The Rising Cost of Imports: A Concern for India's Food Security and Farmers

- 21 Jun 2025

In News:

India’s increasing dependence on imports of pulses and edible oils has raised serious concerns about agricultural sustainability, trade deficits, and farmer welfare. Despite policy claims of self-reliance in agriculture, recent trends highlight structural imbalances in domestic production and pricing mechanisms, especially for pulses and oilseeds.

Farmers at the Receiving End

Farmers cultivating pulses and oilseeds, such as moong, chana, masoor, and soyabean, are struggling due to poor price realization and lack of systematic procurement at Minimum Support Prices (MSP). Rao Gulab Singh Lodhi, a farmer from Madhya Pradesh, harvested 90 quintals of moong in summer 2025. Despite an MSP of ?8,682/quintal, he had to sell his produce in the open market at ?6,000/quintal due to the absence of procurement infrastructure. Soyabean prices, too, are well below MSP, selling at ?4,100–4,200/quintal against an MSP of ?5,328 (for 2025–26).

Unlike rice and wheat, for which procurement is extensive and assured, pulses and oilseeds lack institutional support, even in regions where agro-climatic conditions favour their cultivation. This discourages farmers from growing these critical crops, despite using high-yielding and climate-resilient varieties.

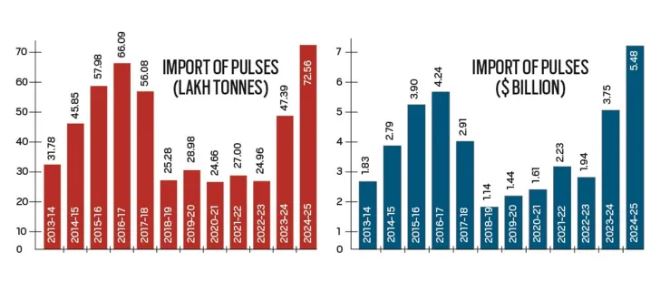

Pulses: From Self-Reliance to Import Surge

India witnessed a record 7.3 million tonnes (mt) of pulses imports worth $5.5 billion in 2024–25, surpassing the previous high of 6.6 mt in 2016–17. This comes after years of reduced imports, thanks to improved domestic production which had peaked at 27.3 mt in 2021–22.

However, the El Niño-induced drought in 2023–24 brought down production to 24.2 mt, leading to higher retail inflation in pulses and prompting duty cuts on imports. While these imports helped control prices—with CPI inflation in pulses falling to –8.2% by May 2025—they also depressed mandi prices. In Maharashtra, arhar and chana are currently trading below MSPs, impacting farmer incomes.

Major pulse imports in 2024–25 included:

- 2.2 mt of yellow/white peas (Canada, Russia),

- 1.6 mt of chana (Australia),

- 1.2 mt each of arhar and masoor (Africa, Canada, Australia),

- 0.8 mt of urad (Myanmar, Brazil).

Edible Oils: Worsening Import Dependency

India’s vegetable oil imports more than doubled in a decade—from 7.9 mt in 2013–14 to 16.4 mt in 2024–25. In value terms, imports jumped from $7.2 billion to $20.8 billion, driven partly by global supply disruptions (e.g., Russia-Ukraine war) and high domestic consumption.

India now imports over 60% of its edible oil needs, with palm (7.9 mt), soyabean (4.8 mt), and sunflower oil (3.5 mt) forming the bulk. In May 2025, CPI inflation for vegetable oils stood at 17.9%. In response, the Centre slashed import duties on crude palm, soyabean, and sunflower oil from 20% to 10%, reducing the overall tariff to 16.5%.

While the move may lower consumer prices, industry bodies like the Soyabean Processors Association of India have warned it will "flood the market with cheap imports", making domestic oilseed cultivation less viable. Farmers may shift to alternative crops in the coming kharif season, further weakening India’s self-sufficiency goals.

Conclusion

India’s growing import reliance for essential food commodities like pulses and edible oils, coupled with poor farm-level price realization and weak procurement systems, undermines the objectives of food security and self-reliance. Sustainable import substitution must be driven by robust domestic production incentives, fair pricing mechanisms, and resilient procurement frameworks—especially for non-cereal crops.