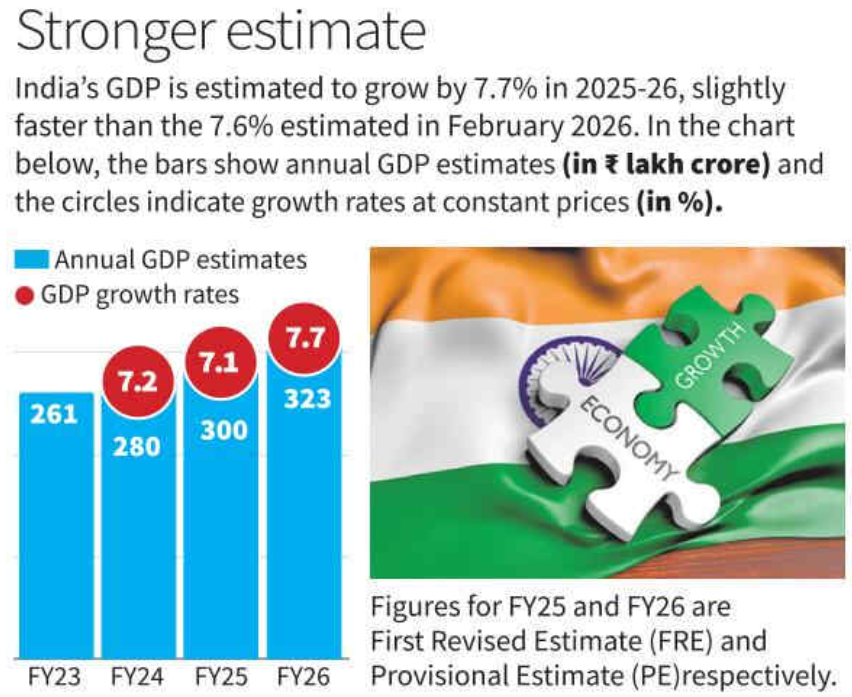

India’s GDP Growth at 7.7% in FY 2025–26

- 10 Jun 2026

In News:

The Ministry of Statistics and Programme Implementation (MoSPI) has released the Provisional Estimates of National Income, placing India’s GDP growth at 7.7% in FY 2025–26, slightly higher than the 7.6% estimate released earlier in February 2026. The latest figures reaffirm India's position as one of the world's fastest-growing major economies despite global economic and geopolitical uncertainties.

What is GDP?

- Gross Domestic Product (GDP) measures the total monetary value of all final goods and services produced within a country's borders during a specific period. It is the most widely used indicator of economic growth and overall economic health.

Key Highlights of the Estimates

- India's economy recorded a robust expansion during FY 2025–26, with real GDP growth reaching 7.7%, while growth in the fourth quarter (Q4) stood at 7.8%, indicating sustained economic momentum.

- Growth was driven primarily by strong performance in manufacturing and services. The manufacturing sector expanded by 7%, reflecting improving industrial activity, while the broad services segment comprising trade, transport, hotels, communication and related services registered an impressive 11% growth, emerging as the key growth driver.

- Domestic demand also remained strong. Private Final Consumption Expenditure (PFCE), a key indicator of household spending, grew by 7.2%, signalling resilient consumer demand. At the same time, Gross Fixed Capital Formation (GFCF), which reflects investment in productive assets, increased by 8.2%, pointing towards sustained investment activity in the economy.

- Agriculture recorded moderate but stable growth of around 4%, supported by favourable monsoon conditions and improved rural demand, though its growth remained lower than that of manufacturing and services.

Significance

The latest GDP estimates highlight the resilience of India's domestic economy amid external challenges such as geopolitical conflicts, global trade uncertainties and slowing growth in several advanced economies.

Strong growth in manufacturing, services, consumption and investment is important because it:

- Supports employment generation.

- Increases household incomes and consumer spending.

- Enhances government tax revenues and fiscal capacity.

- Encourages private sector investment.

- Strengthens India's attractiveness as a global investment destination.

The data also suggests that India's growth continues to be driven by a combination of domestic consumption, capital formation and services-sector expansion, making the economy relatively less vulnerable to external shocks.

End of the ‘Cheap Money’ Era

- 03 Jun 2026

In News:

The Reserve Bank of India (RBI), in its Annual Report 2025–26, has cautioned about rising sovereign bond yields across major economies and the possibility of a reversal in monetary easing by global central banks. This signals the gradual end of the long phase of ultra-low interest rates and abundant global liquidity that characterized the post-2008 and post-pandemic world economy.

Understanding the Context

A government bond is a debt instrument issued by a sovereign government to raise funds. In return, the government pays periodic interest and repays the principal at maturity. Since sovereign governments back these securities, they are generally considered among the safest financial assets.

The return earned on these securities is known as the bond yield, which acts as a benchmark for interest rates across the economy. Higher bond yields typically translate into higher borrowing costs for governments, businesses, and households.

The era of cheap money was largely driven by Quantitative Easing (QE), a monetary policy under which central banks created new money to purchase government bonds and long-term assets. This increased liquidity, reduced interest rates, and encouraged lending and investment.

The Rise and Fall of Cheap Global Money

Following the 2008 Global Financial Crisis and later the COVID-19 pandemic, central banks in advanced economies maintained exceptionally low interest rates and pursued aggressive QE policies.

As a result:

- US bond yields declined from over 6% in the late 1990s and early 2000s to around 0.9% during 2020–21.

- UK yields fell from 5.4% to 0.4%.

- Japan's yields approached zero, and even turned negative during 2016–17 and 2019–20.

This abundance of low-cost capital pushed global investors towards emerging markets such as India in search of higher returns.

However, the situation has changed dramatically. Supply-chain disruptions after COVID-19, the Russia–Ukraine conflict, tariff actions under the Trump administration in 2025, and the ongoing US–Israel versus Iran conflict have revived inflationary pressures globally. Consequently, central banks have moved away from ultra-loose monetary policies.

Rising Global Bond Yields

The reversal is visible in sovereign bond markets:

- Japan: Average yield of 1.8% in 2025–26, rising to 2.5%, with a peak of 2.8% in May 2026.

- United States: Average yield of 4.2%, rising to 4.4%, with a high of 4.7%.

- United Kingdom: Average yield of 4.6%, increasing to 4.9%, with a high of 5.2%.

These figures indicate that global capital is becoming increasingly expensive.

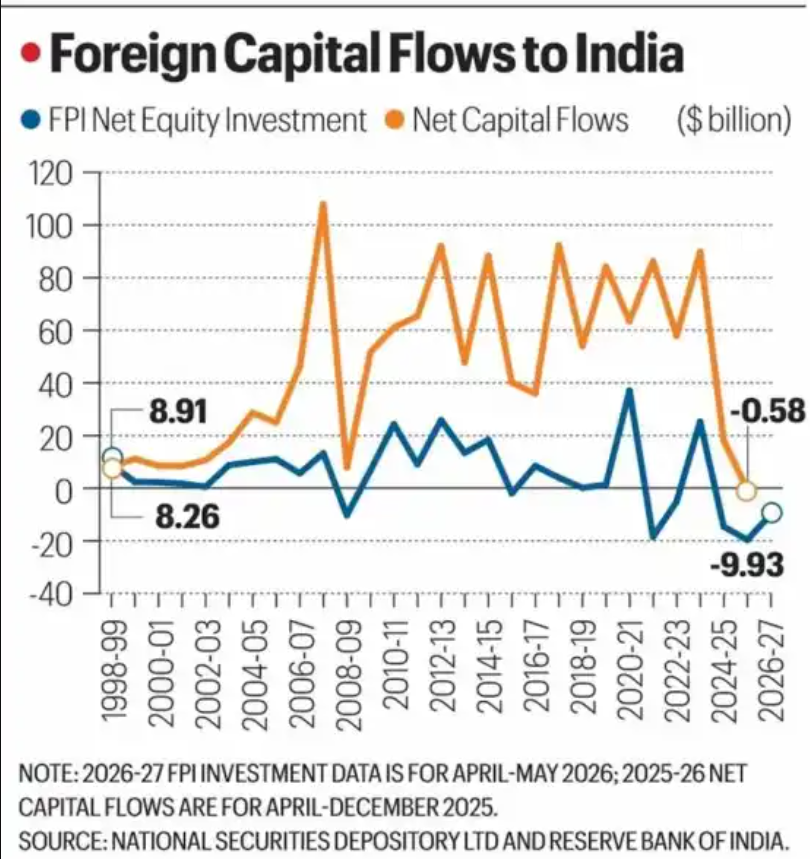

Implications for India

India benefited significantly from global liquidity during the cheap-money era. Net capital inflows rose from $8.3 billion in 1998–99 to a record $107.9 billion in 2007–08, and averaged $67.3 billion annually between 2009–10 and 2023–24. However, inflows fell sharply to $18 billion in 2024–25, while the first nine months of 2025–26 recorded net capital outflows of $580 million.

Another concern is the narrowing yield gap between Indian and US government bonds. India's 10-year government bond yield is around 7%, while the US 10-year Treasury yield is about 4.5%, leaving a differential of only 2.5 percentage points, compared to a historical average of more than 4 percentage points. After accounting for rupee depreciation and the safe-haven appeal of US Treasuries, Indian assets become relatively less attractive to foreign investors.

This could result in:

- Lower foreign capital inflows.

- Increased pressure on the rupee.

- Higher borrowing costs for governments and businesses.

- Greater stock market volatility.

- Challenges in financing current account deficits.

The Way Forward

In a world where capital is no longer abundant and cheap, India must increasingly rely on its own economic fundamentals. Sustaining high GDP growth, maintaining macroeconomic stability, expanding manufacturing through initiatives such as Make in India and PLI schemes, deepening domestic financial markets, and attracting stable long-term FDI will be crucial.

The RBI's warning highlights a broader structural shift in the global economy. As the era of easy money fades, countries will have to compete for investment on the basis of growth prospects, policy credibility, and economic resilience rather than merely benefiting from excess global liquidity.

India's Semiconductor Roadmap: NITI Aayog's 10-Year Vision

- 06 Jun 2026

In News:

Union Finance Minister Nirmala Sitharaman and IT Minister Ashwini Vaishnaw jointly launched the NITI Aayog Frontier Tech Hub's report titled "Future of India's Semiconductor Industry" — India's first comprehensive 10-year roadmap for the semiconductor sector. The joint launch signals cross-ministerial ownership across Finance, MeitY, and NITI Aayog.

India's Current Status

- India currently does not possess a fully operational semiconductor fabrication plant. The first fab, expected in Dholera, Gujarat, may become operational by 2028. Around 10 semiconductor projects are under various stages of development. India imports nearly all its semiconductor requirements, making the economy vulnerable to global supply chain disruptions.

- The Union government had earlier launched the India Semiconductor Mission (ISM) with a corpus of ?76,000 crore, providing capital subsidies of over 50% for fabrication units, supporting compound semiconductors, packaging facilities, and design-linked incentives for startups.

Key Findings of the Report

- The report explicitly states that India's local ecosystem is not ready to fully meet domestic demand. Many semiconductor components used in defence systems are sourced from outside India, posing national security risks.

- Taiwan dominates global chip manufacturing; a disruption there could massively impact India's electronics supply chain. Fabrication units require 4–5 years before commencing production, and the sector demands "sustained, mission-mode commitment over a decade or more."

Strategic Vision: $120–150 Billion by 2035

- The report presents a strategic blueprint to establish a USD 120–150 billion semiconductor ecosystem by 2035. Rather than competing in the capital-intensive race for cutting-edge wafer fabrication, the roadmap advocates a "More-than-Moore" strategy focused on mature logic nodes, advanced OSAT (Outsourced Semiconductor Assembly and Test) packaging, and specialised wide-bandgap compound materials.

Capital Requirements and ISM 2.0

- The report estimates state capital expenditure of $45–60 billion over a decade for the second phase (ISM 2.0). The roadmap directly reinforces priorities announced under India Semiconductor Mission 2.0 in Union Budget 2026, marking India's shift from ecosystem creation to ecosystem deepening — from attracting investments to developing deeper capabilities across design, materials, manufacturing, packaging, talent, R&D, and trusted global partnerships.

Strategic Focus Areas

- The report steers away from frontier chips (3–7 nanometre nodes) where risks are very high, and instead prioritises mature and advanced nodes, compound semiconductors for defence and industrial applications, and advanced chip packaging as a "core production pillar." Clear goals include positioning India as a leading global destination for advanced packaging and OSAT, building leadership in compound semiconductor manufacturing, and creating more than 100 advanced semiconductor design IPs.

Trusted Partners and Geopolitics

Priority partner nations identified are the United States, Japan, the European Union, and South Korea — for access to critical tools, technology transfer, and joint R&D. The report implicitly treats China as an adversarial player, reflecting the broader global semiconductor realignment away from Chinese supply chains.

New WPI Series and Transition to Producer Price Index (PPI)

- 05 Jun 2026

In News:

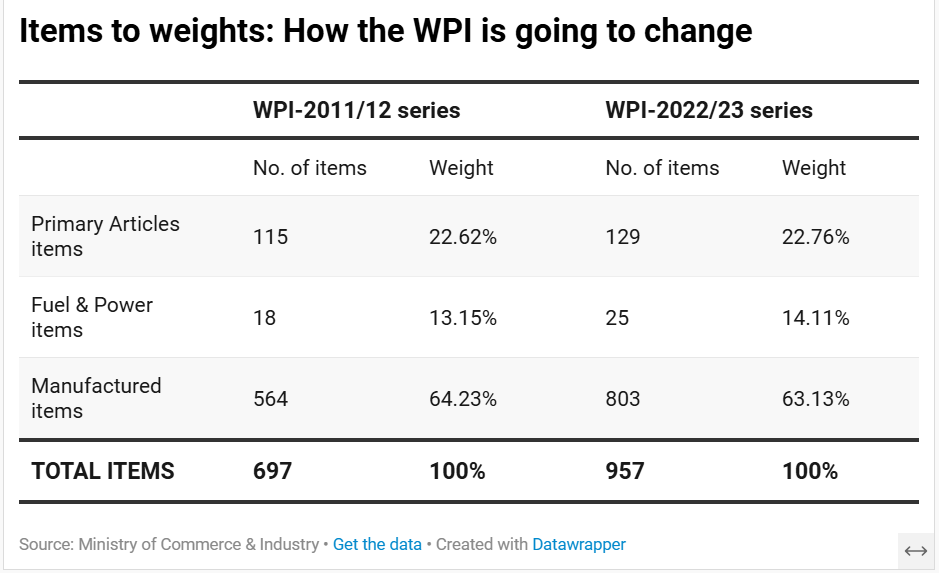

Recently, the Department for Promotion of Industry and Internal Trade (DPIIT) under the Commerce Ministry will release a revised Wholesale Price Index (WPI) series with 2022-23 as the new base year, replacing the 2011-12 series. Simultaneously, India will introduce a comprehensive Producer Price Index (PPI) framework — with the WPI expected to be discontinued by 2031 after a five-year transition.

This reform is part of India's broader statistical overhaul in 2026, following base year revisions to GDP, CPI, and IIP — all updated to 2022-23.

Key Features of the Revised WPI

The commodity basket has been expanded from 697 items to 957 items, with new additions including solar energy, wind energy, nuclear electricity, and other emerging sectors. The revised series will be released with data from May 2026, along with a back-series from April 2023.

The New PPI Framework

Three types of PPIs will be released simultaneously on June 15:

- Output PPI measures prices received by producers at the farm gate or factory gate. It excludes indirect taxes and trade/transport margins. It will initially cover 125 items, expanding to approximately 1,500 items once the WPI is discontinued. This index will be released monthly, with a back-series from April 2023.

- Input PPI (experimental) measures prices paid by producers for inputs, including trade and transport margins. It is being introduced for the manufacturing sector on a trial basis starting March 2026, with validation expected over approximately two years.

- Services PPI covers seven major services: banking, securities transactions, insurance, pension fund management, railways, air passenger transport, and telecommunications. It will be released quarterly, with the first data covering January–March 2026.

All three PPIs carry 2022-23 as the base year.

Why Transition from WPI to PPI?

WPI only tracks goods prices, leaving India's increasingly service-driven economy out of the measurement framework. PPI addresses this gap. Additionally, the output PPI is more consistent with the national accounts framework — the IMF and other global institutions have long advocated PPI adoption for accurately deflating nominal GDP into real GDP. Currently, India uses a combination of WPI and CPI to compute real GDP; once the PPI series stabilises, the output PPI is expected to serve as a more accurate deflator, improving the robustness and international comparability of India's GDP estimates.

Five-Year Transition (2026–2031)

WPI remains widely embedded in long-term procurement contracts, infrastructure agreements, construction projects, and price escalation clauses. To avoid disruption, WPI and PPI will be published in parallel for five years. The Ministry of Finance's Department of Expenditure will issue a circular directing users that fresh long-term contracts extending beyond 2031 should adopt PPI-based escalation mechanisms.

Challenges

Building reliable producer-level price databases — especially for services — is complex. Input PPI remains experimental. Industries and government departments must adapt existing contracts and data frameworks progressively.

Way Forward

- Strengthen data collection infrastructure: Robust producer-level price databases must be built across manufacturing and service sectors. This requires capacity building in statistical agencies, particularly at the district and firm level.

- Validate the Input PPI: The experimental input PPI for manufacturing needs rigorous quality testing and stakeholder feedback over its trial period before it can be formally adopted.

- Expand services coverage: The initial services PPI covers only seven sectors. A roadmap must be developed to progressively include sectors such as healthcare, education, real estate, and IT services.

- Facilitate contractual transition: Government departments, PSUs, and private firms need clear guidelines and legal frameworks to seamlessly migrate price escalation clauses from WPI to PPI in long-term contracts before the 2031 deadline.

- Coordinate with RBI and MoSPI: Close coordination between DPIIT, MoSPI, and the Reserve Bank of India is essential to ensure PPI data is reliable enough to eventually serve as a GDP deflator, strengthening the quality of national income estimates.

Conclusion

India's transition from WPI to PPI is not merely a statistical exercise — it reflects the structural transformation of the Indian economy from a goods-dominated to a services-led one. The simultaneous release of output PPI, input PPI, and services PPI, alongside the revised WPI, marks a decisive step toward aligning India's price measurement architecture with global best practices. Together with the recent revisions in GDP, CPI, and IIP, this reform signals a maturing of India's statistical system, which is foundational to sound policymaking, credible GDP estimation, and investor confidence.

India's EV Transition: Why the Grid Challenge Is Bigger Than the Vehicle

- 20 May 2026

In News:

Rising crude oil prices and recurring geopolitical tensions in the Strait of Hormuz have accelerated India's push toward electric vehicles (EVs). While electric two-wheelers are gaining rapid urban traction owing to affordability and low maintenance costs, the deeper — and largely underappreciated — challenge lies in building a power grid capable of sustaining large-scale transport electrification, particularly in the freight sector.

The Scale of the Problem

India currently has nearly 420 million registered vehicles. Full electrification of this fleet would demand an additional 900–1,100 TWh of electricity annually — effectively requiring the construction of a second large-scale power system alongside the existing one. Even a partial electrification scenario — where half the fleet transitions by 2047 — would still necessitate approximately 500 TWh of additional generation, equivalent to nearly one-third of India's current annual power output.

This arithmetic makes EV adoption not merely a transport policy question but a fundamental energy infrastructure challenge.

The Visibility Trap: Two-Wheelers vs. Freight

Public discourse around EVs is disproportionately focused on electric scooters and motorcycles — politically visible, subsidy-driven, and rapidly growing. Yet their actual grid burden is modest. Electrifying all 309 million two-wheelers would require only 55–75 TWh annually — less than 7% of total projected EV electricity demand.

The real stress lies in freight. India's approximately 6.26 million heavy goods vehicles (HGVs), each covering nearly 60,000 km per year at high energy intensity, would alone require 450–565 TWh annually if electrified. Including medium goods vehicles (MGVs) pushes total freight electricity demand to 500–600 TWh. In effect, electrifying India's roads means electrifying its supply chains, logistics networks, and industrial transport systems — not merely its consumer commute.

The Evening Peak Crisis

A critical structural vulnerability is the evening peak demand problem. If millions of EVs charge simultaneously after sunset — when solar generation drops — the grid faces severe stress, risking shortages, tariff spikes, and supply instability. Several state discoms already report delays in granting high-tension charging connections due to financial distress and inadequate infrastructure.

Solutions exist — time-of-use pricing, workplace daytime charging, battery-swapping networks, and large-scale energy storage — but India currently lacks a mandatory national standard for smart charging, meaning chargers being installed today without grid-responsive capability could become costly liabilities tomorrow.

What the Grid Must Deliver

Sustainable EV growth demands a diversified and clean energy mix. Solar and wind offer scalable, low-cost generation but are weather-dependent. Nuclear energy provides stable low-carbon baseload but requires long lead times. Pumped hydro, battery storage, and limited gas-based generation are essential for balancing supply-demand mismatches.

Critically, expanding coal dependence to power EVs would negate environmental gains — replacing imported oil with imported coal merely shifts India's energy vulnerability while perpetuating high emissions.

Policy Imperatives

Several institutional and regulatory reforms are essential. EV demand projections must be integrated into national capacity planning. Smart-charging standards must be made mandatory for all new infrastructure. Key freight corridors — the Golden Quadrilateral and Dedicated Freight Corridors — require coordinated power planning before electric trucking scales commercially. The Revamped Distribution Sector Scheme (RDSS) must be leveraged to financially strengthen discoms and improve last-mile electricity delivery. Strong inter-ministerial coordination across transport, power, and finance ministries is non-negotiable.

RBI'S Expected Credit Loss Framework

- 03 May 2026

In News:

The Reserve Bank of India's new Expected Credit Loss (ECL) framework, set to take effect from April 1, 2027, is projected to cause a one-time net capital impact of up to 120 basis points on banks' Common Equity Tier-1 (CET-1) ratios, according to CRISIL Ratings. The gross impact could reach up to 170 bps, with existing provisions reducing the net effect.

What is the ECL Framework?

Currently, Indian banks follow the Incurred Loss Model — provisions are made only after a loan shows stress or becomes a Non-Performing Asset (NPA). This reactive approach often recognises risk too late, allowing banks to report healthy books even when early warning signs are visible.

The ECL framework shifts this to a forward-looking approach. Banks must now estimate losses before default by assessing three parameters:

- Probability of Default (PD)

- Loss Given Default (LGD)

- Exposure at Default (EAD)

The new norms are broadly aligned with IFRS 9, the global accounting standard adopted internationally after the 2008 financial crisis to make banking systems more resilient.

Three-Stage Asset Classification

The ECL framework classifies all loan assets into three stages based on credit risk:

Stage I — Low or no significant increase in credit risk. Banks provision for 12-month expected credit loss. Minimum provisioning levels are broadly similar to current norms but serve only as a floor.

Stage II — Significant increase in credit risk, but not yet an NPA. Banks must provision for lifetime expected credit loss. This stage carries the highest transition impact — Stage II assets currently form only 2–2.2% of the banking system, which will help contain the overall burden.

Stage III — Credit-impaired assets or NPAs. Banks recogniselifetime expected credit loss. Provisioning requirements here will also be higher than the current 15% mandate for sub-standard assets.

A critical shift: banks must now provide more for stressed loans before they cross the traditional 90-day overdue NPA threshold.

New NPA Classification Rules

The 90-day NPA classification period remains unchanged, but classification will now occur at the borrower level, not the account level. This means if one loan of a borrower turns bad, all loans of that borrower with the same bank may be treated as NPAs. Upgrading back to standard status requires the borrower to clear all liabilities, not just the defaulted account. This is expected to strengthen credit discipline and prevent selective repayment.

Additionally, the framework now extends provisioning to off-balance-sheet exposures and undisbursed credit limits — meaning banks must account for committed but yet-to-be-disbursed credit lines as well.

Impact on Banks

- Indian banks are well placed to absorb the transition, supported by a healthy CET-1 ratio of around 14% as of March 31, 2026, and steady profitability, with return on assets of about 1.25–1.3% in the last fiscal. Banks will be allowed to spread the transition impact over four financial years, reducing immediate pressure. Additional provisioning buffers already maintained by several lenders will further cushion the effect.

- However, the ECL regime will also lead to a structural rise in credit costs over time. Banks with higher exposure to microfinance, unsecured retail loans, and other riskier segments face greater pressure on margins. Some of these costs may eventually be passed on to borrowers. Banks will need to proactively focus on strengthening net interest margins and controlling operating expenses to absorb the long-term impact.

- Net NPA ratios for most major Indian banks currently stand below 1%, making this an opportune moment for the transition — the sector's strength reduces the risk of disruption.

Significance

The ECL framework marks a structural upgrade in how Indian banks manage credit risk. It enables earlier detection of stress, builds provisioning buffers in advance, reduces the chance of sudden shocks to balance sheets, and aligns India's banking norms with global standards (IFRS 9). For regulators, it improves transparency and accountability in credit risk assessment, making banking supervision more robust.

Revenue Deficit States and Challenge of Fiscal Stability

- 02 May 2026

In News:

The Ministry of Finance’s Monthly Economic Review (April 2026) has issued a stark warning regarding the divergent fiscal paths of Indian states. As the 16th Finance Commission (FC) period commences, the interplay between rising global energy costs, high debt burdens, and the adherence to the "Golden Rule" of financing has become the focal point of India’s federal economic stability.

1. The Federal Fiscal Landscape: Union vs. States

While the Union government demonstrates resilience, the sub-national level reveals a fragmented picture of fiscal health.

The Union: A Cautious Buffer

The Centre has maintained a prudent fiscal stance, anchored by a conservative tax buoyancy assumption of 0.8. A critical innovation is the Economic Stabilisation Fund (ESF), a ?1-trillion buffer designed to absorb external shocks—such as oil price spikes—without derailing the fiscal deficit target. Despite this, external research firms like BMI suggest a potential breach of the 4.3% deficit target, predicting it could hit 4.5% due to emergency energy subsidies.

The States: A Tale of Two Realities

The performance of 18 large states highlights a divide between fiscal discipline and structural stress:

- Revenue Deficit States: 9 out of 18 states are currently failing to cover their daily expenses with their own earnings. Stressed leaders include Himachal Pradesh (-2.4%), Punjab (-2.2%), and Kerala (-2.1%).

- Revenue Surplus Leaders: Conversely, 8 states are projected to run surpluses, led by Odisha (3%), Jharkhand (2.5%), and Uttar Pradesh (1.6%).

2. Critical Concerns: Energy, Inflation, and Debt

The Energy Trap

With the Indian crude basket hovering between USD 113–115 per barrel, the fiscal math is under pressure. The Union is forced to absorb these costs via higher fertilizer and petroleum subsidies, which drains the ESF. For states, this volatility creates a "double whammy": pressure to cut VAT on fuel while simultaneously facing higher costs for public transport and operations.

The Interest Burden and "Degrees of Freedom"

High debt levels are severely limiting the "degrees of freedom" for stressed states. Punjab represents the extreme, spending 22.8% of its total revenue receipts just on interest payments. When nearly a quarter of income is diverted to servicing old debt, little remains for health, education, or infrastructure.

16th Finance Commission Risks

FY 2026-27 marks the transition to the 16th FC recommendations. The primary risk factor is the absence of Revenue Deficit Grants, which were a lifeline for stressed states under the previous commission. States must now rely more on their own tax efforts and performance-based grants (20% of the total allocation).

3. The ‘Golden Rule’ of Fiscal Financing

The Ministry of Finance has specifically warned states against violating the Golden Rule.

- The Principle: A government should borrow only to fund capital projects (investment) and not for day-to-day consumption (salaries, pensions, and subsidies).

- Intergenerational Equity: Borrowing for a bridge is equitable because future generations benefit from the asset while paying the debt. Borrowing for today’s subsidies, however, shifts the cost to the future with no corresponding asset creation.

- Case Study: Odisha vs. Punjab:

- Odisha budgets a fiscal deficit of 3.5%, seemingly high, but it maintains a 3% revenue surplus. This indicates that its borrowing is entirely "productive," used for a massive capital outlay of 6.5% of GSDP.

- Punjab and Kerala, by contrast, are borrowing to fund revenue deficits, effectively "eating into their future."

4. Strategic Roadmap for Strengthening Fiscal Outlook

For the Union Government

- Energy Diplomacy: Moving toward Government-to-Government (G2G) deals with producers like Brazil, Guyana, and Russia to reduce the "risk premium" associated with West Asian conflicts.

- Capex Prioritization: Protecting the budget for high-multiplier sectors such as Semiconductors and Green Hydrogen to sustain a 7% growth trajectory.

- Monetary Coordination: Working with the RBI to stabilize the Rupee and prevent "imported inflation" from ballooning the national debt.

For State Governments

- Revenue Diversification: Reducing reliance on volatile fuel VAT by digitizing and strengthening State Excise and Stamp Duties.

- Green Energy Mandates: Shielding budgets by transitioning public transport to Electric Vehicles (EVs) and adopting solar-powered irrigation (KUSUM scheme) to lower the subsidy burden.

- Performance-Based Compliance: Focusing on property tax reforms to unlock the 20% performance-linked grants introduced by the 16th FC.

Conclusion

The 2026 fiscal outlook is a balancing act between Central resilience and Sub-national vulnerability. Long-term stability in the Indian federal structure hinges on states moving away from "consumption borrowing" toward productive capital investment. Only by adhering to the Golden Rule can states ensure that the current energy crisis does not become a permanent debt trap for future generations.

The Rise and Fall of Paytm Payments Bank: A Landmark Shift in Indian Fintech Regulation

- 26 Apr 2026

In News:

The Reserve Bank of India’s (RBI) decision to cancel the banking licence of Paytm Payments Bank Limited (PPBL), marks a watershed moment in the oversight of India’s digital finance ecosystem. This move, coming more than two years after the initial regulatory curbs, underscores the central bank's unwavering stance on governance and "Chinese wall" separation between fintech innovations and traditional banking discipline.

Understanding the Payments Bank Model

Payments banks were conceptualized as a niche banking category to drive financial inclusion by catering to low-income groups, small businesses, and the migrant labor force.

- Operational Scope: They are permitted to accept demand deposits (currently capped at ?2 lakh per customer) and offer remittance services.

- Restrictive Mandate: Unlike universal banks, they are strictly prohibited from lending or issuing credit cards.

- Safety Net: To safeguard depositors, they must invest at least 75% of their demand deposits in Government Securities (SLR-eligible) with maturities up to one year.

The Road to Cancellation: A Timeline of Scrutiny

The downfall of PPBL was not sudden but the result of a multi-year supervisory struggle regarding "persistent non-compliance."

- 2018 (Initial Red Flags): RBI audits identified critical gaps in KYC (Know Your Customer) compliance. Major violations included a single PAN being linked to thousands of accounts and transactions exceeding regulatory limits, raising severe money laundering alarms.

- March 2022: The RBI formally barred the bank from onboarding new customers.

- October 2023: A significant monetary penalty of ?5.39 crore was imposed for continued lapses.

- January–February 2024: Citing "material supervisory concerns," the RBI prohibited fresh deposits, top-ups in wallets, FASTags, and NCMC accounts.

- April 24, 2026: The final blow—the total cancellation of the banking licence and the initiation of winding-up proceedings before the High Court.

Legal Foundations of the RBI’s Action

The RBI invoked several stringent provisions of the Banking Regulation (BR) Act, 1949 to justify this unprecedented step:

- Section 22(4): Provides the power to withdraw a licence if a bank fails to meet stipulated conditions.

- Section 22(3)(c) & (e): The RBI concluded that the management’s character was prejudicial to public interest and that no "useful purpose" would be served by allowing the entity to continue.

- Section 5(b) and Section 6: These sections effectively prohibit PPBL from conducting any banking or related business with immediate effect.

A primary concern was the lack of an independent "Chinese wall" between PPBL and its parent entity, One97 Communications, which led to significant conflicts of interest and regulatory bypass.

Strategic Impact and Future Outlook

1. For the Paytm Ecosystem: One97 Communications has since moved to a "partner-bank-driven model," forging emergency alliances with entities like Axis Bank and Yes Bank to ensure that the Paytm UPI app remains functional. While the parent company is "legally ring-fenced," the cancellation complicates its path toward obtaining future licences (like an NBFC or a mobile wallet licence).

2. For the Fintech Industry: The "Paytm Case" serves as a stern warning that innovation is not a license for non-compliance. The fintech sector must now institutionalize independent compliance functions that are strictly decoupled from the aggressive growth mandates of their parent tech firms.

3. For Consumer Protection: The RBI has assured that PPBL maintains sufficient liquidity to repay all depositors in full. Most users have already migrated to rivals like PhonePe and Google Pay, but the process of winding up under High Court supervision ensures a structured exit that protects the "sanctity of the ledger."

Conclusion

This episode highlights the Security-Development Nexus in the financial sector. For a "Viksit Bharat" (Developed India), financial stability is as crucial as financial inclusion. The RBI’s action demonstrates that institutional credibility is paramount; even the most popular market players must adhere to the prudential norms that ensure the safety of the Indian banking system.

The Precarious City: Navigating the Crisis of India’s Urban Informal Workforce

- 24 Apr 2026

In News:

Recent worker protests in industrial hubs like Noida have once again brought to the fore the structural vulnerabilities of India’s informal sector. As urban centers transition from traditional industrial hubs to survival-oriented service spaces, the informal workforce—comprising nearly 90% of India’s total labor force—faces an existential crisis characterized by economic exclusion and spatial marginalization.

The Informal Sector: Scope and Economic Significance

The informal sector encompasses economic activities that function outside the ambit of formal regulatory and institutional frameworks. It is a heterogeneous mix including self-employed individuals, daily wage laborers, street vendors, and unregistered micro-enterprises.

- Dominance in Livelihood: Despite the push for formalization, the informal sector remains the backbone of the Indian economy. Even in urban landscapes, formal salaried positions are scarce, leaving the majority of migrants and residents dependent on unstable, low-paying work.

- Structural Vulnerabilities: These workers typically lack written contracts, job security, and any form of institutional social protection. This makes them the first victims of economic shocks, as seen during global pandemics or local industrial downturns.

The Urban Shift: From Production to Survival

India’s urban economic structure is undergoing a profound transformation. The decline of large-scale formal industries—symbolized by the historical closure of textile mills in Mumbai and Ahmedabad—has led to a fragmented labor market.

- The Survival Economy: Cities are increasingly becoming spaces for "social reproduction" rather than industrial production. This means the urban economy is now focused on basic survival needs like housing, food, and low-end services.

- Spatial Marginalization: Approximately 40% of the urban poor live in slums or informal settlements. These areas often lack basic sanitation and legal recognition, forcing workers into hazard-prone environments.

- The Rent Trap: A significant portion of an informal worker's income—often up to 50%—is consumed by rent in these precarious settlements. This leaves little for nutrition, health, or education.

Key Challenges and Policy Gaps

Despite its scale, the informal sector suffers from systemic neglect in urban planning and financial policy.

- Privatization of Essentials: Economic reforms have shifted the state’s role from a service provider to a market facilitator. The resulting privatization of water and electricity has increased the cost of living for those least able to afford it.

- Financial Exclusion and Debt: Lacking collateral, workers are often shunned by formal banking systems. This forces them into the clutches of local moneylenders, leading to a cycle of chronic indebtedness.

- Low Bargaining Power: The fragmented nature of urban labor prevents collective bargaining, leaving workers at the mercy of volatile market demands and predatory middle-men.

Institutional Response and Government Initiatives

The government has launched several flagship initiatives to bridge the formal-informal divide:

- Code on Social Security (2020): A legislative attempt to extend life and disability insurance, maternity benefits, and old-age protection to unorganized workers.

- e-Shram Portal: A national database of unorganized workers designed to facilitate better policy targeting and the seamless delivery of welfare benefits.

- PM SVANidhi: A micro-credit scheme providing collateral-free working capital loans to street vendors to help them resume livelihoods post-disruption.

However, challenges such as digital illiteracy, complex registration processes, and implementation bottlenecks at the local level continue to hinder the reach of these schemes.

The Way Ahead: Towards Inclusive Urban Governance

To address the precariousness of urban labor, a shift in governance philosophy is required:

- Integrating Workers into Governance: Moving beyond top-down policies, cities need inclusive structures such as workers’ councils. These platforms allow informal workers to participate in urban decision-making and advocate for their rights.

- Securing Housing and Services: Urban planning must prioritize affordable housing and protected access to essential services to reduce the "survival cost" of city life.

- Formalization with Protection: While formalizing the economy is a long-term goal, the immediate priority must be providing a "social floor"—a minimum level of social security that stays with the worker, regardless of their employment status.

Conclusion

The protests in Noida are a symptom of a deeper malaise in India’s urban growth story. A truly "Viksit Bharat" (Developed India) cannot be built on the back of an invisible and exploited informal workforce. Recognizing the informal sector not as a transient phase but as a permanent, vital part of the urban fabric is the first step toward creating resilient and inclusive cities.

The Global Economic Pecking Order: Analyzing India’s Shift to the 6th Largest Economy

- 20 Apr 2026

In News:

The global economic landscape of 2026 has witnessed a significant recalibration. According to the IMF’s World Economic Outlook 2026, India has slipped to the position of the world’s 6th largest economy. This development marks a notable shift from 2022, when India famously overtook the United Kingdom to claim the 5th spot. While the ranking shift has generated headlines, a deeper analysis reveals that the change is driven more by currency dynamics and statistical adjustments than by a fundamental loss of economic momentum.

Methodology of Global Rankings

To understand India's current position, it is essential to look at how the IMF determines global rankings. These are measured using Nominal GDP expressed in current US dollars. This calculation relies on two variables:

- Domestic GDP in local currency (the Rupee).

- Exchange Rates against the US dollar.

This methodology creates a "valuation effect." An economy might grow robustly in domestic terms, but if its currency depreciates against the dollar, its global standing in dollar terms can diminish. Conversely, if the British Pound or Japanese Yen strengthens, those nations can leapfrog others even with slower real growth.

The 2026 Economic Standings

As per the 2026 estimates, the global economic hierarchy reflects a massive gap between the "Big Two" and the rest of the world. The United States leads with a GDP exceeding $32 trillion, followed by China at approximately $20 trillion.

The subsequent tier is highly congested, with several nations clustered around the $4 trillion mark:

- Japan: $4.38 trillion

- United Kingdom: $4.27 trillion

- India: $4.15 trillion

Because these economies are so closely matched, even minor fluctuations in data or currency can trigger a "musical chairs" effect in the rankings.

Deconstructing India’s Decline: Three Primary Factors

1. Statistical Revisions and Base Year Changes: The decline was partly triggered by a downward revision of India’s GDP estimates. Following the adoption of a new base year, the government revised the 2025-26 GDP from ?357 lakh crore to ?345 lakh crore. This statistical correction indicated that previous estimates had slightly overstated the economy's size, immediately impacting the dollar conversion.

2. Currency Depreciation (The Valuation Effect): The Indian Rupee faced significant depreciation against the US dollar in 2025-26. Simultaneously, the British Pound and the Japanese Yen showed relative resilience or appreciation. This "double whammy" meant that while India’s economy grew in Rupee terms, its "dollar-denominated size" shrank relative to the UK and Japan.

3. Exchange Rate Volatility: The IMF’s reliance on nominal dollar-based comparisons makes these rankings highly sensitive to the global forex market. In a year of global financial tightening, currency movements often overshadow real production gains in the short-term ranking tables.

Strategic Future Outlook

Economists and the IMF suggest that the slip to the 6th position is a temporary statistical "re-basing" rather than a structural decline. India’s long-term fundamentals including a strong demographic dividend, infrastructure spending, and digital transformation remain intact.

- 2027 Projections: India is expected to regain the 4th largest economy spot as the effects of currency volatility stabilize.

- 2031 Projections: India is on a trajectory to become the 3rd largest economy, likely overtaking Germany, provided it maintains a consistent growth rate and manages inflationary pressures.

The New Consumer Price Index (CPI)

- 16 Apr 2026

In News:

In a significant move to align economic indicators with contemporary consumption patterns, the Ministry of Statistics and Programme Implementation (MoSPI) has transitioned to a new Consumer Price Index (CPI) series with 2024 as the base year. This revision is crucial for the Reserve Bank of India (RBI) and policymakers to accurately gauge the "cost of living" and calibrate monetary policy effectively.

I. Understanding CPI and the Need for Revision

The CPI is the primary gauge of retail inflation in India. It measures price changes in a "basket" of goods and services consumed by typical households.

- Monetary Policy Link: The RBI uses CPI for Inflation Targeting. Changes in CPI directly influence the Repo Rate, pensions, and dearness allowances.

- The Consumption Shift: As the Indian economy evolves, consumption habits move from basic necessities (like food) to discretionary items and services (like electronics and healthcare). Periodic revisions prevent the index from becoming obsolete.

II. Key Features of the 2024 Series

The transition from the previous base year (2012) to 2024 introduces several structural changes:

- Modernized Basket: Obsolete items like CDs and DVDs have been removed. They are replaced by modern essentials such as Bluetooth devices, headphones, and earphones, reflecting the digital transformation of Indian households.

- Reduced Weight of Food: Reflecting "Engel’s Law" (as income rises, the proportion of income spent on food falls), the weightage of food items has been reduced.

- Significance: Lower food weight may reduce the volatility of headline inflation, as food is highly susceptible to monsoon and supply-chain shocks.

- Revised Precious Metals Weight:

- Old Series: Gold (1.08%), Silver (0.11%).

- New Series: Gold/Diamond/Platinum jewellery (0.62%), Silver jewellery (0.31%).

- Impact: Despite the individual weight of gold decreasing, the high volatility of global bullion prices remains a significant driver of headline inflation. For instance, excluding gold and silver in December 2025 would have dropped inflation from 1.33% to a mere 0.26%.

III. Statistical Challenges: The "Apples-to-Oranges" Problem

A major hurdle in adopting a new series is the lack of direct comparability with older data.

- The Comparison Gap: January’s inflation was reported at 2.75% under the new series, while December was 1.33% under the old series. This jump is partly due to the different "baskets" being compared rather than a sudden price surge.

- The Back-Series Debate: To help economists, MoSPI released a back-series to 2013. However, experts argue this is a mechanical adjustment using linking factors rather than a reconstruction of historical data using the new consumption weights.

IV. Implications for Monetary Policy and Governance

The new series provides a more realistic lens for the RBI’s Monetary Policy Committee (MPC):

- Core Inflation Insights: With updated weights for services and non-food items, "Core Inflation" (CPI minus food and fuel) will provide a clearer picture of underlying demand.

- Better Calibration: Accurate data allows the RBI to adjust interest rates more precisely, preventing "over-tightening" or "over-easing" based on outdated consumption data.

- Welfare Schemes: Real-time inflation data ensures that government subsidies and wage adjustments (like MGNREGA wages) stay in sync with the actual cost of living.

From Borrowers to Builders: The Evolution of Women in India’s Credit Market

- 11 Apr 2026

In News:

In a landmark development for financial inclusion and women-led development, NITI Aayog released the second edition of its comprehensive report, "From Borrowers to Builders: Women and India’s Evolving Credit Market”. Prepared under the aegis of the Women Entrepreneurship Platform (WEP) in collaboration with TransUnion CIBIL and MicroSave Consulting (MSC), the report highlights a structural shift where women are transitioning from mere recipients of credit to significant drivers of India's entrepreneurial economy.

Key Highlights: The Quantitative Shift

The report presents a compelling narrative of growth in women's participation in formal credit systems between 2017 and 2025.

- Portfolio Growth: Women borrowers now hold a credit portfolio of ?76 lakh crore, accounting for 26% of the total system credit. This represents a staggering 4.8-fold increase from ?16 lakh crore in 2017.

- Expansion in Business Lending: While retail loans remain dominant, business-purpose loans for women have surged 7.5 times since 2017, now constituting 25% of their total credit value.

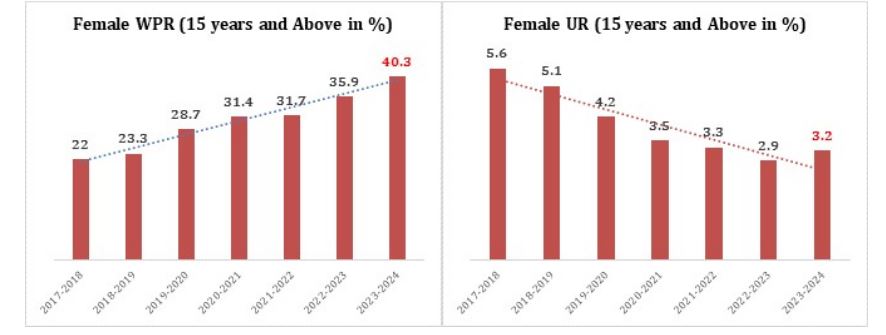

- Credit Penetration: The percentage of credit-active women has nearly doubled, rising from 19% to 36%, representing approximately 16 crore (160 million) active women borrowers.

- Regional Trends: While the South and West remain leaders, Northern states like Bihar and Uttar Pradesh are emerging as high-growth markets, recording business loan Compound Annual Growth Rates (CAGRs) of 59% and 42%, respectively.

- Superior Credit Behavior: The report underscores that women are highly reliable borrowers, with default rates 30% lower than the general market average.

The Role of Digital Public Infrastructure (DPI)

The convergence of DPI—including UPI, e-KYC, and digital identity systems—has been a primary catalyst in reducing entry barriers.

- Speed of Credit: Same-day approvals for consumption loans rose from 34% in 2022 to 45% in 2025.

- Digital Adoption: Among Rural Women Nano-Entrepreneurs (RWNEs), 60–70% now use digital payments, creating a "verifiable cash-flow history" that can be used for credit underwriting.

Challenges to Financial Autonomy

Despite the progress, several structural and behavioral barriers persist:

- Time Poverty: Women face significant "time poverty" due to unpaid care and household responsibilities, limiting their ability to engage consistently with financial tools.

- Shared Resources: The use of shared mobile devices in rural households often constrains independent and private financial decision-making.

- Limited Strategic Control: Many women manage daily business operations but lack final authority over large-scale strategic investments or procurement.

- Microfinance Contraction: The MFI sector has seen a contraction in supply due to rising Non-Performing Assets (NPAs) and concerns over borrower over-indebtedness.

- Complexity Gap: Access to sophisticated products like Cash Credit (CC) and Overdraft (OD) facilities remains low, utilized by only ~4.3% of women-owned entities.

Recommendations for Sustainable Growth

To transition from inclusion to "progression-led participation," the report offers several strategic interventions:

- Flow-Based Underwriting: Lenders should move away from collateral-heavy models toward using UPI transaction data and digital footprints to assess risk for first-time borrowers.

- Gender-Intelligent Products: Designing credit products with flexible repayment schedules that align specifically with the cash-flow cycles of women-led small businesses.

- Project Seher: Expanding credit education programs to improve financial literacy and help women understand the long-term value of their credit scores.

- Leveraging SHGs: Utilizing Self-Help Groups (SHGs) as "trust bridges" to introduce new financial technologies and digital tools.

- End-to-End Digitization: Reducing Turnaround Time (TAT) for secured loans (like housing) by digitizing property valuation and collateral checks.

India’s Defence Export Surge

- 05 Apr 2026

In News:

India’s defence sector has achieved a historic milestone in the financial year 2025-26, with defence exports reaching an all-time high of ?38,424 crore. This represents a staggering 62.66% increase over the previous fiscal year (?23,622 crore). This surge is a testament to India's transition from being one of the world's largest arms importers to an emerging global exporter, driven by the vision of Atmanirbhar Bharat (Self-Reliant India).

Key Highlights of FY 2025-26

The growth in exports is characterized by a robust partnership between the public and private sectors:

- Sectoral Contribution: Defence Public Sector Undertakings (DPSUs) contributed 54.84% (?21,071 crore), while the private sector accounted for 45.16% (?17,353 crore).

- Surging Growth: DPSU exports skyrocketed by 151%, while private firms maintained steady growth with a 14% increase.

- Global Footprint: India now exports defence equipment to more than 80 countries. The number of active exporters has grown to 145, reflecting a more competitive and wider industrial base.

- Budgetary Support: The defence budget has grown significantly to ?6.81 lakh crore in 2025-26, providing the necessary capital for modernization and indigenous production.

Major Exported Products and Destinations

India's export basket has expanded from components to full-scale advanced platforms:

- Key Products: BrahMos Supersonic Cruise Missiles, Akash Surface-to-Air Missile systems, Pinaka Multi-Barrel Rocket Launchers, Advanced Towed Artillery Gun System (ATAGS), Dornier-228 aircraft, and Zen Anti-Drone Systems.

- Top Buyers:

- Components/Sub-systems: United States, France, and Israel (primarily for aero-structures and electronics).

- Indigenous Weapon Systems:Armenia (Akash, Pinaka, ATAGS) and the Philippines (BrahMos).

- Others: UAE, South Korea, Italy, and various nations across Africa and Southeast Asia.

The Strategic Imperative for Indigenisation

The push for domestic manufacturing is rooted in the need for Strategic Autonomy:

- National Security: Reducing dependence on foreign OEMs ensures that supply chains are not disrupted during geopolitical crises or through technology denials (sanctions).

- Economic Efficiency: Indigenous production conserves foreign exchange and creates a "waste-to-wealth" cycle within the domestic economy.

- Tailored Technology: Platforms can be customized for India’s unique terrains—ranging from high-altitude Himalayan regions to tropical maritime zones.

- Technological Sovereignty: Owning the Intellectual Property (IP) allows India to upgrade and modify systems without seeking external permissions.

Key Reforms Driving the Transformation

The Government of India has introduced several structural reforms to facilitate this growth:

- DAP 2020 & IDDM: The Defence Acquisition Procedure (DAP) 2020 prioritizes the Indian-IDDM (Indigenously Designed, Developed, and Manufactured) category as the highest preference for procurement.

- Simplified ‘Make’ Procedures:

- Make-I: Government-funded (up to 70%) development of complex systems.

- Make-II: Industry-funded prototypes with simplified paperwork and fast-track approvals.

- FDI Liberalization: Automatic route for Foreign Direct Investment increased to 74%, and up to 100% via government approval for niche technologies.

- Innovation Ecosystems:

- iDEX (Innovations for Defence Excellence): Grants for startups and MSMEs.

- Technology Development Fund (TDF): Funding up to ?10 crore for R&D in critical technologies.

- Defence Industrial Corridors (DICs): Established in Uttar Pradesh and Tamil Nadu, these hubs have attracted over ?9,145 crore in investment and signed nearly 290 MoUs to build a localized supply chain.

Roadmap to 2029: The Global Hub Vision

The Ministry of Defence has set ambitious targets for the near future:

- Production Target: Reach ?3 lakh crore in annual domestic defence production by 2029.

- Export Target: Aim for ?50,000 crore in annual exports by 2029.

- MSME Integration: Engaging over 16,000 MSMEs to ensure a resilient and tiered manufacturing ecosystem.

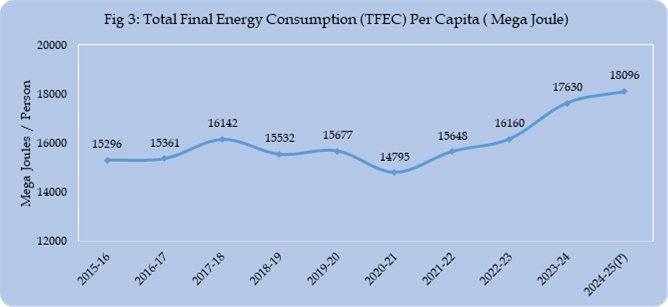

Energy Statistics India 2026

- 03 Apr 2026

In News:

The Ministry of Statistics and Programme Implementation (MoSPI) has released its annual publication, “Energy Statistics India 2026.” This comprehensive dataset integrates information on India’s energy reserves, production, consumption, and trade, providing a pulse check on the nation's energy security and transition trajectory as of March 31, 2025.

Macro-Economic Energy Indicators

During the Financial Year 2024-25, India’s energy sector mirrored the nation’s robust economic growth.

- Primary Energy Supply: The Total Primary Energy Supply (TPES) registered a healthy expansion of 2.95% over the previous year.

- Per-Capita Consumption: Reflecting rising living standards and industrialization, per-capita energy consumption has grown at a Compound Annual Growth Rate (CAGR) of 1.89% over the decade spanning 2015-16 to 2024-25.

- Credit Flow: Financial confidence in the sector has skyrocketed. Investment flows surged from ?1,688 crore in 2021 to ?10,325 crore in 2025, a more than six-fold increase in just four years.

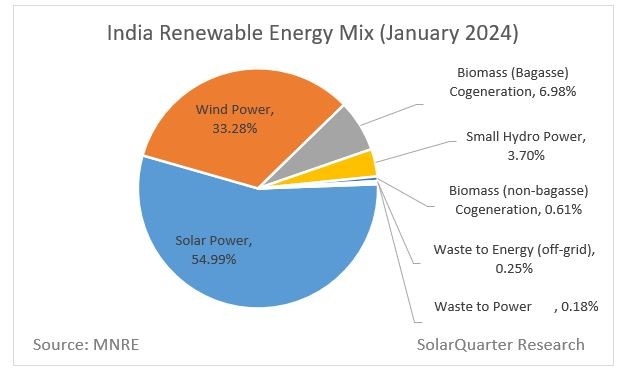

The Renewable Energy Paradigm

India’s renewable energy (RE) sector is the cornerstone of its climate strategy, showing both immense potential and rapid adoption.

- Total Potential: As of March 2025, India’s estimated renewable energy potential stands at a staggering 47,04,043 MW.

- Resource Composition:Solar energy is the dominant pillar, accounting for nearly 71% of this potential. This is followed significantly by wind power and large hydro projects.

- Geographic Concentration: A critical administrative challenge is the spatial distribution of these resources. Over 70% of India's RE potential is clustered in just six states: Rajasthan, Maharashtra, Gujarat, Andhra Pradesh, Karnataka, and Madhya Pradesh.

- Generation Growth: Actual electricity generation from renewable sources (Utility and Non-Utility) has witnessed a robust CAGR of 9.17%, outpacing conventional growth rates.

Continued Reliance on Fossil Fuels

Despite the green surge, the report highlights a persistent structural reality: Coal remains the dominant source of energy, contributing the highest share to the total primary energy supply. This underscores the "Energy Trilemma" India facesbalancing energy security, energy equity, and environmental sustainability.

Key Takeaways for Policy Analysis

- Demand Dynamics: The steady rise in demand reflects sustained economic growth, but it also necessitates a concurrent expansion in generation capacity to prevent supply deficits.

- Infrastructure Imperatives: The geographic concentration of RE in western and southern states creates an urgent need for the Green Energy Corridor and enhanced interstate transmission networks to prevent regional energy imbalances.

- Transition Challenges: The dominance of coal indicates that while the "addition" of green energy is fast, the "replacement" of fossil fuels is a long-term structural challenge.

- Investment Climate: The massive growth in credit flow suggests that policy frameworks like the Production Linked Incentive (PLI) for solar modules and sovereign green bonds are successfully building investor trust.

Fiscal Federalism in India and the Debate over the 41% Tax Devolution

- 12 Mar 2026

In News:

The debate on fiscal federalism in India has intensified following the Union government’s acceptance of the 41% tax devolution recommended by the Sixteenth Finance Commission. While the recommendation appears to maintain the existing share of tax revenues for States, critics argue that structural changes in the fiscal framework may gradually reshape the balance of financial power between the Centre and the States.

Fiscal Federalism in India

Fiscal federalism refers to the division of financial powers, taxation authority, and expenditure responsibilities between different levels of government in a federal system. In India, the Constitution establishes a structured framework for fiscal relations between the Union and the States.

Key constitutional provisions include:

- Articles 268–281: These articles govern the distribution of taxation powers and revenue sharing between the Union and the States.

- Article 280: Provides for the establishment of the Finance Commission, which recommends the sharing of central taxes and grants to States.

- Seventh Schedule: Divides taxation powers between the Union List and the State List.

Since the Union government collects a major share of taxes, the Finance Commission periodically recommends how the divisible pool of central taxes should be distributed among States.

Evolution of Tax Devolution

The share of States in the divisible pool has increased over time:

- 14th Finance Commission: Increased States’ share to 42%.

- 15th Finance Commission: Reduced it slightly to 41% after the reorganisation of Jammu and Kashmir.

- 16th Finance Commission: Recommended retaining the 41% share.

Although the percentage has remained unchanged, analysts argue that the effective transfer of resources to States may be declining.

The Divisible Pool and the Issue of Cesses and Surcharges

The divisible pool represents the portion of central tax revenues that is shared with States. However, certain revenues such as cesses and surcharges are excluded from this pool and are retained entirely by the Union government.

Over time, the share of the divisible pool in gross tax revenue has declined:

- 13th Finance Commission period: 89.2%

- 14th Finance Commission period: 82.1%

- 15th Finance Commission period: 78.3%

This trend implies that even though the States’ share is fixed at 41%, the base from which this percentage is calculated has shrunk, reducing the overall transfer to States.

Key Recommendations of the Sixteenth Finance Commission

The Union government accepted several major recommendations of the Commission, including:

- Retaining 41% tax devolution to States

- Acceptance of the horizontal distribution formula among States

- Approval of grants to local bodies

- Continuation of the disaster management funding framework

However, several structural reforms proposed by the Commission were deferred. These include:

- Reform of Fiscal Responsibility Legislation (FRL) frameworks

- Regulation of off-budget borrowings by States

- Reforms in the power sector distribution companies (DISCOMs)

- Rationalisation of subsidies

Fiscal Stress in States

The Commission also highlighted rising fiscal stress in several States. For example:

- Punjab: Debt–GSDP ratio of 42.9% and revenue deficit of 3.7% of GSDP (2023–24).

- Rajasthan: Liabilities at 37.9% of GSDP.

- West Bengal: Liabilities at 38.3% of GSDP.

- Andhra Pradesh: Liabilities around 34.6% of GSDP.

In some cases, borrowing is used primarily to finance revenue expenditure such as salaries and interest payments, rather than capital investment. Another concern is off-budget borrowing, where loans are raised through government-controlled entities and serviced using public funds.

Changes in Horizontal Devolution

The Finance Commission also revised the horizontal distribution formula among States. Earlier, a criterion known as tax and fiscal effort rewarded States that improved their tax collection efficiency. This has now been replaced with a “contribution to GDP” indicator with a weight of 10%.

This shift may benefit economically stronger States such as Maharashtra, Gujarat, and Karnataka, which contribute significantly to national GDP. However, poorer States such as Bihar, Jharkhand, and Uttar Pradesh, which depend heavily on central transfers, may gain relatively less, raising concerns about weakening the principle of fiscal equalisation.

Local Body Grants

The Sixteenth Finance Commission also recommended ?7,91,493 crore in grants for rural and urban local bodies. These grants are divided into:

- Basic grants for essential services and administration.

- Performance grants linked to conditions such as timely constitution of State Finance Commissions, audited accounts, and compliance with data reporting systems.

However, implementation challenges persist, as only 62.6% of recommended urban local body grants were released during the previous Finance Commission period.

Conclusion

The retention of 41% tax devolution appears to preserve the formal structure of fiscal federalism. However, the increasing use of cesses and surcharges, changes in allocation criteria, and delays in structural reforms indicate evolving Centre–State fiscal dynamics. These developments may gradually reshape India’s fiscal federal landscape, raising important questions about resource distribution, fiscal autonomy, and cooperative federalism.

India’s New GDP Series (Base Year 2022–23): A Major Statistical Reform

- 27 Feb 2026

In News:

The Ministry of Statistics and Programme Implementation (MoSPI) is releasing a new series of National Accounts Statistics (NAS) with 2022–23 as the base year, replacing the 2011–12 base year. The revised series aims to improve the accuracy and granularity of estimates of Gross Domestic Product (GDP) and Gross Value Added (GVA), reflecting structural changes in the Indian economy over the past decade.

Rationale for Revision

Since the previous base year revision in 2015, India’s economy has undergone significant transformations:

- Expansion of the digital economy and e-commerce

- Increased formalisation following the GST regime

- Shifts in consumption, employment, and production patterns

- Rapid growth of financial and service sectors

Updating the base year ensures better measurement of real growth, improved sectoral representation, and stronger evidence-based policymaking.

Key Structural Improvements

1. Sectoral Measurement Reforms

- Private Corporate Sector: Earlier, a company’s entire GVA was attributed to its dominant sector. The new approach allocates GVA based on activity-wise revenue shares, improving sectoral accuracy.

- General Government Sector: Inclusion of housing services provided to government employees and better coverage of local bodies and autonomous institutions enhances government output estimation.

2. Better Estimation of the Household Sector

The household sector—one of India’s largest contributors to GVA—will now be estimated using annual data from:

- Annual Survey of Unincorporated Sector Enterprises (ASUSE)

- Periodic Labour Force Survey (PLFS)

This replaces earlier extrapolation methods with direct annual estimation.

3. Improved Consumption Estimates

Private Final Consumption Expenditure (PFCE) will be derived from:

- Household Consumer Expenditure Surveys

- Production-side data

- Administrative datasets

This strengthens measurement of domestic demand.

Integration of Administrative Data

- Expanded use of GST data for regional output estimation and corporate value addition.

- Identification of active companies through tax records.

- Use of RBI’s Statistical Tables Relating to Banks in India (STRBI) for banking sector estimates.

- Replacement of proxy methods for private NBFCs with actual financial data from the Ministry of Corporate Affairs.

These changes improve financial sector GVA estimation and reduce reliance on assumptions.

Informal Sector and Agriculture

Greater use of ASUSE improves coverage of informal enterprises, insurance agents, and Gross Fixed Capital Formation (GFCF) in the unincorporated sector.

Agriculture estimation is strengthened using updated methodologies and data from institutions such as:

- Central Marine Fisheries Research Institute

- Central Inland Fisheries Research Institute

- Grassland and Fodder research bodies

This improves measurement of livestock, fisheries, and fodder output.

Methodological Upgrade: Double Deflation

One of the most significant reforms is the shift from a single deflator to a double deflator method.

- Earlier: Same inflation rate applied to inputs and outputs, causing growth distortions.

- Now: Separate deflators for inputs and outputs, ensuring more accurate real GVA estimates.

This reduces statistical discrepancies and improves credibility.

Additionally, Supply and Use Tables (SUTs) will be integrated, improving consistency between production and expenditure approaches.

International Alignment

India currently follows the System of National Accounts (SNA 2008). With the UN adopting SNA 2025, India plans to align with updated global standards in future revisions.

Challenges

- Complexity of double deflation and data integration.

- Back-series reconstruction may take nearly a year.

- State-level data quality variations.

- Need for greater transparency to avoid credibility debates seen in past revisions.

Conclusion

The 2022–23 base year revision represents one of India’s most comprehensive statistical overhauls in over a decade. By integrating richer datasets, modern methodologies, and improved sectoral coverage, the new GDP series aims to enhance policy reliability and international comparability. Its success, however, will depend on transparent implementation, timely back-series release, and sustained strengthening of India’s statistical ecosystem.

India’s Aviation Sector: The Case for Data-Driven Oversight

- 20 Feb 2026

In News:

India’s aviation sector has emerged as one of the fastest-growing in the world, marked by rising passenger traffic, expansion of low-cost carriers, and rapid airport infrastructure development across metros and tier-2 cities. However, regulatory mechanisms have not kept pace with this expansion.

The growing complexity of algorithm-based pricing and market concentration makes a strong case for data-driven oversight, moving beyond reactive crisis management to proactive, evidence-based regulation.

Structural Transformation of India’s Aviation

- Rapid rise in domestic air travel.

- Dominance of low-cost carriers.

- Expansion of airport infrastructure under public-private partnerships.

- Increasing use of dynamic revenue management systems for pricing.

While operational data on passenger numbers, fleet size, and freight movement is regularly tracked, systematic monitoring of fare behaviour and market conduct remains limited.

Why Data-Driven Oversight is Needed

1. Dynamic Pricing and Algorithmic Markets

Airline fares fluctuate in real time based on:

- Demand patterns

- Seat inventory

- Competitor pricing

- Seasonal variation

- Route-level market share

This makes it difficult to distinguish between legitimate demand-driven price increases and potential market power abuse.

2. Limits of Crisis-Based Regulation

Recent fare spikes in India have triggered:

- Temporary fare caps

- Requests for data submission

- Post-facto investigations

However, ad hoc interventions are reactive and do not substitute for continuous, structured oversight. Often, data collected is retrospective and insufficient for robust analysis.

3. Volume-Focused Oversight

Current regulatory practice largely tracks traffic volumes rather than pricing behaviour. In a market increasingly driven by algorithmic decision-making, this creates regulatory blind spots.

Importance of Data Transparency

(a) Identifying Route-Level Market Power

If routes dominated by a single airline consistently show higher fares compared to competitive routes, it may signal structural pricing power.

(b) Tracking Entry and Exit Effects

- Entry of a new airline → Fares usually decline.

- Exit of a competitor → Fares often increase.

Systematic data collection enables regulators to measure competitive intensity.

(c) Monitoring Peak-Period Pricing

Holiday seasons provide natural tests of pricing conduct. Disproportionate fare increases on routes with high market share may indicate dominance leverage.

(d) Algorithmic Accountability

When pricing outcomes are observable and periodically reviewed, airlines are incentivised to embed compliance safeguards within revenue management systems. Transparency acts as a deterrent without constant state intervention.

Global Best Practice: The U.S. DB1B Model

The United States’ Airline Origin and Destination Survey (DB1B), maintained by the Bureau of Transportation Statistics (BTS), provides a model for structured transparency.

- Collects ticket-level data since 1995.

- Covers a 10% random sample of domestic tickets each quarter.

- Tracks fares, routes, and carrier details.

The DB1B database enables:

- Long-term pricing trend analysis

- Competition assessment

- Empirical research

- Transparent policymaking

Adopting a similar 10% sampling framework in India could expand the role of the Directorate General of Civil Aviation (DGCA) from volume tracking to behaviour monitoring.

Addressing Industry Concerns

- Proprietary Algorithms: A sampling framework monitors outcomes, not algorithmic code.

- Technical Burden: Airlines already maintain digital databases; quarterly reporting is feasible.

- Risk of Implicit Coordination: Delayed and aggregated release of data can prevent real-time collusion risks.

Way Forward

- Institutionalise periodic, structured fare data collection.

- Build analytical capacity within regulatory bodies.

- Shift from temporary fare caps to continuous oversight.

- Promote competition while safeguarding consumer interests.

- Strengthen inter-agency coordination between aviation and competition authorities.

Conclusion

India’s aviation growth is a major economic achievement. However, rapid expansion without robust data infrastructure risks regulatory vulnerabilities. The solution lies not in heavy-handed control but in structured transparency and analytical regulation.

In an increasingly algorithm-driven aviation market, regulatory institutions must evolve toward data-centric governance to ensure fair competition, consumer protection, and sustainable sectoral growth.

Revising India’s GDP Framework

- 21 Dec 2025

In News:

India is undertaking a significant overhaul of its Gross Domestic Product (GDP) estimation framework as part of the revision of the national accounts series with a new base year of 2022–23. The reform, led by the Ministry of Statistics and Programme Implementation (MoSPI), proposes the elimination of the long-debated ‘discrepancies’ component from GDP estimates. The new GDP series is scheduled for release on 27 February 2026, while the revised back series is expected by February 2027.

Understanding ‘Discrepancies’ in GDP Estimation

GDP in India is compiled using two parallel approaches: the production (or income) approach and the expenditure approach. In theory, both should yield the same aggregate GDP. In practice, however, differences in data sources, coverage, valuation methods, and time lags lead to mismatches between the two estimates. This gap is recorded as ‘discrepancies’ under the expenditure-side GDP, which is conventionally considered less reliable than the production-side estimate.

A positive discrepancy indicates that production-side GDP exceeds expenditure-side GDP, while a negative discrepancy implies the opposite. These discrepancies have become increasingly volatile in recent years, particularly in the post-pandemic period.

Why Discrepancies Are a Concern

Large and fluctuating discrepancies obscure the true drivers of economic growth and complicate macroeconomic analysis. They also raise the likelihood of substantial future revisions in GDP growth rates, undermining confidence among policymakers, investors, and analysts.

For instance, in the July–September quarter, when real GDP growth was reported at 8.2%, discrepancies amounted to ?1.63 lakh crore, or 3.3% of GDP in real terms. In nominal terms, the discrepancy was –?2.46 lakh crore (–2.9% of GDP). Similar sharp swings were observed earlier, from –3% of GDP in January–March 2023 to 3.3% in April–June 2023.

The Proposed Reform: Integrating Supply and Use Tables

To address this issue, MoSPI plans to integrate Supply and Use Tables (SUTs) with the compilation of annual national accounts. SUTs map the supply of goods and servicesthrough domestic production and imports—against their uses, such as intermediate consumption, final consumption, capital formation, and exports. A key accounting constraint is that total supply must equal total use for each product.

By aligning GDP estimates with SUTs and the principles of the System of National Accounts (SNA), discrepancies are expected to be minimized in early estimates and eliminated entirely in final estimates once comprehensive data becomes available.

Expert Views and Persistent Challenges

Economists have broadly welcomed the move, noting that persistent discrepancies in past GDP revisions have weakened interpretability of growth trends. However, concerns remain regarding data quality, particularly the continued reliance on outdated survey data, in some cases more than a decade old. The complexity of estimating GDP in a large, diverse, and informal economy like India further compounds the challenge.

Additional issues include time lags in data availability, uneven quality of administrative records, and the risk that eliminating discrepancies may involve judgement-based adjustments, potentially affecting transparency.

Way Forward and Conclusion

For the reform to succeed, India must strengthen institutional capacity for national accounts compilation, regularly update surveys, especially in services and informal sectorsand enhance real-time administrative data systems. Methodological transparency and close alignment with international best practices under the SNA will be critical.

Overall, the proposed removal of ‘discrepancies’ represents a structural improvement in India’s GDP framework, promising cleaner, more consistent, and policy-relevant growth estimates—provided it is underpinned by robust data and transparent statistical practices.

Union Budget 2026–27: Charting India’s Path to Growth, Inclusion and Resilience

- 04 Feb 2026

In News:

The Union Budget 2026–27 was presented in Parliament by the Nirmala Sitharaman, marking her ninth consecutive Budget and the first to be prepared in Kartavya Bhawan. The fiscal blueprint is structured around three core duties or “Kartavyas” that reflect the government’s strategic priorities: accelerating and sustaining economic growth, building human capacities and fulfilling aspirations, and ensuring inclusive development across regions and communities. This framework signals an integrated approach to achieve Viksit Bharat by 2047 amid global uncertainties and domestic structural challenges.

Macro-Fiscal Framework and Priorities

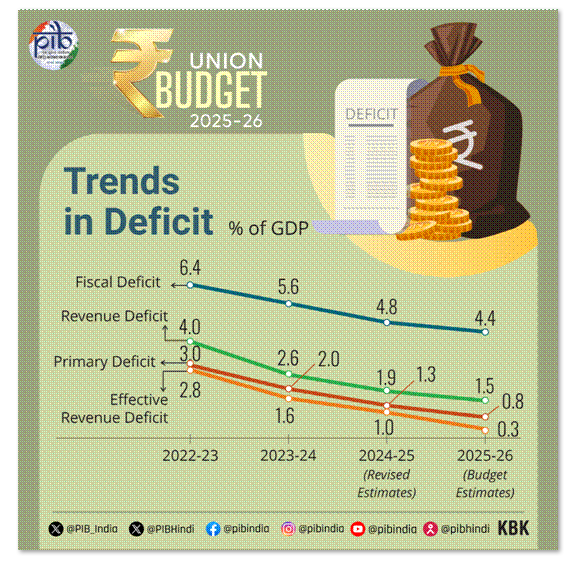

For the financial year 2026–27, the Budget projects total expenditure at ?53.5 lakh crore, with non-debt receipts estimated at ?36.5 lakh crore and net tax receipts at ?28.7 lakh crore. The fiscal deficit is targeted at 4.3% of GDP, marginally lower than the revised estimate of 4.4% for 2025–26, underscoring a continued commitment to fiscal consolidation. The debt-to-GDP ratio is projected to decline to 55.6%, indicating gradual improvement in fiscal metrics.

First Kartavya: Growth, Competitiveness and Infrastructure

The Budget places strong emphasis on strengthening India’s growth engine through investment-led strategies and sector-specific interventions. Public capital expenditure is significantly enhanced to ?12.2 lakh crore, reinforcing the infrastructure build-out across transport, logistics, waterways and urban connectivity. Seven high-speed rail corridors are proposed as growth connectors, while 20 new national waterways are slated to be operational in the coming five years.