begin after partial implementation of these commitments.

Nuclear Issue Deferred

Rather than resolving the nuclear issue immediately, both countries agreed to maintain the status quo.

Iran reiterated that it would not produce nuclear weapons and agreed not to expand uranium enrichment pending negotiations on a comprehensive nuclear agreement within 60 days. Thus, the most contentious issue has been deferred for subsequent negotiations.

The 60-Day Implementation Period

The framework establishes a 60-day verification and implementation window, considered crucial for determining whether a durable peace agreement can emerge.

Its success will depend upon:

- Effective restraint on further military escalation.

- Timely withdrawal of the US naval presence.

- Release of frozen Iranian assets.

- Progress towards broader regional de-escalation.

Significance

The agreement marks a major diplomatic breakthrough in one of the world's most volatile regions. It has the potential to stabilize global energy markets, reduce geopolitical tensions in West Asia, and revive negotiations on Iran's nuclear programme under a diplomatic framework.

For India, regional stability is strategically significant because:

- The Strait of Hormuz is the principal route for India's crude oil imports from the Persian Gulf.

- Stability supports India's energy security, reduces freight and insurance costs, and safeguards Indian seafarers operating in the region.

- Improved regional conditions facilitate connectivity initiatives such as the Chabahar Port, which is central to India's engagement with Central Asia and Afghanistan.

- Peace in the region also contributes to broader stability in India's extended neighbourhood and global energy supply chains.

India–Slovakia Comprehensive Partnership

- 19 Jun 2026

In News:

Prime Minister Narendra Modi paid a historic visit to Bratislava, becoming the first Indian Prime Minister to visit Slovakia since its independence in 1993. During the visit, India and Slovakia elevated their bilateral ties to a Comprehensive Partnership, marking a new phase in cooperation across defence, technology, trade, digital innovation, labour mobility, and multilateral affairs.

India–Slovakia Relations

India established diplomatic relations with Slovakia in 1993, following the peaceful dissolution of Czechoslovakia into the Czech Republic and Slovakia. Prior to this, India maintained close ties with Czechoslovakia, one of the earliest countries to recognize independent India.

The relationship is founded on shared democratic values, pluralism, support for a rules-based international order, and commitment to multilateralism. As a member of the European Union (EU) and NATO, Slovakia has emerged as an important partner for India's engagement with Central Europe and has consistently supported stronger India–EU cooperation, including the India–EU Free Trade Agreement (FTA) and India's candidature for permanent membership of the UN Security Council (UNSC).

Major Outcomes of the Visit

Elevation to Comprehensive Partnership

The two countries upgraded their relationship to a Comprehensive Partnership, providing an institutional framework for deeper cooperation based on shared trust, strategic convergence, and long-term engagement.

Defence Cooperation

A Letter of Intent (LoI) was signed to strengthen defence collaboration through:

- Joint development and production of defence equipment.

- Defence industrial cooperation.

- Enhanced strategic and security partnership.

Trade and Economic Cooperation

Economic ties have expanded steadily, with bilateral trade reaching €1.28 billion in 2024, compared to €858.1 million in 2023 and €711.9 million in 2022.

India's major exports include:

- Mobile phones

- Footwear

- Garments

- Automobile components

- Tyres

- Pharmaceuticals

- Electrical equipment

Major imports from Slovakia include:

- Motor vehicles

- Machinery

- Pumps

- Transmission shafts

- Measuring instruments

- Bearings

- Wires and cables

Both countries agreed to expand cooperation in automobiles, railways, precision manufacturing, electronics, green technologies, and investment, while emphasizing early implementation of the India–EU FTA.

Technology and Innovation

Technology emerged as a key pillar of the partnership.

Major initiatives include:

- MoU on Digital Technology to promote cooperation in Digital Public Infrastructure (DPI).

- Establishment of an India Chair on Artificial Intelligence at a Slovak university.

- Collaboration in space technology and civil nuclear energy, with Slovak companies invited to participate in India's expanding space sector.

Labour Mobility

Both sides signed an MoU on Labour Migration to facilitate legal mobility of skilled workers and agreed to conclude a Social Security Agreement, ensuring protection of workers' social security benefits while addressing Slovakia's growing labour shortages.

Counter-Terrorism Cooperation

India and Slovakia strongly condemned terrorism, including the Pahalgam terror attack (2025), and agreed to:

- Establish a Joint Working Group on Terrorism.

- Support adoption of the Comprehensive Convention on International Terrorism (CCIT) at the United Nations.

- Take action against UNSC 1267 Sanctions Committee-listed terrorists.

- Reject double standards and oppose state-sponsored terrorism.

Multilateral Cooperation

Both countries reaffirmed their commitment to:

- Reform of the United Nations, including expansion of the UN Security Council.

- Strengthening multilateralism and the rules-based international order.

- India's aspiration for permanent membership of the UNSC.

Significance for India

The Comprehensive Partnership elevates India's engagement with Central Europe, diversifies strategic partnerships within the European Union, and strengthens cooperation in defence manufacturing, digital technologies, AI, skilled workforce mobility, clean energy, and resilient supply chains. Slovakia's strategic location in Europe and its advanced manufacturing base complement India's Make in India, Digital India, and Atmanirbhar Bharat initiatives, while also reinforcing India's broader objective of deepening ties with Europe amid evolving geopolitical and economic dynamics.

Supreme Court-Appointed National Task Force (NTF) on Student Mental Health and Suicides

- 18 Jun 2026

In News:

The Supreme Court-appointed National Task Force (NTF) has submitted its interim report on student mental health and suicides, observing that student suicides are not merely individual mental health issues but reflect structural and institutional failures. The report calls for comprehensive reforms in higher educational institutions to address systemic causes of student distress.

About the National Task Force (NTF)

The National Task Force (NTF) was constituted by the Supreme Court in Amit Kumar & Ors. v. Union of India (2026) under the chairmanship of Justice S. Ravindra Bhat (Retd.), former Judge of the Supreme Court.

The Task Force was mandated to examine the causes of student suicides in higher educational institutions and recommend measures to strengthen institutional support systems and student well-being.

Key Findings of the Interim Report

The NTF concluded that student suicides are the outcome of multiple structural, social, academic, institutional and economic factors, rather than being solely attributable to mental health disorders.

Major findings include:

- Absence of a dedicated legal framework for suicide prevention in higher educational institutions, with existing measures largely limited to non-binding guidelines.

- Over 70% of institutions lack full-time mental health professionals, while less than 4% have structured suicide-risk management systems.

- Social exclusion and discrimination, particularly among SC, ST and OBC students, contribute to higher dropout rates and psychological distress.

- Significant mismatch between the diversity of the student population and faculty representation adversely affects inclusion and academic integration.

- Financial hardship, institutional discrimination and inadequate support mechanisms further increase student vulnerability.

Key Recommendations

The NTF has recommended a systemic approach centred on institutional accountability and student welfare.

Key recommendations include:

- Filling all faculty vacancies, including reserved-category posts, within three months, while ensuring that key administrative positions remain vacant for no more than one month.

- Making mandatory reporting of every student suicide by educational institutions to regulators and State nodal authorities, irrespective of where the death occurs.

- Ensuring 24×7 access to qualified medical and mental health professionals in all residential educational institutions.

- Directing the National Crime Records Bureau (NCRB) to maintain separate data on school and higher education student suicides to facilitate evidence-based policymaking.

Significance

The report shifts the discourse from viewing student suicides solely as individual mental health failures to recognising them as a governance, equity and institutional responsibility issue. Its recommendations aim to strengthen mental healthcare, improve inclusivity, enhance institutional accountability, and support vulnerable student groups. If implemented effectively, the recommendations could contribute significantly to creating safer, more equitable and supportive educational environments.

AI Data Centers and Environmental Friction

- 17 Jun 2026

In News:

Global opposition to the environmental impact of Artificial Intelligence (AI) data centres is intensifying. Communities across the United States, Europe, Latin America, and Southeast Asia are increasingly resisting hyperscale AI infrastructure due to concerns over excessive water consumption, electricity demand, land use, and ecological degradation.

What are AI Data Centres?

AI data centres are hyperscale computing facilities equipped with high-performance processors designed to train, deploy, and operate Artificial Intelligence and machine learning models. Unlike conventional data centres that mainly store and process digital information, AI data centres require continuous, energy-intensive computing to handle billions of computations every second, resulting in significantly higher demand for electricity, cooling systems, and water.

Global Trends

Growing environmental concerns have led to increased scrutiny of AI infrastructure worldwide.

- In 2025, community protests reportedly delayed or blocked AI data centre projects worth about USD 152 billion.

- The European Union is encouraging smaller, energy-efficient regional data centres powered by renewable energy and waste-heat recovery.

- Several US States have introduced stricter approval processes and resource-impact assessments before permitting hyperscale facilities.

India's AI Data Centre Expansion

India is positioning itself as a major AI infrastructure hub.

- The Adani Group has announced plans to invest USD 100 billion in developing a 5 GW AI infrastructure platform by 2035.

- Google and the Adani Group are jointly establishing a 2 GW hyperscale data centre in Visakhapatnam, expected to be India's largest AI data centre.

- The project has been allotted 480 acres of land in a coastal zone, raising concerns regarding ecological sensitivity.

Environmental Concerns

AI data centres generate several environmental challenges:

- Extremely high electricity consumption, increasing pressure on already stressed power grids.

- Heavy water requirements for cooling, potentially affecting local drinking water availability.

- Land conversion in ecologically fragile coastal areas, agricultural land, and orchards.

- Increased heat generation, noise, and light pollution, affecting local ecosystems.

- Granting of utility subsidies and reported waivers from Environmental Impact Assessment (EIA) requirements for certain projects has raised concerns regarding environmental governance.

Challenges for India

India faces additional constraints owing to:

- Existing water scarcity and rising energy demand.

- Limited long-term local employment generated by highly automated hyperscale facilities.

- Balancing digital infrastructure growth with environmental sustainability.

- Need for stronger regulatory oversight of resource-intensive technology projects.

Way Forward

India should ensure that AI infrastructure development aligns with the principles of sustainable development by:

- Mandating comprehensive Environmental Impact Assessments (EIAs) for large AI data centres.

- Promoting renewable energy, water-efficient cooling technologies, and wastewater recycling.

- Rationalising electricity and water subsidies for resource-intensive projects.

- Encouraging distributed regional data centres rather than concentrating hyperscale facilities in ecologically sensitive areas.

- Establishing transparent standards for sustainable digital infrastructure while supporting India's AI ambitions.

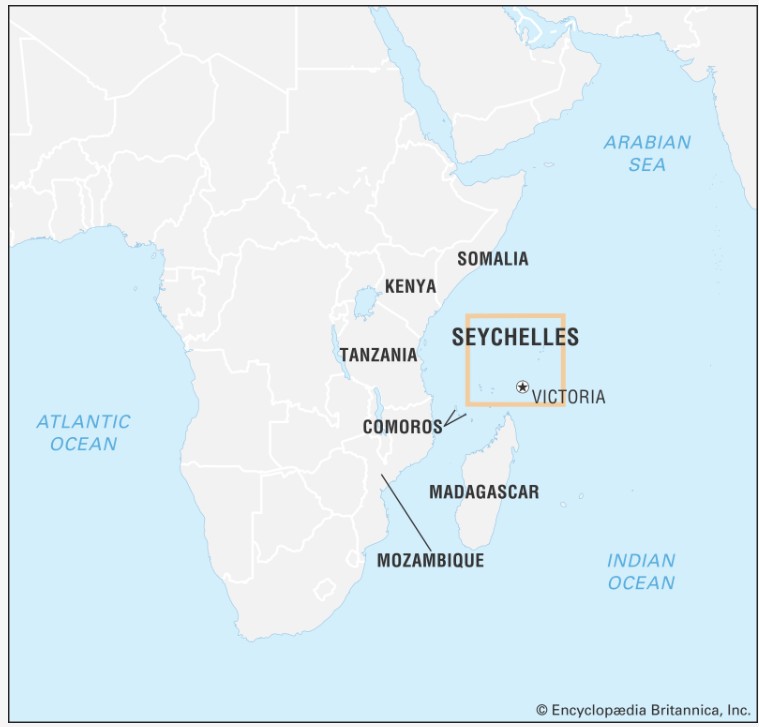

Prime Minister's State Visit to Seychelles

- 28 Jun 2026

In News:

The Prime Minister of India paid a State Visit to Seychelles as the Guest of Honour for the country's 50th National Day (Golden Jubilee of Independence) celebrations. The visit also marked 50 years of India–Seychelles diplomatic relations, during which both countries unveiled a commemorative logo celebrating five decades of bilateral ties.

Key Outcomes of the Visit

India and Seychelles signed several agreements covering digital payments, healthcare, defence, maritime cooperation, space, agriculture and capacity building, reflecting the growing strategic partnership between the two countries.

A major outcome was the agreement between NPCI International Payments Ltd. (NIPL) and the Central Bank of Seychelles to introduce the Unified Payments Interface (UPI) in Seychelles, promoting digital payments and financial inclusion. India also announced an umbrella Line of Credit worth ?1,250 crore in Indian Rupees to finance priority development projects.

In the health sector, agreements were signed to introduce the Pradhan Mantri Bhartiya Janaushadhi Pariyojana model in Seychelles through affordable generic medicines and to cooperate in developing a new Seychelles National Hospital.

The two countries also concluded an Extradition Treaty to strengthen cooperation against transnational crimes, including drug trafficking and financial fraud. An agreement on mutual recognition of seafarer certification will enable Indian seafarers to serve on Seychelles-flagged vessels.

Cooperation was further expanded through agreements on peaceful uses of outer space, agricultural research (2026–2031) between ICAR and Seychelles, and diplomatic training through collaboration between the Sushma Swaraj Institute of Foreign Service (SSIFS) and Seychelles' Ministry of Foreign Affairs.

India also handed over the Fast Patrol Vessel (FPV) PS LESPWAR, built by Goa Shipyard Limited, along with ambulances, utility vehicles and laser radial boats to strengthen Seychelles' maritime security and disaster response capabilities.

Strategic Importance of Seychelles for India

Seychelles occupies a strategically significant position in the Western Indian Ocean, close to major Sea Lanes of Communication (SLOCs) and maritime chokepoints. It plays an important role in India's maritime security, Blue Economy initiatives and Indo-Pacific strategy. The country is integrated into India's Coastal Surveillance Radar System (CSRS) network, with data linked to the Information Fusion Centre–Indian Ocean Region (IFC-IOR), enhancing maritime domain awareness. Seychelles also serves as a gateway for India's engagement with East Africa, the African Union (AU) and the Indian Ocean Commission (IOC).

Significance

The visit operationalises India's MAHASAGAR (Mutual and Holistic Advancement for Security and Growth Across Regions) vision by combining traditional development cooperation with digital, healthcare and maritime partnerships. It also reinforces India's role as a trusted development partner in the Indian Ocean Region while supporting regional stability, connectivity and sustainable development.

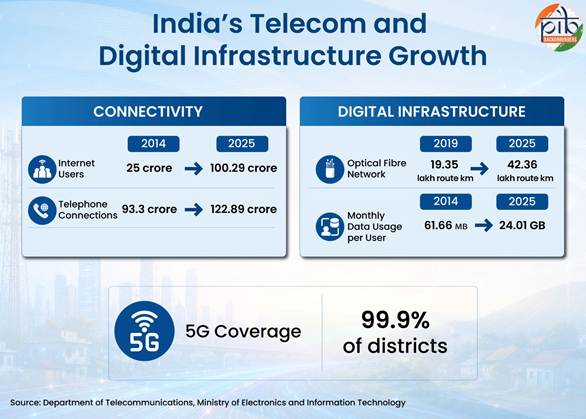

Infrastructure-Led Nation Building

- 16 Jun 2026

In News:

The Press Information Bureau (PIB) has released a comprehensive report highlighting the transformation of India's physical, digital, financial and social infrastructure over the last twelve years. The report showcases progress across transport, logistics, housing, water, energy and Digital Public Infrastructure (DPI), reflecting the government's focus on infrastructure-led economic growth.

Infrastructure-Led Nation Building

Infrastructure has emerged as a key driver of economic integration, employment generation, ease of living and global competitiveness. India's approach has shifted from isolated projects to integrated, multimodal infrastructure planning, combining transport, logistics, digital connectivity and social infrastructure to support long-term economic development.

Key Achievements

Transport & Logistics

- Railway electrification increased from about 20% (pre-2014) to 99.6% (69,873 route km) by March 2026.

- 162 Vande Bharat and 60 Amrit Bharat Express services are operational.

- Kavach 4.0, India's indigenous Automatic Train Protection system, has been deployed over 3,103 route km and installed on 4,277 locomotives, reducing consequential train accidents from 135 (2014-15) to 16 (2025-26).

- India possesses the world's second-largest road network (63.73 lakh km), while four-lane and above National Highways expanded from 18,371 km (2014) to 45,516 km (2026).

- Under PMGSY, 99.6% of eligible rural habitations are now connected by all-weather roads.

Civil Aviation, Metro & Maritime

- Operational airports increased from 74 to 165 under the UDAN Scheme, benefiting 1.64 crore passengers across 665 routes.

- Digi Yatra has facilitated over 9.3 crore seamless passenger journeys across 38 airports.

- Metro rail network expanded from 248 km to over 1,155 km across 26 cities, making India home to the world's third-largest metro network.

- Major port capacity nearly doubled from 873 MMTPA to 1,726 MMTPA, while average cargo turnaround time reduced from 94 hours to 48.8 hours.

- Operational National Waterways increased from 5 to 111, with inland cargo movement rising from 29 MMT to 218 MMT.

Social Infrastructure & Energy

- Under Jal Jeevan Mission, rural tap water coverage increased from 17% (3.23 crore households) in 2019 to 81.94% (15.86 crore households) by June 2026.

- PMAY-Urban has completed 98.10 lakh houses out of 125.31 lakh sanctioned, with 96% registered in women's ownership. PMAY-Gramin has completed 3.06 crore houses.

- India's installed power generation capacity reached 532.74 GW, while the power deficit declined from 4.2% (2014) to 0.03% (2025-26).

- LPG coverage expanded from 55.9% to 107.2%, covering 33.39 crore consumers.

Digital Public Infrastructure (DPI)

- Internet connections increased to 100.29 crore, while average monthly data consumption rose from 61.66 MB (2014) to 24.01 GB (2025).

- The JAM Trinity now comprises over 144 crore Aadhaar numbers and 57.71 crore Jan Dhan accounts.

- UPI processed 2,264 crore transactions worth ?29.53 lakh crore in March 2026 and is operational in eight countries.

- Since 2015, PRAGATI has reviewed 382 projects worth over ?85 lakh crore, resolving 2,958 implementation bottlenecks.

Challenges

Despite significant progress, challenges remain in land acquisition, last-mile approvals, difficult Himalayan terrain, underutilisation of PM-WANI public Wi-Fi, and delays in infrastructure projects due to litigation and administrative coordination.

Way Forward

The focus should remain on expanding Kavach across the remaining railway network, achieving universal rural tap water coverage under the extended Jal Jeevan Mission, strengthening Infrastructure Investment Trusts (InvITs) for infrastructure financing, accelerating industrial infrastructure under the BHAVYA initiative, and expanding India's Digital Public Infrastructure, including UPI and DigiLocker, globally.

State Finance Commissions (SFCs)

- 15 Jun 2026

In News:

The Ministry of Panchayati Raj (MoPR) released the Report on Datasets for State Finance Commissions (June 2026), highlighting critical data gaps affecting fiscal decentralisation and recommending reforms to improve the functioning of State Finance Commissions (SFCs).

State Finance Commission (SFC)

The State Finance Commission (SFC) is a constitutional body established through the 73rd and 74th Constitutional Amendment Acts, 1992 to strengthen fiscal decentralisation. It reviews the financial position of Panchayati Raj Institutions (PRIs) and Urban Local Bodies (ULBs) and recommends principles for the devolution of State finances.

Constitutional Provisions

- Article 243-I: Mandates every State to constitute an SFC every five years to review the finances of Panchayats.

- Article 243-Y: Extends the SFC's mandate to Municipalities.

- Article 280(3)(bb) & (c): Requires the Central Finance Commission (CFC) to recommend measures for augmenting State Consolidated Funds for local bodies based on SFC recommendations.

Major Functions

The SFC recommends:

- Distribution of State taxes, duties, tolls and fees between the State and local bodies.

- Allocation of resources among different tiers of PRIs and ULBs.

- Assignment of taxes and grants-in-aid.

- Measures to strengthen the financial position of local governments.

Key Findings of the MoPR Report

The report finds that poor quality and fragmented local government data remain one of the biggest obstacles to effective fiscal decentralisation.

Major Challenges

- Fragmented databases and absence of consolidated local accounts make expenditure analysis difficult.

- Shortage of trained accounting personnel at the Gram Panchayat level leads to incomplete and non-uniform financial records.

- The 15th Finance Commission observed an average delay of 16 months in submission of SFC reports.

- The 16th Finance Commission found many SFC reports inconsistent and unsuitable for framing central devolution recommendations.

Existing databases such as eGramSwaraj, Panchayat Advancement Index (PAI 2.0), Census and SECC 2011, and CAG audit reports suffer from issues of outdated information, inconsistent data entry, or inadequate Gram Panchayat-level granularity.

Key Recommendations

Strengthening Data Systems

- The report recommends creating Gram Panchayat-level digital databases with standardized accounting practices and restructuring the Panchayat Advancement Index (PAI) by classifying indicators based on needs, performance and backwardness.

- It also suggests integrating datasets through the Local Government Directory to enable uniform GP-level reporting.

Institutional Reforms

- Establish permanent SFC Cells within State Finance or Planning Departments.

- Create a national forum for knowledge sharing among SFCs.

- Request the Comptroller and Auditor General (CAG) to conduct a performance audit on the implementation of the 73rd Constitutional Amendment.

Budgetary & Reporting Reforms

- Introduce uniform accounting heads for all transfers to local bodies.

- Publish supplementary State Budget documents showing devolution up to the Gram Panchayat level.

- Adopt a common reporting format, as recommended by the 13th Finance Commission.

Capacity Building

The report recommends that NIRDPR undertake regular capacity-building programmes and document best practices, while NIPFP should prepare a comprehensive State Finance Commission Manual. It also proposes an Expert Group comprising MoPR, MoSPI, MoHUA and NITI Aayog to strengthen India's local statistics ecosystem.

Issues with State Finance Commissions

- Delayed constitution and submission of reports.

- Weak implementation of SFC recommendations by States.

- Inadequate fiscal autonomy of local bodies.

- Poor quality, fragmented and outdated data.

- Limited technical and institutional capacity.

Significance

Robust and timely SFC recommendations are essential for strengthening cooperative federalism, ensuring predictable fiscal transfers, improving local governance, and achieving the objectives of the 73rd and 74th Constitutional Amendments. Reliable local-level data will also enable evidence-based resource allocation and improve accountability in Panchayati Raj Institutions.

Way Forward

Strengthening the local government data ecosystem through standardised accounting, digital integration, capacity building, timely SFC constitution and improved institutional coordination is crucial for deepening fiscal decentralisation. Implementing these reforms will empower Panchayats and Urban Local Bodies to deliver public services more effectively and realise the constitutional vision of grassroots democracy.

SUMAN Roadmap 2030

- 29 Jun 2026

In News:

The Union Ministry of Health & Family Welfare has released the SUMAN Roadmap 2030 during the 16th Conference of the Central Council of Health and Family Welfare (CCHFW). The roadmap provides a comprehensive strategy to accelerate progress towards the Sustainable Development Goal (SDG) 3 targets by reducing maternal, neonatal and infant mortality through evidence-based and state-specific interventions.

What is SUMAN Roadmap 2030?

The SUMAN Roadmap 2030 is a national strategic framework aimed at strengthening maternal and newborn healthcare across the continuum of care. Developed under the RMNCHA N (Reproductive, Maternal, Newborn, Child, Adolescent Health and Nutrition) framework, it adopts a life-cycle approach, integrating interventions from pre-pregnancy to postnatal care.

Unlike a uniform national strategy, the roadmap proposes customised and differentiated interventions based on the specific needs of States and districts, particularly those with a high maternal and newborn disease burden.

Objectives

The Roadmap seeks to:

- Accelerate progress towards SDG-3 targets.

- Reduce Maternal Mortality Ratio (MMR) to below 70 per 100,000 live births by 2030.

- Reduce Neonatal Mortality Rate (NMR) and Infant Mortality Rate (IMR).

- Achieve universal coverage of quality maternal and newborn healthcare services.

- Eliminate preventable maternal and newborn deaths.

Key Features

Life-Cycle Approach

The roadmap integrates healthcare services across:

- Pre-pregnancy care

- Antenatal care

- Intrapartum (delivery) care

- Postnatal care

It also converges with child health, adolescent health, family planning and nutrition under the RMNCHA N framework.

High-Risk Pregnancy Management

A structured four-stage framework has been introduced for early identification and continuous monitoring of:

- Antenatal high-risk pregnancies

- Third-trimester high-risk pregnancies

- Intrapartum high-risk pregnancies

- Postnatal high-risk mothers

This aims to ensure timely referral and specialised care.

Targeted Interventions

- The roadmap prioritises 130 districts across 13 high-focus States: Assam, Bihar, Chhattisgarh, Haryana, Jharkhand, Karnataka, Madhya Pradesh, Odisha, Punjab, Rajasthan, Uttar Pradesh, Uttarakhand and West Bengal.

Key interventions include:

- SUMAN Package for Pregnant Women promoting early registration, complete antenatal care and adequate post-partum institutional stay.

- Bi-weekly ASHA home visits during the eighth and ninth months for danger-sign screening, nutrition counselling and birth preparedness.

- Financial support for a designated caregiver during the postnatal period.

- Strengthened referral transport for obstetric emergencies.

- Establishment of Birth Waiting Homes (BWHs), Maternal & Child Health (MCH) Wings, High Dependency Units (HDUs) and ICUs in underserved areas.

Strategies for All States & UTs

The roadmap also proposes nationwide measures such as:

- Pre-pregnancy folic acid supplementation.

- Comprehensive interventions to address maternal anaemia and undernutrition.

- Improved tracking of high-risk pregnancies.

- Strengthening maternal and newborn healthcare services across all levels.

Community Participation

Recognising the importance of community ownership, the roadmap introduces:

- SUMAN Panchayat to promote:

- Zero preventable maternal deaths

- Zero infant deaths

- Universal antenatal care

- Institutional deliveries

- Full immunisation

- Mothers' Picnic, a community awareness platform encouraging healthy maternal and newborn care practices.

Technology & Innovation

The roadmap leverages technology to improve service delivery through:

- AI-enabled labour rooms

- Digital monitoring via the JANANI Portal

- Strengthened Maternal Death Surveillance and Response (MDSR)

- Maternal Near Miss (MNM) reviews

- Use of Non-Pneumatic Anti-Shock Garments (NASG) for managing obstetric haemorrhage.

- Climate-responsive action plans to address heatwaves and other climate-related risks.

- Establishment of SUMAN Call Centres for grievance redressal and referral coordination.

Significance

The SUMAN Roadmap 2030 marks a shift from a one-size-fits-all approach to a district-specific, evidence-based maternal health strategy. By integrating healthcare services across the life cycle, strengthening high-risk pregnancy management, leveraging digital technologies and promoting community participation, it seeks to bridge regional disparities in maternal and newborn healthcare.

The roadmap also reinforces India's commitment to achieving SDG-3, universal health coverage and the goal of zero preventable maternal and newborn deaths by 2030.

Urban Fire Safety in India

- 14 Jun 2026

In News:

Recent fire tragedies, including the devastating blaze at a guest house in Delhi's Malviya Nagar and a hospital fire in Bihar, have once again drawn attention to the growing fire safety crisis in India's urban areas. These incidents are not isolated accidents but symptoms of deeper structural weaknesses in urban planning, building regulation, and emergency response systems.

Fire Safety: A Persistent Urban Risk

India continues to witness a significant number of fire-related deaths every year. According to NCRB data, nearly 60% of fire fatalities occur within residential buildings, making homes the most vulnerable spaces despite being perceived as safe environments. Hospitals, shopping complexes, hotels, and other commercial establishments also account for a substantial share of casualties.

The recurring nature of such incidents points towards systemic shortcomings rather than individual lapses.

Why Are Urban Fires Becoming More Frequent and Deadly?

One of the primary reasons is the absence of basic fire safety infrastructure in a large number of residential and mixed-use buildings. Smoke detectors, sprinkler systems, fire alarms, emergency exits, and evacuation plans are either missing or poorly maintained.

Another major concern is the widespread conversion of residential buildings into commercial establishments such as guest houses, hostels, and hotels without corresponding upgrades in safety infrastructure. Such unauthorized modifications increase occupancy while compromising evacuation and firefighting capabilities.

Electrical faults remain the leading cause of urban fires. Aging wiring systems, overloaded circuits, poor maintenance, and increasing dependence on electrical appliances create a constant fire hazard. LPG leakages due to defective equipment and unsafe handling practices further aggravate the risk.

The challenge is compounded by India's dense urban settlements. Narrow roads, congested neighbourhoods, illegal constructions, and inadequate access routes often delay the arrival of fire engines and hamper rescue operations.

Understanding the Nature of Fire Hazards

Fire-related deaths are often caused not by burns but by smoke inhalation and toxic gases. As noted by the National Institute of Disaster Management (NIDM), oxygen depletion and poisonous fumes released from burning materials are responsible for a majority of fatalities.

High temperatures can also trigger secondary explosions due to the expansion of gases, fuels, and combustible substances. Consequently, even a localized fire can rapidly escalate into a major disaster.

Recognizing this, the National Disaster Management Authority (NDMA) categorizes fire as a human-induced disaster, emphasizing that most fire incidents are preventable through proper planning and compliance.

Regulatory and Institutional Framework

Fire services are a State subject under the Constitution and have also been included as a municipal responsibility under Article 243W and the Twelfth Schedule. Therefore, the primary responsibility for fire prevention and emergency response lies with State Governments and Urban Local Bodies (ULBs).

India already possesses a comprehensive regulatory framework through the National Building Code (NBC), 2016, prepared by the Bureau of Indian Standards (BIS). The code provides detailed provisions relating to fire-resistant construction, smoke management, evacuation systems, electrical safety, periodic audits, and modern firefighting technologies.

However, the challenge lies not in the absence of regulations but in weak implementation and poor enforcement.

Key Challenges

A major governance gap exists in the enforcement of building and fire safety norms. Unauthorized constructions, illegal land-use conversions, and inadequate inspections continue to undermine safety standards.

Fire services across many states remain under-equipped and understaffed. Recognizing this deficiency, the 15th Finance Commission recommended ?5,000 crore for strengthening fire services and emergency response infrastructure. Nevertheless, significant shortages persist in equipment, manpower, training, and high-rise firefighting capabilities.

Rapid urbanization presents another challenge. The growth of high-rise buildings, vertical cities, and mixed-use developments demands sophisticated firefighting technologies and specialized response systems, which many urban centres still lack.

The Way Forward

Addressing urban fire risks requires a multi-pronged strategy. Strict enforcement of the National Building Code and regular fire safety audits must become mandatory for residential, commercial, and institutional buildings. Unauthorized building conversions should attract stringent penalties.

Fire services require substantial modernization through investment in advanced equipment, high-rise rescue systems, early warning technologies, and professional training. Public awareness campaigns, evacuation drills, and community-based preparedness programmes can help create a culture of fire safety.

Urban planning must also integrate disaster-risk reduction principles by ensuring wider access roads, adherence to zoning regulations, and fire-resilient infrastructure in rapidly expanding cities.

Conclusion

Urban fire disasters are largely preventable. Their recurrence reflects failures in regulation, planning, enforcement, and preparedness rather than a lack of legal provisions. As Indian cities continue to expand vertically and horizontally, strengthening fire safety systems must become an integral component of urban governance. Building resilient cities will require coordinated action by governments, municipal authorities, builders, businesses, and citizens alike. Without systemic reforms, the cycle of tragedy, outrage, and temporary corrective action is likely to continue.

SIPRI Yearbook 2026

- 13 Jun 2026

In News:

The Stockholm International Peace Research Institute (SIPRI), in its Yearbook 2026, has highlighted growing global nuclear risks, weakening arms-control frameworks, and the increasing integration of emerging technologies into warfare. A significant observation regarding India is the expansion of its nuclear arsenal to approximately 190 warheads and the reported deployment of a small number of warheads in an operational state, reflecting the evolving nature of India's strategic deterrence posture.

Key Findings on India

India emerged as the fifth-largest military spender globally in 2025, with defence expenditure rising by 8.9% to USD 92.1 billion. SIPRI also identified India as the second-largest importer of major arms during 2021–25, accounting for 8.2% of global arms imports.

According to the report, India's nuclear stockpile is estimated at 190 warheads, comprising 12 deployed warheads and 178 in reserve/storage. This places India behind China (620 warheads) but ahead of Pakistan (170 warheads). The report suggests that India is gradually enhancing the operational readiness and survivability of its nuclear deterrent.

Another notable development was the integration of cyber operations into military confrontation during the 2025 India-Pakistan conflict, indicating the growing importance of cyber capabilities in modern warfare and deterrence.

Global Security Trends

The report notes that all nine nuclear-armed states continue to modernize and expand their arsenals. Globally, there are an estimated 12,187 nuclear warheads, of which around 9,745 are available for military use, while more than 4,000 remain deployed on missiles and aircraft.

The United States and Russia together possess nearly 86% of the world's nuclear weapons, yet the expiry of the New START Treaty in 2026 without a successor agreement has increased concerns regarding strategic stability.

SIPRI also points to the growing use of artificial intelligence, autonomous systems, drones, and cyber capabilities in contemporary conflicts such as Ukraine and Gaza, signalling a transformation in the nature of warfare.

Simultaneously, the global arms-control architecture is witnessing strain, reflected in withdrawals from treaties such as the Convention on Cluster Munitions and the Anti-Personnel Mine Convention.

India's Nuclear Doctrine

India's nuclear doctrine, officially operationalized in 2003, is based on the principles of credible minimum deterrence and No First Use (NFU).

Under the doctrine, India pledges not to initiate a nuclear attack and reserves the use of nuclear weapons solely for retaliation against a nuclear strike on Indian territory or armed forces. Any such retaliation would be massive and designed to inflict unacceptable damage on the aggressor.

The doctrine also emphasizes strict civilian control through the Nuclear Command Authority (NCA). The Political Council, chaired by the Prime Minister, alone possesses the authority to authorize nuclear weapon use, while the Executive Council, headed by the National Security Advisor, provides operational inputs.

India additionally maintains that it may consider nuclear retaliation in response to a major chemical or biological weapons attack.

Evolution of India's Nuclear Programme

India's nuclear journey began as a peaceful programme focused on energy self-reliance under Homi J. Bhabha and Jawaharlal Nehru. However, changing security dynamics, particularly China's nuclear test in 1964, prompted India to conduct its first nuclear test, Pokhran-I (Smiling Buddha), in 1974.

Subsequently, strategic concerns arising from China's capabilities and the China-Pakistan nexus led to Pokhran-II (Operation Shakti) in May 1998, after which India formally declared itself a nuclear weapon state.

Since then, India has developed a doctrine centred on deterrence rather than warfighting while simultaneously integrating into global nuclear commerce through the 2008 India–US Civil Nuclear Agreement and the Nuclear Suppliers Group waiver.

India's Position on Global Nuclear Governance

India remains outside the Nuclear Non-Proliferation Treaty (NPT) and the Comprehensive Nuclear-Test-Ban Treaty (CTBT), arguing that these arrangements are discriminatory because they divide the world into nuclear "haves" and "have-nots."

At the same time, India has demonstrated responsible nuclear behaviour and has secured membership in major export-control regimes, including the Missile Technology Control Regime (MTCR), Wassenaar Arrangement, and Australia Group, while continuing to seek membership in the Nuclear Suppliers Group (NSG).

Conclusion

The SIPRI Yearbook 2026 underscores a world witnessing renewed strategic competition, nuclear modernization, and rapid technological transformation in warfare. For India, the expansion of its nuclear arsenal and limited deployment of warheads reflect efforts to maintain a credible deterrent amid a complex security environment shaped by nuclear rivalry with Pakistan, strategic competition with China, and evolving threats in cyberspace and emerging technologies. Going forward, balancing national security requirements with commitment to responsible nuclear stewardship and global disarmament will remain central to India's strategic outlook.

Supreme Court Seat Expansion through Ordinance

- 12 Jun 2026

In News:

A constitutional debate has emerged following the President's promulgation of an Ordinance under Article 123 increasing the sanctioned strength of the Supreme Court from 34 to 38 judges. While the move seeks to address mounting judicial workload and vacancies, it has raised important questions regarding judicial independence, separation of powers, security of tenure, and the limits of executive law-making.

What Happened?

Following the Ordinance, five new judges were appointed to the Supreme Court. Two appointments filled existing vacancies within the previously sanctioned strength of 34 judges. However, the remaining three appointments were made against the additional posts created through the Ordinance.

The controversy arises because these new posts are temporary unless Parliament subsequently enacts a law replacing the Ordinance.

Constitutional Provisions Involved

Article 124(1)