End of the ‘Cheap Money’ Era

- 03 Jun 2026

In News:

The Reserve Bank of India (RBI), in its Annual Report 2025–26, has cautioned about rising sovereign bond yields across major economies and the possibility of a reversal in monetary easing by global central banks. This signals the gradual end of the long phase of ultra-low interest rates and abundant global liquidity that characterized the post-2008 and post-pandemic world economy.

Understanding the Context

A government bond is a debt instrument issued by a sovereign government to raise funds. In return, the government pays periodic interest and repays the principal at maturity. Since sovereign governments back these securities, they are generally considered among the safest financial assets.

The return earned on these securities is known as the bond yield, which acts as a benchmark for interest rates across the economy. Higher bond yields typically translate into higher borrowing costs for governments, businesses, and households.

The era of cheap money was largely driven by Quantitative Easing (QE), a monetary policy under which central banks created new money to purchase government bonds and long-term assets. This increased liquidity, reduced interest rates, and encouraged lending and investment.

The Rise and Fall of Cheap Global Money

Following the 2008 Global Financial Crisis and later the COVID-19 pandemic, central banks in advanced economies maintained exceptionally low interest rates and pursued aggressive QE policies.

As a result:

- US bond yields declined from over 6% in the late 1990s and early 2000s to around 0.9% during 2020–21.

- UK yields fell from 5.4% to 0.4%.

- Japan's yields approached zero, and even turned negative during 2016–17 and 2019–20.

This abundance of low-cost capital pushed global investors towards emerging markets such as India in search of higher returns.

However, the situation has changed dramatically. Supply-chain disruptions after COVID-19, the Russia–Ukraine conflict, tariff actions under the Trump administration in 2025, and the ongoing US–Israel versus Iran conflict have revived inflationary pressures globally. Consequently, central banks have moved away from ultra-loose monetary policies.

Rising Global Bond Yields

The reversal is visible in sovereign bond markets:

- Japan: Average yield of 1.8% in 2025–26, rising to 2.5%, with a peak of 2.8% in May 2026.

- United States: Average yield of 4.2%, rising to 4.4%, with a high of 4.7%.

- United Kingdom: Average yield of 4.6%, increasing to 4.9%, with a high of 5.2%.

These figures indicate that global capital is becoming increasingly expensive.

Implications for India

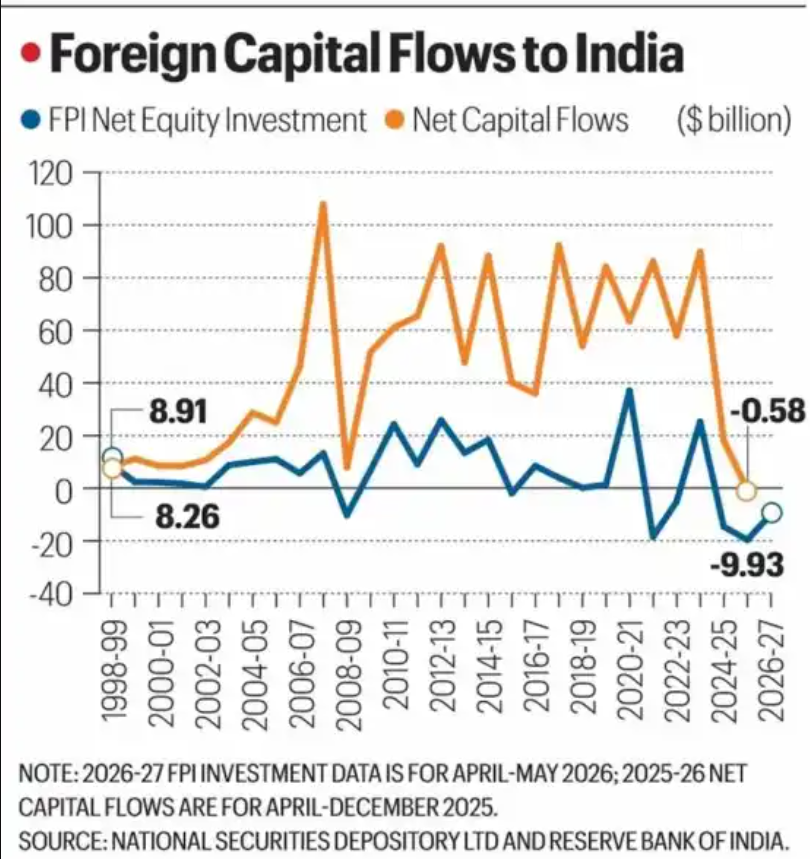

India benefited significantly from global liquidity during the cheap-money era. Net capital inflows rose from $8.3 billion in 1998–99 to a record $107.9 billion in 2007–08, and averaged $67.3 billion annually between 2009–10 and 2023–24. However, inflows fell sharply to $18 billion in 2024–25, while the first nine months of 2025–26 recorded net capital outflows of $580 million.

Another concern is the narrowing yield gap between Indian and US government bonds. India's 10-year government bond yield is around 7%, while the US 10-year Treasury yield is about 4.5%, leaving a differential of only 2.5 percentage points, compared to a historical average of more than 4 percentage points. After accounting for rupee depreciation and the safe-haven appeal of US Treasuries, Indian assets become relatively less attractive to foreign investors.

This could result in:

- Lower foreign capital inflows.

- Increased pressure on the rupee.

- Higher borrowing costs for governments and businesses.

- Greater stock market volatility.

- Challenges in financing current account deficits.

The Way Forward

In a world where capital is no longer abundant and cheap, India must increasingly rely on its own economic fundamentals. Sustaining high GDP growth, maintaining macroeconomic stability, expanding manufacturing through initiatives such as Make in India and PLI schemes, deepening domestic financial markets, and attracting stable long-term FDI will be crucial.

The RBI's warning highlights a broader structural shift in the global economy. As the era of easy money fades, countries will have to compete for investment on the basis of growth prospects, policy credibility, and economic resilience rather than merely benefiting from excess global liquidity.