India–South Africa Technology Partnership

- 11 Jun 2026

In News:

India and South Africa have upgraded their 31-year-old Science and Technology partnership from a research-centric framework to a technology-driven industrial co-production model, marking a significant evolution in India–Africa relations. The move reflects India's broader strategy of strengthening Global South cooperation through innovation, supply-chain resilience and economic integration.

Key Areas of Cooperation

- The partnership will focus on emerging technologies such as Artificial Intelligence (AI), Digital Public Infrastructure (DPI), advanced manufacturing, quantum technologies, genomics and cyber-physical systems. Both countries are also expanding cooperation in green hydrogen, renewable energy, biotechnology, vaccine development and healthcare innovation.

- A major area of collaboration remains the Square Kilometre Array (SKA) project, which supports advancements in astronomy, big data analytics and high-performance computing.

Telangana–South Africa Collaboration

- The partnership has acquired a sub-national dimension through cooperation between Telangana and South Africa. Leveraging Hyderabad's strengths in IT, pharmaceuticals, healthcare, aerospace and defence manufacturing, the collaboration seeks to promote medical tourism, vaccine production, healthcare supply chains and investment in advanced manufacturing.

India's Emerging Africa Strategy

- India's engagement with Africa is gradually shifting from Lines of Credit and development assistance towards industrial co-production, technology partnerships, critical minerals cooperation and value-chain integration.

- India is increasingly leveraging the African Continental Free Trade Area, while also pursuing access to strategic minerals such as lithium, cobalt and rare earth elements that are crucial for electric mobility, renewable energy and the green hydrogen economy.

Geopolitical Significance

- The deepening partnership strengthens cooperation among Global South countries and supports efforts to reform global governance institutions. It also complements India's SAGAR (Security and Growth for All in the Region) vision through enhanced maritime cooperation and capacity building in the Indian Ocean Region.

- The partnership offers an alternative model of development cooperation based on capacity building, technology sharing and mutual benefit, while reinforcing India's growing diplomatic and economic presence in Africa.

Challenges

- Despite growing engagement, challenges persist in the form of project implementation delays, political instability in parts of Africa, competition from China's economic presence, trade barriers and connectivity constraints.

Conclusion

The India–South Africa partnership signifies a transition from traditional scientific cooperation to a comprehensive framework centred on technology, innovation, green energy, healthcare and industrial co-production. As India deepens its engagement with Africa through economic integration and strategic partnerships, the relationship is likely to emerge as a key pillar of Global South cooperation and sustainable development.

India–Canada Trade and Investment Forum 2026

- 04 Jun 2026

In News:

The Union Commerce and Industry Minister led the largest-ever Indian business delegation to Canada. Both countries launched the Canada-India Trade and Investment Forum and reaffirmed their commitment to conclude the Comprehensive Economic Partnership Agreement (CEPA) by end of 2026.

Canada-India Trade and Investment Forum

- The Forum was launched as a permanent institutional platform to bring together Canadian and Indian business leaders, foster commercial partnerships, and drive two-way investment.

- Key outcomes include: a shared trade target of USD 50 billion by 2030 (current bilateral merchandise trade stands at approximately USD 13.6 billion); a focus on Small and Medium Enterprises (SMEs) as the operational backbone of untapped trade volumes; and Canada's announcement of a "Team Canada Trade Mission" to India later in 2026.

- Negotiations will adopt a pragmatic "low-hanging fruit" approach, avoiding immediate demands in sensitive sectors like agriculture and dairy. Canada described the CEPA as a potential "game changer" for bilateral economic ties.

Strategic Sectors of Cooperation

- Both sides agreed to deepen cooperation in clean energy, critical minerals, agri-food, advanced manufacturing, digital technologies, and skills development. Significantly, in May 2026, an MoU was signed to develop secure and resilient critical mineral supply chains, aligning with the G7 Critical Minerals Action Plan. Canada is a Tier-1 global supplier of potash, uranium, and nickel — resources essential for India's EV manufacturing ambitions and renewable energy transition.

About CEPA

A CEPA is a comprehensive bilateral free trade agreement covering trade in goods, services, investment, competition, and intellectual property rights (IPR) — broader than a standard FTA. India currently has five CEPAs in force: with South Korea, Japan, Malaysia, UAE, and Oman.

Current Trade Profile (2025)

- Merchandise: India exports USD 9.7 billion (pharmaceuticals, machinery, electronics, precious metals, iron and steel); imports USD 3.9 billion (vegetables, mineral fuels, wood pulp, fertilisers, paper).

- Services: Strongly favours Canada — USD 15.2 billion exports vs USD 4.5 billion imports, driven overwhelmingly by Indian student education spend.

Strategic Significance

- Critical Minerals and Energy Security: Canadian uranium sustains India's civilian nuclear programme under the 2010 Nuclear Cooperation Agreement. Canadian potash and nickel are critical for India's green transition.

- Indo-Pacific Balance: Canada's Indo-Pacific Strategy identifies India as a key partner for a rules-based regional order, aligning with India's MAHASAGAR vision as a counterweight to Chinese assertiveness.

- Diaspora Bridge: The Indian diaspora of 1.8 million (≈4% of Canada's population) exercises significant political and corporate influence. India remains the largest source of international students in Canada.

- Security Architecture: Bilateral security cooperation is anchored in the Joint Working Group on Counter Terrorism (1997), Framework for Cooperation on Countering Terrorism (2018), Extradition Treaty (1987), and Mutual Legal Assistance Treaty (1994).

- Frontier Tech: The Australia-Canada-India Technology and Innovation Partnership (ACITI) advances cooperation in quantum computing, biotechnology, and advanced manufacturing.

AI-Driven Disaster Resilience: Transforming India’s Management Framework

- 26 Mar 2026

In News:

India’s geographical diversity makes it highly susceptible to a range of natural disasters, from cyclones and floods to avalanches and droughts. In a landmark shift toward technology-led resilience, the Government of India has significantly expanded the role of Artificial Intelligence (AI) and Machine Learning (ML) following the enactment of the Disaster Management (Amendment) Act, 2025. This legislative and technological synergy aims to move the nation from a "reactive" relief-centric approach to a "proactive" predictive-modeling stance.

The Disaster Management Cycle & AI Integration

AI is being integrated across all four stages of the disaster management cycle to enhance precision and reduce human casualty.

A. Preparedness and Early Warning

The India Meteorological Department (IMD) has pioneered the use of AI/ML under Mission Mausam to bridge the gap between data collection and actionable intelligence.

- Seven-Day Forecasts: Advanced ML models now provide 7-day advance weather predictions with higher local accuracy.

- Cyclone Tracking: AI-enhanced satellite imagery analysis allows for better prediction of cyclone intensity and landfall coordinates.

B. Mitigation and Hydrological Modelling

The Central Water Commission (CWC) has deployed AI to tackle India's most frequent disaster: flooding.

- Short-Range Forecasting: AI models process real-time rainfall data and river discharge levels to provide short-range flood alerts.

- Digital Advisories: Real-time flood advisories are disseminated via integrated digital portals, utilizing rainfall-based hydrological modelling to warn downstream populations.

C. Risk Mapping and Decision Support

The National Disaster Management Authority (NDMA) has developed sophisticated tools to assist local administrators.

- Web-DCRA & DSS: The Web-based Dynamic Composite Risk Analysis and Decision Support System (DSS) allows officials to visualize potential impact zones.

- Dynamic Risk Atlases: These atlases use AI to factor in real-time variableslike population density and infrastructure strength—to optimize evacuation planning during cyclones.

D. Specialized Hazard Detection: Geo-Intelligence

Specialized agencies are using AI for niche topographical hazards:

- National Remote Sensing Centre (NRSC): Uses AI-processed satellite data to develop Flood Hazard Atlases, identifying regions that are chronically vulnerable.

- DRDO (Defence Research and Development Organisation): Employs AI for Avalanche Forecasting in high-altitude Himalayan regions. These autonomous systems detect remote-sensing-based changes in snowpack stability to predict slides before they occur.

Key Provisions: The Disaster Management (Amendment) Act, 2025

The 2025 Amendment serves as the legal backbone for these technological interventions:

- Data Centralization: It mandates the creation of a National Disaster Database where AI can draw "training data" from historical disasters.

- Statutory Integration of Tech: Explicitly recognizes the role of AI/ML in the official protocols for early warning and risk assessment.

- Private Sector Participation: Encourages partnerships with tech firms for the development of "Disaster-Tech" solutions.

Challenges and Way Forward

While AI offers immense potential, several hurdles remain for India:

- Data Quality: AI is only as good as the data it is trained on; sparse historical data in certain remote regions can lead to "algorithmic bias."

- Last-Mile Connectivity: An AI-generated warning is only effective if it reaches a farmer in a remote village in time.

- Ethics of Automation: Ensuring that human oversight remains central to life-and-death evacuation decisions.

Conclusion

The integration of AI into disaster management represents a paradigm shift in India's governance. By leveraging tools from the IMD, CWC, and DRDO, India is building a "Digital Shield" against natural calamities. For a developing economy, this transition is not merely a technological upgrade but a vital necessity to protect its human capital and economic infrastructure from the increasing volatility of climate change.

Union Budget 2026–27: Growth, Inclusion and Structural Transformation

- 02 Feb 2026

In News:

The Union Budget 2026–27 is anchored in a threefold developmental framework accelerating economic growth, building human capacity, and ensuring inclusive participation. At a time when the global economy faces supply chain realignments, technological disruption, and resource insecurity, the Budget attempts to position India as a resilient, innovation-driven, and socially inclusive economy.

I. Growth Strategy: Investment-Led and Technology-Driven

A defining feature of the Budget is the continued emphasis on public capital expenditure, raised to ?12.2 lakh crore. This reinforces the government’s belief that infrastructure spending crowds in private investment, enhances productivity, and generates employment.

The push spans:

- High-speed rail corridors and freight infrastructure

- Expansion of National Waterways for cost-effective logistics

- Development of City Economic Regions (CERs) to leverage urban agglomeration benefits

These measures reflect a shift from isolated project-based development to integrated regional growth planning.

The Budget also promotes strategic manufacturing and high-technology sectors. The Biopharma SHAKTI initiative (?10,000 crore outlay) aims to develop domestic capabilities in biologics and biosimilars, reducing import dependence while addressing India’s rising non-communicable disease burden. This aligns with the broader push toward knowledge-intensive industrialisation.

Simultaneously, the ?10,000 crore SME Growth Fund recognises MSMEs as drivers of employment and innovation, moving beyond survival support toward scaling globally competitive firms.

II. Human Capital: From Demographic Dividend to Skilled Workforce

The Budget acknowledges that economic growth without skill formation risks jobless expansion. Hence, it invests in education, skilling, and sector-specific workforce creation.

- AVGC labs in schools and colleges support India’s emerging digital content industry.

- Establishment of girls’ hostels in STEM districts addresses gender gaps in higher education.

- A National Institute of Hospitality and guide training scheme link skilling with tourism-led growth.

Healthcare is treated not only as welfare but also as an employment-intensive care economy. The proposal for Regional Medical Hubs integrates healthcare delivery, research, and medical tourism, positioning India as a global health services destination.

III. Inclusive Growth and Social Sector Interventions

The third pillar of the Budget centres on inclusion. Schemes such as Bharat VISTAAR, an AI-based multilingual agricultural advisory, aim to democratise digital infrastructure for farmers, thereby reducing information asymmetry and climate risk.

Similarly, SHE-Marts build on SHG-based mobilisation to promote women’s entrepreneurship, signalling a shift from credit access to market integration and enterprise ownership.

Mental health infrastructure expansion, regional development in the Northeast, and targeted tourism circuits indicate an attempt to address geographical and social imbalances.

IV. Fiscal Prudence with Growth Orientation

Despite higher expenditure, fiscal consolidation remains on track:

- Fiscal deficit projected at 4.3% of GDP

- Debt-to-GDP ratio on a declining trajectory

This suggests a calibrated approach where growth-enhancing capex is prioritised while maintaining macroeconomic credibility.

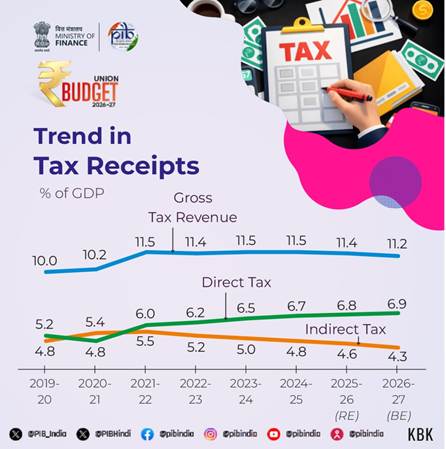

V. Tax Reforms: Simplification and Competitiveness

The introduction of the New Income Tax Act (2025) aims to simplify compliance and reduce litigation. Rationalisation of penalties, decriminalisation of minor offences, and automated safe harbour provisions for IT services improve the ease of doing business.

In a bid to attract global capital, tax incentives for data centres, cloud services, and non-resident investors indicate a strategy to integrate India into global value chains in digital and high-tech domains.

VI. Trade Facilitation and Industrial Policy

Customs reforms reduce duties on inputs for critical minerals, clean energy, aviation, and pharmaceuticals, supporting domestic manufacturing. Digitisation of cargo clearance, AI-based risk assessment, and warehouse reforms enhance trade efficiency and logistics competitiveness.

Conclusion

The Union Budget 2026–27 reflects a structural transition in India’s development model—from consumption-led growth to investment, innovation, and inclusion-led expansion. By combining infrastructure investment, industrial policy, human capital formation, and digital governance, the Budget attempts to align short-term growth impulses with the long-term goal of Viksit Bharat. The key challenge lies in effective implementation and coordination with states, which will determine whether these ambitions translate into broad-based socio-economic transformation.

DefenceAtmanirbharta

- 24 Nov 2025

In News:

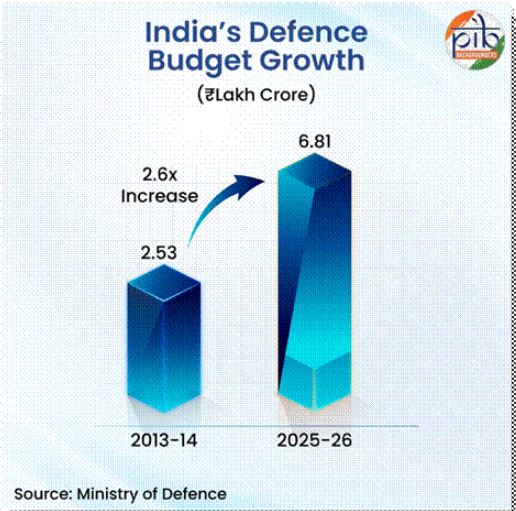

India’s defence sector has undergone a structural transformation over the past decade, marked by record production, expanding exports, and deepening indigenisation. In FY 2024–25, India achieved its highest-ever defence production of ?1.54 lakh crore, while defence exports touched a record ?23,622 crore, reflecting the tangible outcomes of the Atmanirbhar Bharat vision in the strategic domain. This shift signifies India’s transition from one of the world’s largest defence importers to an emerging global manufacturing and export hub.

Rising Production and Export Trajectory

Indigenous defence production rose sharply from ?46,429 crore in FY 2014–15 to ?1,27,434 crore in FY 2023–24, registering a growth of about 174%. This expansion has been supported by sustained budgetary commitment, with the defence budget increasing from ?2.53 lakh crore (2013–14) to ?6.81 lakh crore (2025–26). In FY 2024–25 alone, the Ministry of Defence signed 193 contracts worth ?2.09 lakh crore, of which 177 contracts were awarded to domestic industry, reinforcing the “Buy Indian” approach.

Defence exports, once negligible at less than ?1,000 crore in 2014, have grown steadily, with India now exporting to 80–100 countries. Both Defence Public Sector Undertakings (DPSUs) and the private sector have contributed, with the latter’s share rising to 23%, supported by nearly 16,000 MSMEs supplying subsystems, components, and niche technologies.

Policy Reforms Driving Self-Reliance

This growth has been underpinned by far-reaching reforms. The Defence Acquisition Procedure (DAP) 2020prioritised the Buy (Indian–IDDM) category, streamlined approvals, and embedded advanced technologies such as AI, cyber, and space systems into procurement. Complementing this, the Defence Procurement Manual (DPM) 2025 simplified revenue procurement worth nearly ?1 lakh crore annually, standardised procedures, enhanced digitalisation, and reduced compliance burdens for industry.

Other key enablers include Positive Indigenisation Lists restricting imports of thousands of items, liberalisedFDI norms (74% automatic, 100% via approval), the ?1 lakh crore Research, Development and Innovation (RDI) Scheme, and innovation platforms such as iDEX and the Technology Development Fund. The restructuring of the Ordnance Factory Board into seven DPSUs improved autonomy and efficiency, while Defence Industrial Corridors in Uttar Pradesh and Tamil Nadu attracted over ?9,000 crore in investments, creating manufacturing clusters.

Defence Exports as Strategic Outreach

Export facilitation has been simplified through digital authorisation portals, Open General Export Licences, and rationalised SOPs, resulting in faster clearances and a wider exporter base. Defence exports are increasingly viewed as instruments of diplomacy, fostering interoperability, long-term partnerships, and strategic trust through training, maintenance, and logistics support alongside equipment sales.

Persistent Challenges

Despite progress, challenges remain. India still depends on imports for critical technologies such as propulsion systems, advanced sensors, electronics, and special materials. Production scale is yet to fully match the Armed Forces’ growing requirements, and DPSUs face stiff competition in global markets. Policy–implementation gaps, bureaucratic delays, and dependence on foreign supply chains continue to constrain competitiveness.

Way Forward

Sustaining momentum requires deep-tech capability building, higher defence R&D spending, stronger private-sector participation, and accelerated procurement reforms. Leveraging export diplomacy, long-term procurement commitments, and ecosystem-based innovation can help India achieve its targets of ?3 lakh crore defence production and ?50,000 crore exports by 2029.

Conclusion

India’s defence sector has entered a decisive phase of Atmanirbharta, with record production, rising exports, and a broad-based industrial ecosystem. If structural reforms are consistently implemented and technological depth is strengthened, India is well-positioned to emerge as a globally competitive defence manufacturing hub by the end of this decade, enhancing both national security and economic growth.

Comprehensive Modular Survey: Education 2025

- 01 Sep 2025

In News:

The Comprehensive Modular Survey: Education (CMS:E), 2025, conducted under the 80th round of the National Sample Survey (NSS), provides valuable insights into household expenditure, enrolment trends, and private coaching patterns in school education.

Covering 52,085 households and 57,742 students, this survey, conducted through Computer-Assisted Personal Interviews (CAPI), offers nationally representative data at a critical juncture when India’s education sector is undergoing reforms under NEP 2020 and rapid digital transformation.

Key Findings of CMS: Education 2025

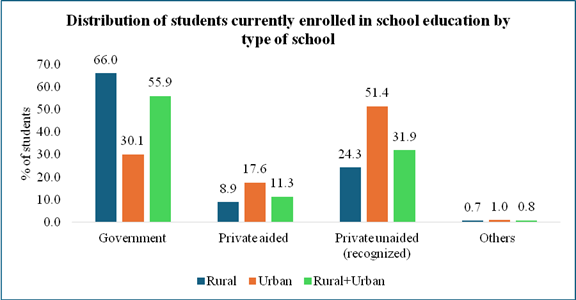

1. Enrolment Patterns

- Government schools dominate enrolment at 55.9%, with higher presence in rural areas (66%) compared to urban (30.1%).

- Private unaided schools account for 31.9% of enrolment, with stronger urban dominance.

2. Education Expenditure

- Average household spending per student:

- Government schools – ?2,863

- Non-government schools – ?25,002

- Overall, expenditure is significantly higher in urban areas (?23,470) than in rural areas (?8,382).

- Course fees constitute the largest expense (?7,111), followed by textbooks and stationery (?2,002).

3. Private Coaching

- Nearly 27% of students availed coaching, higher in urban areas (30.7%) than rural (25.5%).

- Expenditure gap: ?3,988 per student annually in urban areas vs ?1,793 in rural areas.

- At the higher secondary level, coaching costs rise to ?9,950 in urban areas compared to ?4,548 in rural areas.

4. Sources of Education Finance

- 95% of educational expenses were funded by household members.

- Only 1.2% students cited government scholarships as their primary funding source, highlighting weak institutional financial support.

Structural Developments in India’s Education Sector

- Digital and STEM Education: Initiatives like PM e-Vidya and Atal Tinkering Labs (8,000+ labs) promote digital and innovation-driven learning. India’s edtech sector attracted USD 3.94 billion (FY22), projected to grow further.

- Vocational and Skill Integration: NEP 2020 emphasizes skilling; the Union Budget 2025–26 allocated ?500 crore for AI Centres of Excellence in education.

- Rising Private Investment: With 100% FDI permitted, the Indian education market is projected to reach USD 125.8 billion by 2032.

- Higher Education Expansion: India now has 1,362 universities and 52,538 colleges, with Gross Enrolment Ratio (GER) rising to 28.4% (FY25).

- Multilingual & Inclusive Education: Under NEP 2020, focus on regional languages and digital content aims to bridge disparities.

Challenges in Indian Education

- Infrastructure Gaps – Only 47% schools have drinking water; 53% have separate girls’ toilets (2023 data).

- Teacher Shortage – Over 4,500 secondary teachers lack proper training; sanctioned positions declined by 6% (2021–24).

- Low Public Spending – India spends 3–4% of GDP on education, below NEP’s target of 6%.

- Socio-Economic Disparities – Tribal and disadvantaged children face linguistic and access barriers.

- Learning Outcomes – 75% of Class 3 students cannot read Grade 2 text, highlighting rote learning dependence.

- Digital Divide – Only 18.47% of rural schools have internet, compared to 47.29% in urban areas.

- Gender Barriers – 33% of girls drop out due to domestic responsibilities (UNICEF).

Way Forward

- Enhanced Investment in infrastructure, teacher training, and digital access.

- Targeted scholarships and financial aid to reduce household burden.

- Curriculum reforms to shift from rote learning to competency-based assessments (e.g., PARAKH).

- Inclusive education policies for tribal, rural, and girl students.

- Public-Private Partnerships to leverage innovation, funding, and technology.

Conclusion

The CMS: Education 2025 survey underscores the centrality of government schools, the rising cost burden on families, and the growing role of private coaching in shaping education outcomes. While India is witnessing rapid expansion, digitalization, and global investment, challenges of equity, quality, and access persist. Addressing these gaps through sustained policy focus, enhanced funding, and inclusive reforms is essential for realizing the NEP 2020 vision and achieving SDG 4: Quality Education.

NITI Aayog’s Framework for Future Pandemic Preparedness

- 02 Dec 2024

Introduction

In response to the evolving threat of pandemics, NITI Aayog has released an Expert Group report titled "Future Pandemic Preparedness and Emergency Response — A Framework for Action." The report offers a strategic blueprint for India to enhance its pandemic preparedness, drawing from the lessons learned during the COVID-19 crisis and global best practices. This framework aims to create a rapid, well-coordinated response system for future public health emergencies.

Rationale Behind the Expert Group

The COVID-19 pandemic underscored the vulnerability of global and national health systems to emerging infectious diseases. As future pandemics are inevitable, especially with increasing zoonotic threats, India has taken a proactive step in planning for such eventualities. The WHO has warned that 75% of future pandemics may be zoonotic, caused by pathogens transmitted from animals to humans.

Key Findings from COVID-19 Response

India's response to COVID-19 highlighted several strengths and weaknesses in the public health system. Key efforts included developing vaccines, enhancing research and development frameworks, and deploying digital tools for data management across its 1.4 billion population. However, gaps were identified in governance, data management, and cross-sectoral coordination. These lessons have been integrated into the expert group’s framework for future preparedness.

The 100-Day Response Framework

A crucial aspect of the report is the emphasis on the first 100 days of a pandemic. The expert group argues that a rapid response within this period is essential for minimizing the impact of any outbreak. The framework outlines a detailed roadmap for preparedness, which includes tracking, testing, treating, and managing outbreaks efficiently. A robust system for quick deployment of countermeasures, including vaccines and treatments, is pivotal during these critical days.

Four Pillars of Pandemic Preparedness

The report's recommendations are organized around four pillars:

- Governance, Legislation, Finance, and Management:

- Proposes a new Public Health Emergency Management Act (PHEMA) to address modern pandemic needs.

- Creation of an empowered group of secretaries (EGoS) for rapid decision-making and coordination.

- Data Management, Surveillance, and Predictive Tools:

- Calls for a unified data platform to aggregate and analyze data for timely decision-making.

- Emphasizes strengthening genomic surveillance and establishing a national biosecurity network.

- Research, Innovation, and Infrastructure:

- Recommends a high-risk innovation fund to support research on diagnostics, vaccines, and therapeutics.

- Suggests enhancing manufacturing capacity and building biosafety containment facilities.

- Partnerships and Community Engagement:

- Stresses the importance of private sector involvement and community engagement in managing pandemics.

- Proposes a risk communication unit at the National Centre for Disease Control (NCDC) to manage public information and prevent misinformation.

International and National Collaboration

The report underscores the need for cross-border collaboration, aligning India’s efforts with international frameworks such as the WHO’s revised International Health Regulations and the Pandemic Accord negotiations. Collaboration with global institutions, academia, and the private sector is essential for sharing data, technology, and expertise during health crises.

Lessons from Past Epidemics

The report draws lessons from several past epidemics, including SARS, H1N1, and Ebola, which revealed the importance of timely diagnostics, coordinated surveillance, and rapid response. These lessons highlight the need for stronger international regulations, integrated data systems, and enhanced public-private partnerships in tackling future pandemics.

Conclusion and Recommendations

The framework offers actionable recommendations to strengthen India’s pandemic preparedness. From institutionalizing governance structures and creating a dedicated pandemic fund to enhancing surveillance and fostering innovation, these steps are designed to ensure rapid response and minimize the impact of future health crises. By focusing on governance, data management, research, and community partnerships, India aims to build a resilient health system capable of facing future challenges effectively.

Pradhan Mantri Mudra Yojana (PMMY)

- 27 Oct 2024

Introduction

The Pradhan Mantri Mudra Yojana (PMMY) was launched by Prime Minister Narendra Modi on April 8, 2015, with the aim of providing financial support to non-corporate, non-farm small and micro enterprises in India. Through this initiative, loans are provided to individuals and small businesses who are unable to access formal institutional finance.

In the Union Budget 2024-25, Finance Minister Nirmala Sitharaman announced an increase in the loan limit under PMMY from ?10 lakh to ?20 lakh, with the introduction of a new loan category, Tarun Plus, aimed at fostering growth in the entrepreneurial sector.

Key Features of the Pradhan Mantri Mudra Yojana

Loan Limit Increase

- Loan Limit Raised: The loan limit has been increased from ?10 lakh to ?20 lakh for eligible entrepreneurs.

- New Loan Category: The newly introduced Tarun Plus category caters to entrepreneurs who have previously availed and successfully repaid loans under the Tarun category.

- Credit Guarantee: The Credit Guarantee Fund for Micro Units (CGFMU) will cover these enhanced loans, further ensuring the security of micro-enterprises.

Categories of MUDRA Loans

PMMY provides collateral-free loans through financial institutions like Scheduled Commercial Banks, Regional Rural Banks (RRBs), Small Finance Banks (SFBs), Non-Banking Financial Companies (NBFCs), and Micro Finance Institutions (MFIs). These loans are provided for income-generating activities in sectors like manufacturing, trading, services, and allied agriculture activities.

Objectives of PMMY

- Financial Inclusion: PMMY targets marginalized and socio-economically neglected sections of society, promoting financial inclusivity.

- Support to Small Businesses: By providing affordable loans, the scheme encourages small-scale entrepreneurs, particularly women and minority groups, to establish and expand their businesses.

- Fostering Entrepreneurship: PMMY aims to unlock the potential of India’s entrepreneurial spirit, especially in rural and underserved areas.

MUDRA: The Institutional Backbone

Role of Micro Units Development & Refinance Agency Ltd. (MUDRA)

MUDRA is the primary institution set up by the Government of India to manage and implement the Mudra Yojana. It acts as a refinancing agency that provides financial support to small and micro-enterprises by working through financial intermediaries, such as banks and micro-finance institutions.

Funding Sources

- Scheduled Commercial Banks

- Regional Rural Banks (RRBs)

- Small Finance Banks (SFBs)

- Non-Banking Financial Companies (NBFCs)

- Micro Finance Institutions (MFIs)

Application Process

Applicants can avail loans through any of the aforementioned financial institutions or apply online via the Udyami Mitra Portal.

Benefits of Pradhan Mantri Mudra Yojana

- Collateral-free Loans: No security is required to obtain loans, which reduces the financial burden on borrowers.

- Easily Accessible: PMMY loans are available across India, making them accessible to entrepreneurs in both rural and urban areas.

- Quick and Flexible Loans: Loans can be disbursed quickly with flexible repayment terms (up to 7 years).

- Empowering Women Entrepreneurs: The scheme offers special incentives for women entrepreneurs, helping them to establish and grow their businesses.

- Support to Rural Areas: Special emphasis on empowering rural enterprises and reducing regional disparities.

- MUDRA Card: The MUDRA Card is a RuPay debit card that allows borrowers to access funds through an overdraft facility, enhancing liquidity for businesses.

- No Default Penalty: In case of loan defaults due to unforeseen circumstances, the government will step in to reduce the burden on entrepreneurs.

Categories of Loans Under PMMY

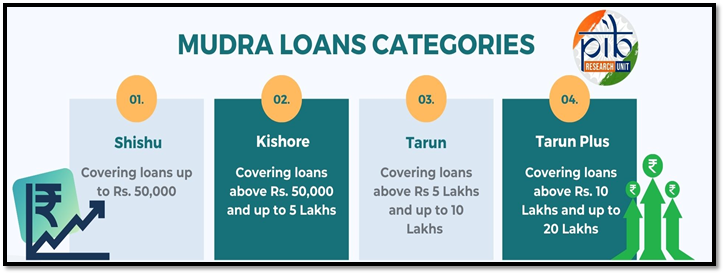

1. Shishu Category: Loans up to ?50,000

- Targeted at micro-enterprises at the initial stage of their business journey.

2. Kishore Category: Loans between ?50,000 and ?5 lakh

- Targeted at enterprises looking to expand their operations and upgrade their infrastructure.

3. Tarun Category: Loans between ?5 lakh and ?10 lakh

- For established businesses that are in need of funds to scale up.

4. Tarun Plus: Loans between ?10 lakh and ?20 lakh

- A new category designed for entrepreneurs who have repaid loans under the Tarun category and wish to further expand their business.

Achievements of PMMY (2023-24)

- Total Loans Sanctioned: ?5.4 trillion across 66.8 million loans in FY 2023-24.

- Loans Disbursed: Significant amounts were disbursed under each category:

- Shishu: ?1,08,472.51 crore

- Kishore: ?1,00,370.49 crore

- Tarun: ?13,454.27 crore

- Women Borrowers: A large share of loans have gone to women entrepreneurs, ensuring gender inclusivity.

- Minority Borrowers: The scheme also emphasizes financial empowerment of minority communities.

- NPA Reduction: The Non-Performing Assets (NPA) in Mudra loans have reduced to 3.4% in FY 2024, compared to higher levels in earlier years.

Digital Tools and Support Systems

MUDRA MITRA App

The MUDRA MITRA mobile app helps users access information about the PMMY scheme, loan application procedures, and other resources. The app is available for download on Google Play Store and Apple App Store.

Online Loan Application

Entrepreneurs can apply for loans online via portals such as PSBloansin59minutes and Udyamimitra, providing greater convenience and accessibility.

Steps to Improve Implementation

- Handholding Support: Assistance in submitting loan applications is available for applicants.

- Intensive Awareness Campaigns: The government conducts publicity campaigns to raise awareness about PMMY.

- Simplified Loan Process: The loan application forms have been simplified to encourage wider participation.

- Performance Monitoring: Regular monitoring of PMMY implementation to ensure its success.

- Interest Subvention: A 2% interest subvention is offered for prompt repayment of Shishu loans.

Conclusion

The Pradhan Mantri Mudra Yojana has been a transformative scheme in fostering entrepreneurship and ensuring financial inclusion for small and micro-businesses across India. With the recent increase in loan limits and the addition of the Tarun Plus category, the scheme continues to empower emerging entrepreneurs and provides a crucial lifeline for business growth and sustainability. By supporting women, minorities, and new entrepreneurs, PMMY has contributed significantly to economic upliftment and inclusive growth in the country.