Geopolitical Shocks and India’s Fertilizer Security: The 2026 Crisis

- 21 Apr 2026

In News:

The escalation of the US-Israel vs. Iran conflict in early 2026, culminating in the closure of the Strait of Hormuz in February, has sent shockwaves through global commodity markets. For India, this maritime blockade is not merely a diplomatic hurdle but a direct threat to national food security. The crisis underscores India’s heavy reliance on the Persian Gulf for both finished fertilizers and the energy inputs required for domestic production.

The Anatomy of the Crisis: India’s Vulnerability

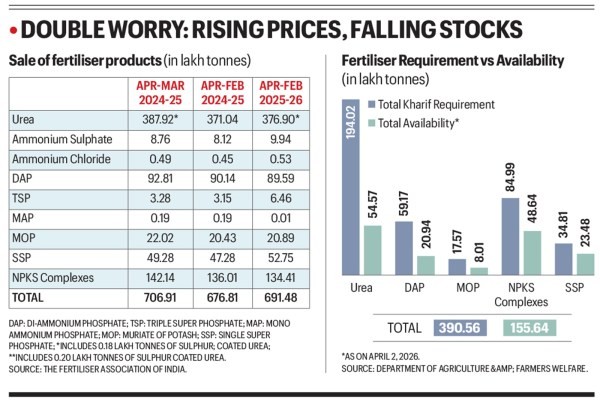

India’s agricultural model, rooted in the Green Revolution, remains high-intensity, requiring massive annual consumption of nutrients—approximately 40 million tonnes (mt) of urea alone. The current blockade has exposed two critical vulnerabilities:

The Import Dependency Trap

The Gulf Cooperation Council (GCC) nations (Oman, Qatar, Saudi Arabia, UAE, and Bahrain) are indispensable partners in India’s "Soil to Silo" chain:

- Urea: GCC countries account for nearly 49% of India’s nitrogen fertilizer imports.

- Feedstock (LNG): Over 60% of India's Liquefied Natural Gas (LNG) is sourced from the Gulf. Since natural gas is the primary feedstock for urea, the energy blockade has crippled domestic factories.

- Intermediates: Prices for essential raw materials like Sulphur and Ammonia have tripled, exceeding $900 per tonne.

The Maritime Chokepoint

The Strait of Hormuz is a physical bottleneck. Unlike the 2022 Russia-Ukraine crisis, where fertilizers could be rerouted via rail or alternative ports, the Hormuz closure "traps" cargo. Tanker traffic dropped to near zero by March 2026 as insurance companies withdrew war-risk coverage, making shipping economically unviable.

Impact Assessment:

- The Price Shock: International urea bids skyrocketed from $510 in February to $950 per tonne by April 2026.

- Production Contraction: Domestic urea output fell from a monthly average of 2.5 mt to 1.5 mt in March 2026 due to LNG shortages and force majeure invoked by suppliers like Petronet LNG.

- Subsidy Burden: To insulate farmers, the Union Cabinet cleared a 12% hike in the Nutrient Based Subsidy (NBS) for Kharif 2026, totaling ?41,533 crore. Analysts estimate the total annual subsidy bill could swell by an additional ?25,000 crore, reaching nearly ?2 trillion.

Government Response and Mitigation Strategies

To prevent a "Harvest of Discontent," the Indian government has launched a multi-pronged tactical response:

- Sourcing Diversification: India is aggressively pivoting to non-Gulf suppliers. Agreements have been fast-tracked with Morocco (for Phosphorus), Russia, Canada, and Jordan (for Potash), and Indonesia/Malaysia (for Ammonia).

- The "Priority Sector-2" Mandate: Under the Natural Gas (Supply Regulation) Order, 2026, the government has mandated that 70% of available natural gas be prioritized for urea plants to keep domestic production running.

- Buffer Management: Leveraging a lean consumption phase, India built a massive opening stock of 18 million tonnes (46% of seasonal requirement) before the peak of the crisis, providing a critical safety net for the Kharif 2026 season.

- Promoting Alternatives: To reduce the pressure on Di-Ammonium Phosphate (DAP), the government is encouraging the use of Single Super Phosphate (SSP) and Triple Super Phosphate (TSP).

Challenges and Structural Risks

- Fiscal Stress: The widening gap between soaring international prices and the fixed subsidized price for farmers (e.g., ?266.5 per 45kg bag of urea) places an immense burden on the fiscal deficit.

- The Rabi Risk: While current stocks may sustain the Kharif crop (June–September), the Rabi season (starting October) remains highly vulnerable if diplomatic efforts fail to reopen the Strait.

- Black Market Emergence: Shortages in raw materials often lead to hoarding at the retail level, requiring strict enforcement under the Essential Commodities Act.

The Way Ahead: A "Nutrient-Secure" India

The 2026 crisis is a wake-up call to transition from "Volume-based" to "Efficiency-based" agriculture:

- Nano-Fertilizers: Accelerating the shift to Nano Urea and Nano DAP can reduce the logistics of importing millions of bulk bags.

- Bio-Stimulants & Fortification: Coating fertilizers with micronutrients (Zinc, Boron) and using Phosphate Solubilizing Bacteria can help unlock nutrients already present in the soil, reducing the need for chemical inputs.

- Diplomatic Neutrality: India must leverage its "Strategic Autonomy" to advocate for neutral trade corridors for food and fertilizer precursors within conflict zones.

Conclusion

The Iran war has highlighted the "thermal injustice" of India’s food security—where a conflict thousands of miles away can dictate the margins of a farmer in Punjab or Andhra Pradesh. Long-term resilience lies in reducing the nitrogen-heavy dependency on the Gulf and embracing a circular nutrient economy powered by domestic innovation and biological alternatives.